Tesco has now released their interim results for 2015.

There is no denying that this is a poor set of results. Revenue in the UK fell by £600M when compared to the first half of last year. In the overseas markets, the performance was just as bad with Asian revenue falling £438M and Continental Europe down £427M. The revenues at the bank did fare better, posting a £23M increase and the fall in the cost of sales did partially mitigate the falling revenue but gross profit was down by more than a billion pounds. Admin expenses actually increased during the period to give an operating profit of £347M, down by an eye watering £1.22BN. Due to the lower profits, taxation did fall and there was a much lower loss from discontinued items but the profit for the year stood at a paltry £6M which was £814M lower than in H1 2014.

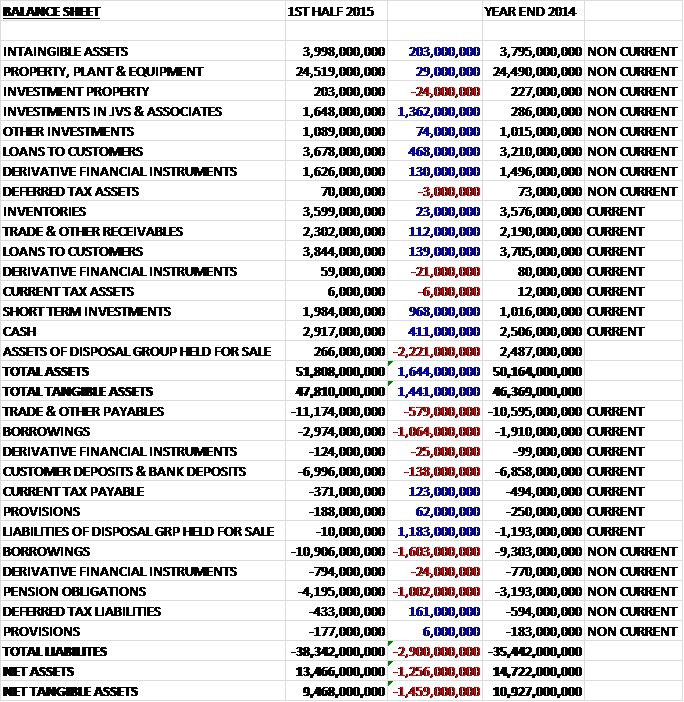

Total assets increased by £1.644BN driven by a £1.362BN increase in joint venture investments relating to the Chinese business, a £968M growth in short term investments, a £468M increase in the value of loans to customers and a £411M hike in the cash levels somewhat mitigated by a £2.221BN fall in the assets held for sale. Liabilities also increased during the six month period with borrowings up a massive £2.667BN, a one billion increase in pension obligations due to a reduction in real corporate bond yields, and a £579M increase in payables which was somewhat counteracted by the £1.183BN reduction in liabilities held for sale.

