GVC has now released its half year results for the year ending 2014.

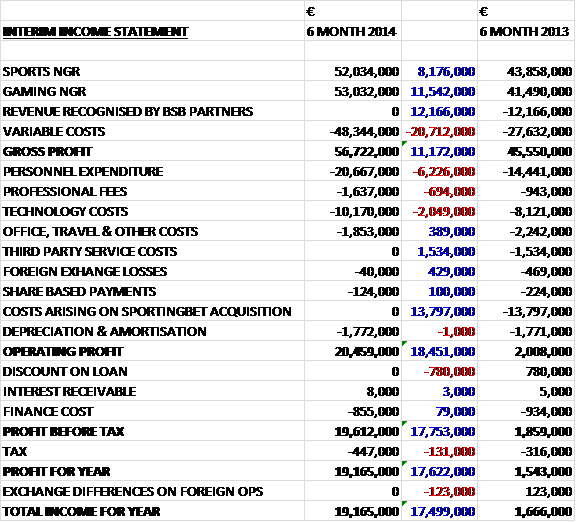

Both sports and gaming revenues are up, with Gaming revenue doing slightly better, increasing by €11.5M. Variable costs were also up but Gross profit improved by €11.2M over the first half of last year. The group increased some costs with personnel expenditure up €6.2M, professional fees increasing by €700K and technology costs up €2M. Conversely, there were lower office and travel costs, less foreign exchange losses and the lack of €1.5M in third party service costs. The real improvement over last year, however, was the lack of nearly €14M in costs relating to the Sportingbet acquisition. Overall operating profit was up by €18.5M before slightly higher taxes and the lack of a discount on a loan meant that profit for the half year was a very healthy €19.2M, some €17.6M more than in the first half of 2013.

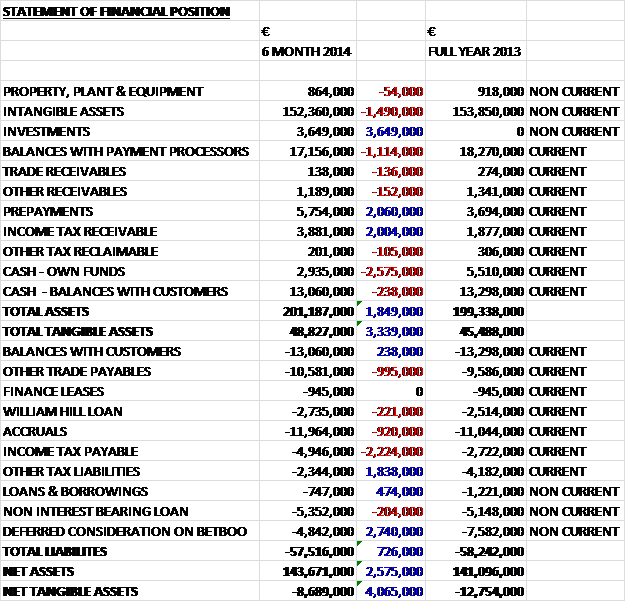

Overall total assets crept up by €1.9M as the €3.6M invested in Betit and €2M increases in both prepayments and income tax receivables were partially offset by a €2.8M fall in cash levels, a €1.5M reduction in intangible assets and a €1.1M decline in balances with payment processors. Conversely, total liabilities showed a small decline as a €2.7M fall in deferred consideration and a €1.8M decline in other tax liabilities were partially counteracted by a €2.2M increase in income tax payable. Overall this led to net assets increasing by €2.6M to €143.7M.

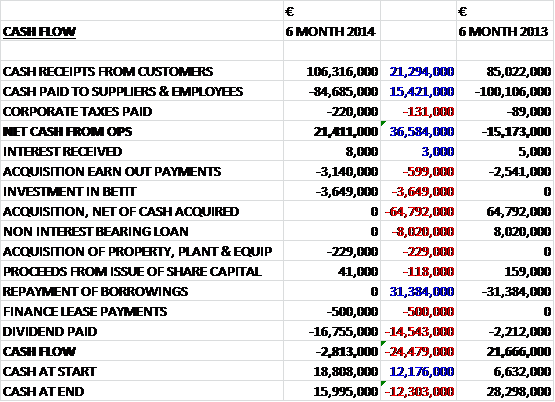

A combination of more cash receipts from customers and less paid out to suppliers and employees meant that net cash from operations was a very decent €21.4M compared to an outflow of €15.2M in the first six months of last year. Of this cash, €3.1M was spent on contingent consideration and €3.7M was invested in Betit. Half a million was spent on finance lease payments relating to computer hardware for the data centres but the rest, some €16.8M, was paid out in dividends. This meant that there was a €2.8M cash outflow in the half year to end the period with €16M. This cash flow statement shows just how cash generative the group is.

Previously the group announced that it had paid €3.5M for a 15% stake in Betit. There is a call option to acquire the balance of the outstanding shares that can be exercised between July and September 2017. The minimum call price is €70M and the actual price would be determined by the mix of revenues between regulated and non-regulated markets. If the call option is not exercised, Betit may require the group to acquire the shares at a certain price.

Overall wagers are up 38% to €694M and the current number of active customers have increased by 22%. The Latin American business continued to grow well and is the market leader in the region for sports betting. Across all businesses in-play now amounts to 70% of wagering with mobile now accounting for 22%, up from 8% in the first half of last year before GVC made investments into this part of its offering. Going forward the group is looking to further enhance the mobile product and sports book next year. There has been a strong start to Q3 with trading per day 20% higher than in Q3 last year.

The group has announced an interim dividend of 12.5c plus a special dividend of 2.5c which to my calculations gives an annual yield of 8.8% at the current share price – still an incredible distribution. Cash flow is very strong, the world cup has seemed to add considerable numbers of new customers and that dividend pay-out is very impressive. Risks remain as the group operates in many grey areas with Turkey of particular concern but overall this seems a good investment even at these prices.

On the 16th December the group released a trading statement covering much of the final quarter of the year. Net Gaming Revenue for Q4 to date averaged €660K per day, an increase of 26% on the same quarter of last year; there was a sixth successive quarter of growth in deposit values with this quarter being 20% higher than Q4 last year; and investment in the mobile development is bearing fruit with Mobile Gross Gaming Revenue up 150% to €168K per day. Trading was strong across all major territories and brands and the board believes that this strength provides a good foundation for continued growth in 2015. Market expectations for the full year will be at least matched in 2014 but it is worth baring in mind that 2015 does not have a major sporting event on the scale of the world cup. Overall a very pleasing update.

On the 12th January the group released a pre-close trading update. In Q4, total NGR was up 22% when compared to the same quarter of 2013 but fell slightly when compared to Q3. There was a record level of sports turnover in the quarter, up 11% on Q4 2013 and NGR for the year was £224.6M, up 23% on last year. An interim dividend of 12.5c was declared which was an increase of 8.7% on last year. A decent update, but this was priced into the shares.

On the 14th January it was announced that investor Richard Griffiths had sold 522,026 shares worth about €2.5M to leave him with just under 13% of the total share capital. This is quite a substantial sell from a well known investor and I hope he is not intending on selling much more of his holdings.