Naibu has not released its half year results for the year ending 2014.

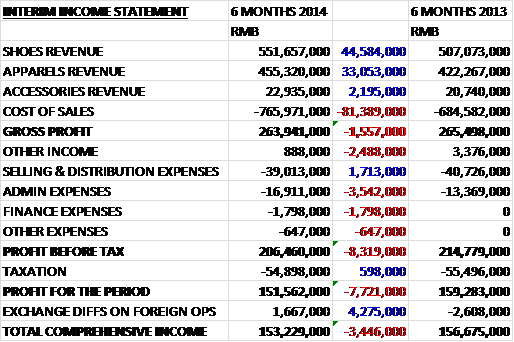

Revenues increased across all categories when compared to the first half of last year, due to increases in volumes sold as unit sales prices remained the same, but cost of sales increased by a greater degree to give a gross profit some £156K lower than last year, presumably due to the increased numbers of outsourced product being sold. Due to increasing admin expenses because of the the redundancy packages for the lost factory lines, a foreign exchange loss due to the weakening HK Dollar, and a reduction in other revenue (interest income), the reduction on last year increased with profit for the period of £15.2M lower to the tune of £772K.

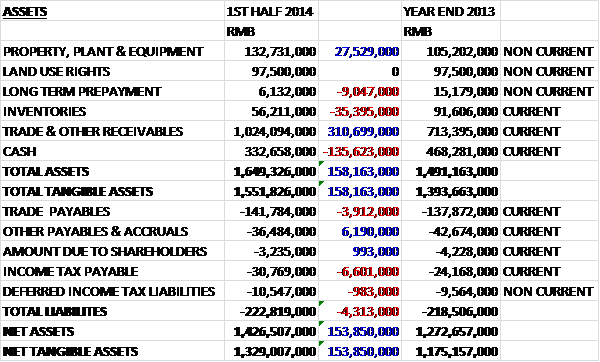

When compared to the end point of last year, total assets increased by £15.8M. This increase was almost entirely driven by a £31.1M hike in the value of receivables, somewhat offset by a £13.6M reduction in cash and a £3.5M fall in inventories. Liabilities were fairly flat as a £619K fall in accruals was counteracted by a £760K increase in tax liabilities. Overall then, net assets increased by £15.4M to £142.7M.

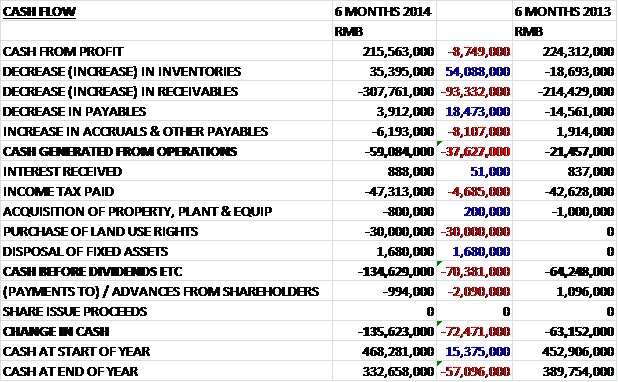

Before movements in working capital, the £21.6M cash income was £875K lower than during the same period of last year. Unfortunately this was obliterated by a £30.8M increase in receivables which meant that there was a £5.9M outflow of cash from operations, some £3.8M worse than last year. On top of this, the group paid £4.7M in tax and £3M to purchase land use rights for the new factory which all contributed to a pretty poor £13.6M outflow of cash during the period to leave the group with £33.3M left in the bank.

Apparently due to increasing competition, a number of smaller players have now exited the market which means that the board are expecting some recovery in their end markets. The market remains highly competitive, however, as foreign brands have stepped up their business expansion into second and third tier cities. The group has now adopted a more prudent approach to expansion by growing existing stores and cutting back on new store openings. The current store portfolio stands at 3,192 stores with 170,000 square metres of sales space. They are developing a new brand based on a European fashion concept that is expected to launch in 2015.