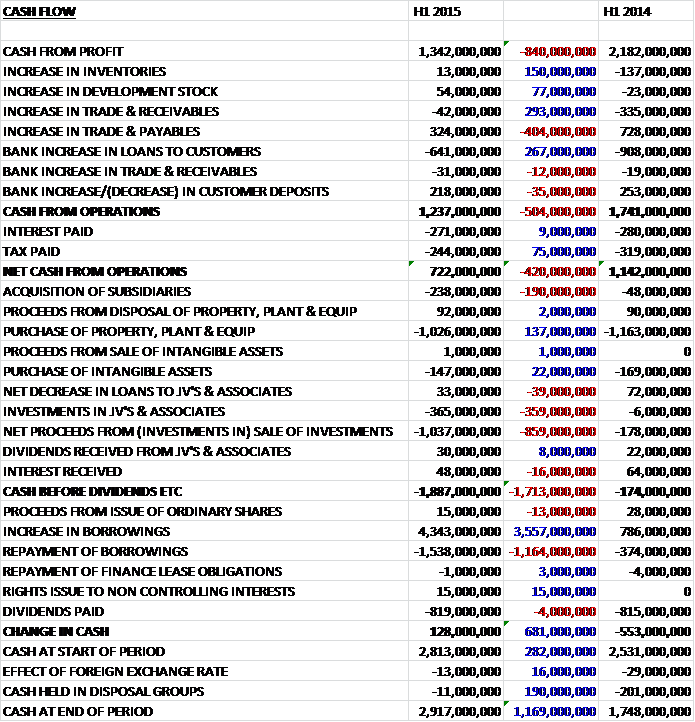

Before the movement in working capital, cash profits collapsed by £840M to £1.342BN. Working capital movements did not change this figure much as a large increase in bank loans to customers were counteracted by increased customer deposits and payables which meant the cash from operations stood at £1.237BN, a £504M decline. After tax and interest was paid, the net cash from operations was £722M which didn’t even cover the £1BN of new tangible assets purchased let alone the £1BN investment, £238M spent on acquisitions, £365M invested into joint ventures and £819M spent on dividends. In order to pay for all this the group took out £2.8BN of net new borrowings to give a rather arbitrary £128M increase in cash. This is clearly not a sustainable situation.

UK trading profit fell by £632M to just under half a million pounds. This period has seen the continued trend towards convenience stores and online retail and Tesco’s relative performance fell short of initial expectations. The decision to reduce the level of couponing activity impacted sales in the short term and like for like sales fell by 4.6%. The group are intending to open another 500K ft2 of new space, mostly in Express and One Stop formats. In total, 262 store refreshes were completed in the first half of the year but the group are reducing their capital expenditure which will slow this programme down going forward.

Asian profits fell by £54M to £260M, held back by difficult market conditions across the region. Market conditions in Korea remained challenging with a higher number of enforced Sunday closures under the DIDA opening regulations. In Thailand the political system improved with the ending of the curfew but the environment remained uncertain for customers and sales were also impacted by increasingly competitive convenience sector. The performance in Malaysia was impacted by low customer sentiment and more recently by protests against Western businesses. The group opened 600K square feet of new space and intend to open a similar amount next half.

European trading profits increased by £21M to £76M on falling sales but positive like for like sales were seen in the Czech Rep, Hungary and Turkey. The profit increase was predominantly due to a lower depreciation charge following last year’s asset impairments but further profit growth was held back by increased pressure on sales in Ireland and Slovakia. In Ireland in particular the market remained challenging with intense competition from the discounters. In Poland the group managed to maintain market share but the market as a whole was hit by lower customer confidence after sanctions were announced against Russia. In Hungary and the Czech Rep, the performance was supported by strong clothing sales. In Turkey, an improvement in like for like sales was seen across the first half of the year. Tesco continued to limit capital expenditure in the region, opening 200K square feet of new space and closing a similar amount of underperforming stores.

Tesco Bank profits improved by £14M to £102M driven by strong lending growth. Customer accounts in the core banking products grew by 14% and the launch of personal current accounts in June completed the portfolio. The result included a further £27M increase in the provision for PPI claims and broadly growth in the bank’s underlying trading profit for the full year will be offset by investment in the current accounts.

The group previously announced that the six month profit guidance was overstated due to the accelerated recognition of commercial income and delayed accrual of costs. It has been determined that this issue also impacted previous statements and the profit before tax for last year was overstated by £70M and in prior years by £75M. Now the FCA has commenced an investigation which is likely to result in significant legal and other costs and potential fines or penalties against the group, along with some potential third party claims. Due to all the issues affecting the group, management have declined to offer a full year profit guidance at this time.

In may the group completed the formation of a new venture with China Resources and it has exchanged its Chinese retail and property interests plus cash of £334M (including £77M due to be paid next year) for a 20% interest in the new venture. In March an agreement was entered into with Tata to form a 50:50 joint venture in India (Trent Hypermarket Ltd which operates the Star Bazaar retail business). An investment of £85M has been recognised in regards to this. In April the group acquired Sociomantic Labs, a German based digital advertising provider for £124M including £38M of deferred consideration.

Tesco have flagged up the potential for employee claims over changes to the calculation of holiday pay in the UK and variable pay in Korea, so this should be watched carefully. Due, I suspect, to the revelations about the over statement of profits, the Chairman has announced plans to leave and is “preparing the ground to ensure an orderly process for his succession”.

Net debt at the end of the period increased by £984M to £7.491BN. The interim dividend was cut from just 4.63p to 1.16p and at the current share price if the final dividend is not cut this still represents a yield of 6.6%. It seems very likely that the final dividend will be cut, however, and if it was reduced by the same percentage as the interim dividend, it would be 2.53p and represent a total yield of 2.1% which is rather poor. This is clearly a difficult time for Tesco. They are having problems across all of their markets and have also been hit by the mess involving income recognition which is likely to result in further costs. It really is difficult to see any silver linings at the moment, unless the performance in some of the European markets is a sign of a recovery there. I am certainly not going to invest further given the current uncertainty but might as well wait it out with my current shares.