As previously announced the new Quangang plant did not commence production due to a lack of skilled workers. Somehow, Naibu has now managed to lease the factory out at an annual rent of £600K. Quite what the company renting the factory is going to do with a facility that it can’t fill with staff is a bit of a mystery. In the meantime, the company has made arrangement for their OEM suppliers to continue making the products that would have been manufactured in the Quangang plant. In Dazhu County, the group has paid the second instalment of £3M for land use rights and expects to pay the remaining £2.2M upon granting of the certificate in Q1 2015. The land is in the process of being prepared and it is expected that the facility will be operational in Q2 2016.

Part of the cause for the huge increase in receivables was the inexplicable decision to extend credit terms to distributors to 120 days. Apparently this has not resulted in any accruals of bad debts which seems very unlikely in my opinion. In order to help their network partners reduce their operating cost pressures, the group has been granting subsidies to distributors for store refurbishments, which have apparently helped increase sales. It is interesting to note that the group is granting subsidies to their customers and extending credit terms to their suppliers and are getting squeezed in the middle.

Net profit for shoes was £7.2M, a fall from the £7.8M recorded last year. Net profit for Apparel and Accessories was £8.4M, an increase of £300K over the same period of last year. Due to the declining cash position, and presumably because there is little hope of any of those receivables turning into cash, the board have elected not to pay an interim dividend this time. So, what do we have here? Despite the increasing profits, the decision to extend credit terms with their customers means there is a cash outflow from operations. Due to this, the dividend has been stopped and one of the main reasons for holding the share has been removed. I really do want to believe in this company but it is looking more and more likely to me that there is about to be a massive write-off of bad debts (even though this is denied by Naibu). I will keep my small holding but I really can’t advocate buying the shares until the uncertainty about those receivables has been sorted out.

On the 17th October the group released a statement that reported some errors in the financial accounts. The cost of decoration and machinery for he Quangang factory was £2.6M and not £260K as stated. Also, the figure of construction in progress relates to Quangang and Dazhu, not just Quangang as stated. This does not really inspire confidence but at least the errors have been highlighted.

On the 24th November the group informed the market that since the half year point there has been a slowdown in sales of Naibu products that has led to some overstocking by distributors. The company is now intending to introduce a limited programme of discounting in order to “reduce the overstocking within the distributor system”. Therefore there is unlikely to be a dividend this year as they address this issue but they may start paying them again in 2015. This all seems very convenient and I have pretty much given up on finding any value here.

On the 2nd January the company announced that Zhen Li has resigned as CFO. This is yet another ill omen.

On the 9th January it was announced that the non-executive directors have requested suspension of the company’s shares pending clarification of its trading position. Not really much of a surprise, this, but it looks as though they are finished.

On the 18th February it was announced that the UK based non-executive directors have been unable to contact any of the Chinese executive directors. In order to clarify the situation they have appointed KPMG to prepare a report on the group’s financial position. The non-executives have asked CEO Mr Lin to co-operate with KPMG but as they cannot find him, he has not indicated that he will do so! Further announcements will be made in due course.

On the 29th April the non-executive directors released an update. They have been unable to obtain the co-operation of Chairman Huoyan Lin to progress the appointment of KPMG to review the financial positon of the group and have therefore appointed a leading Chinese law firm to initiate legal action to gain control of the operating subsidiary of the group and the associated accounts. They have been able to contact Lin but his lack of co-operation means that his employment contract has been terminated, along with that of VP of production, Congdeng Lin. The company’s shares remain suspended but at least actually speaking to one of the executive directors seems to be progress. I still find it unlikely that there is any value left in this company, however.

On the 22nd May a statement was released that said the non-executive directors felt a resolution would not be reached before the 6 month AIM deadline in July, the NOMAD has resigned and there was little prospect of appointing another one. Therefore the AIM listing will be cancelled on 22nd June with a private dealing facility a possibility going forward (I won’t hold my breath). What a total shambolic disaster.