On the 29th October the group confirmed that it has been notified by the Serious Fraud Office that it has started an investigation into accounting practices at the company and in light of this investigation, the FCA has discontinued its own investigation.

On the 9th December the group released a profit warning stating that due to the changes and investments made trading profit for the year will be under £1.4BN. They have retrained the entire team due to the revenue allocation scandal and have invested further in service and product availability to try and win back some lost business. This is clearly bad news but not totally unexpected I would say.

On the 8th January the group released a trading statement covering Q3 and Christmas trading. Overall, like for like sales excluding fuel fell by 3.8% in Q3, an improvement over the 4.8% decline in Q2 but worse than the decline in Q1. The performance improved throughout the quarter, however, and culminated in a decline of just 0.6% over the Christmas period. In the UK there was a 4.2% decline in Q3 and a 0.3% decline over Christmas. Asian sales were hit by a 5% decline with a poor performance across all territories but things were slightly better in Europe with a decline of just 1.2% over the quarter. Indeed sales in the Czech Republic were up 2.9%, Hungary was up 1.4% and Turkey up an impressive 6.7%, although Ireland remained a drag. The group trading profit guidance of no more than £1.4BN remains in place.

In the UK the group has seen a strong improvement in satisfaction in store, aided by the introduction of more than 6,000 new customer facing staff members. Like for like volume growth in fresh food over Christmas was positive for the first time in five years. General merchandise showed a positive sales growth over Christmas and Black Friday promotions resulted in the highest week of sales on record for Tesco Direct contributing to a 22% like for like sales growth in online merchandise. Convenience and online grocery sales also increased with a 4.9% and 12.9% increase respectively over Christmas. As mentioned, market conditions across Asia remained challenging with performance in Korea suffering from more enforced Sunday closures and performance in Malaysia especially poor. There was an improving trend in Thailand, however, as the impact of political disruption became annualised. Sales at the bank increased by 3% due to a broader product range in mortgages and loans, although this was partly offset by a more competitive insurance market.

Dave Lewis also used this update to outline some of his plans for structural change in the group. They included the appointment of the CEO of Halfords, Matt Davies as the new CEO of the UK and Ireland business – he will start on the 1st June. There will be a restructuring of central overheads, simplification of store management structures and increased working hour flexibility which is expected to deliver cost savings of £250M at a one-off cost of £300M. The decision was made to consolidate head office locations, closing Cheshunt in 2016 and making Welwyn Garden City the new HQ and to close 43 unprofitable stores. In addition the decision was made to revise the store building programme, close the company defined benefit pension scheme, reduce capital expenditure to about £1BN, dispose of Tesco Broadband and Blinkbox to TalkTalk, loo at offloading the dunnhumby business and not pay a final dividend for this year.

To some extent this is another disappointing update with declining sales but the improved performance towards the end of the quarter is cause for some cautious optimism and the measures taken to improve profitability in the medium term certainly suggest the group’s issues are being tackled so for the first time in a long time I am a bit more optimistic about my shares here but not quite enough to buy any more this time, although once the market euphoria over the update has died down I may try and pick up a bargain here.

On the 17th February the group announced the appointment of John Allan as chairman. He will join at the start of March and be paid a fee of £650K per annum (not bad work if you can get it!). He has previously been CEO of Excel and then CFO of Deutsche Post. More recently he was chairman of Dixons Retail and oversaw a quadrupling of the share price before the merger with Carphone Warehouse.

On the 4th March it was announced that Byron Grote will be joining the board as non-executive director and Gareth Bullock will be retiring from the main board to concentrate on his role on the board of Tesco Bank. Byron is currently non-executive director at Unilever, Anglo American, Standard Chartered and Akzo Nobel but will step down from the Unilever board at the end of April. He was previously CFO of BP from 2002 to 2011.

On the 20th March the group announced a deal whereby it took sole ownership of 21 superstores from the joint venture with British Land along with £96M in cash in return for Tesco’s stake in three shopping centres, three retail parks and three standalone stores. The acquired stores were subject to RPI indexed rent increases and the group will continue to lease the stores that British Land acquired at market rents not subject to RPI indexed increases. This seems like a good deal to increase the proportion of stores owned as freeholds which can only be good in the long term.