Air Partner has now released its interim results for 2015.

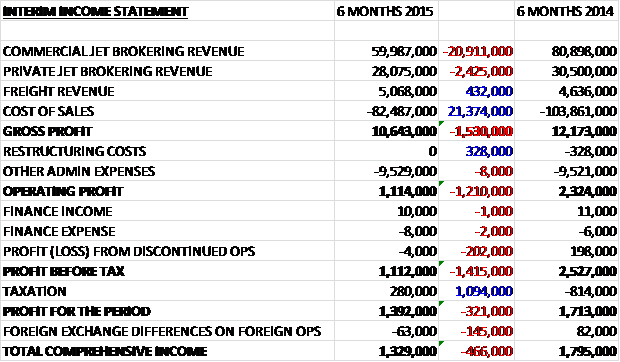

Commercial jet brokering suffered a fall in revenues of £20.9M when compared to the first half of last year and private jet brokering sales fell by £2.4M. Revenues at the freight business actually improved, up £432K. Sales improved across all geographic markets except France and Germany. Costs of sales were also down but gross profit still fell by £1.5M. The lack of restructuring costs were somewhat offset by the lack of £200K worth of profit from the discontinued Fuel business to give a profit before tax some £1.4M lower. The group actually got a tax rebate during the first half of this year due to £750K of an R&D tax claim recognised during the period which meant that profit for the year wasn’t so bad, down £321K at £1.4M.

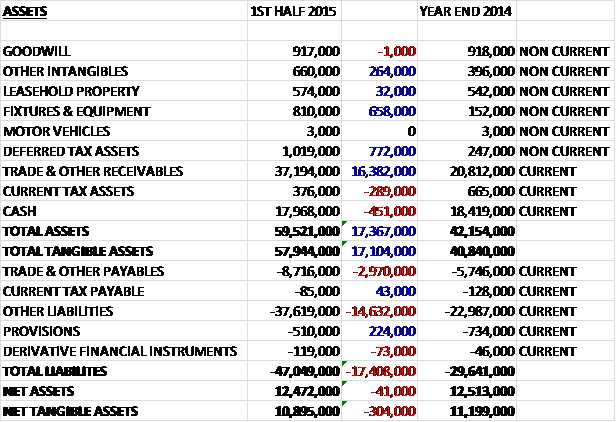

When compared to the end point of last year, total assets were up £17.4M driven almost entirely by a £16.4M increase in receivables and a much smaller increased in deferred tax assets and fixtures & equipment. Total Liabilities also increased due to a £14.6M hike in “other” liabilities and a £3M increase in payables. This all meant that net tangible assets fell by £304K to £10.9M.

Before movements in working capital, cash profits were down by £1.6M to just £1M. A large increase in payables was broadly offset by an increase in receivables and the tax paid during the first half of this year was about half that of last year so that net cash from operations, at just under £2M was some £1.3M worse than last year. The group then paid £777K for property, plant and equipment and £276K on intangible assets, relating to software, which were both covered by the cash from operations before a £1.4M payment on dividends meant that there was a £387K outflow of cash in the half year. Given that the group finished the year with £18M in cash, it seems they can afford to pay those dividends but the outflow was some £3.5M worse than the inflow during the same period of 2014.

During the first half of the year Commercial Jet Brokering showed a segment result of £1.1M, a decrease of more than £800K from the first half of last year. Last year the group benefited from a number of large one-off contracts that were not repeated this year which has led to the decline in profits. Action has been taken to reduce the division’s costs but on the plus side the group is seeing growing sales outside of the core government and military contracts with Tour Operating being particularly strong in the UK, Austria and Italy. Oil and Gas activity provided decent revenues with a particularly strong performance in the UK and the US with a 227% increase in sales in the States. Finally, there was a greater amount of customer activity in the automotive industry through new car launches.

Private Jet Brokering profits fell by £400K to £590K which reflects the investment that the group has made in its sales team. The market remains challenging, especially in Europe but Italy and Switzerland have delivered strong performances. The strong performance of the Jet Card bodes well for the future here and as the customers start to use the pre-paid hours held on their cards, the board expect to see improved profitability.

The Freight segment produced a result of no profit, a £21K improvement on last year which reflects new business wins and the investment made in new recruitment which led to a 32% growth in newly acquired business after a large government contract came to an end. The contract for the UK’s Department for International Development has been extended for another year which has involved supplying aid flights to the Middle East. Areas that have shown growth have been automotive and freight forwarding.

The Jet Card initiative seems to be doing well after the group has strengthened the sales teams in both the UK and the US. Deposits on the card are at an all-time high and £5M of the cards were sold during the period to give a record deposit on the card of nearly £12M. The roll out of the CRM IT system is now complete having cost £300K and the group has also implemented a complete IT upgrade which has taken the total technology spend during the period to £1M.

The interim dividend has been increased by 10% to 6.66p per share which seems to suggest a yield of about 7.7% at the current share price, which is a very good return. Due to the nature of the business, there is limited visibility for sales but the board remains confident that expectations for the rest of the year will be met. There is no doubt that this is a disappointing set of results for the group. Profits at both of the main businesses have declined, mainly due to less governmental work. The net assets also fell and the group recorded a cash outflow. The cash levels, however, are decent and the yield is very good so this was not a disaster but I feel I would rather wait until the group starts growing sales and profits before investing.

On the 15th October it was announced that a large shareholder, Richard Griffiths had sold shares so that he now owns less than 5% of the company which is not exactly a ringing endorsement.

On the 4th December the group released an interim statement. Trading in both the Commercial Jet and Private Jet divisions continues to perform in line with expectations and during the period the Commercial Jet division undertook a number of large projects including a programme of car launched with a major European manufacturer involving the movement of over 20,000 passengers to various press launches. The smaller Freight division has performed ahead of expectations due to work arising from assisting aid agencies in West Africa. This seems to be a good time to test the waters here so I have bought some shares.

On he 14th January it was announced that investor Richard Griffiths had sold a substantial amount, perhaps most, of his shares to bring his holding from above 4% of the company to below 3%. It seems Richard doesn’t see the share price going anywhere soon.

On the 30th January the group announced that since the last update the Commercial Jets division put in a better than expected performance over a traditionally quiet period. The board still expect full year profit to be in line with current expectations though. All in all, this sounds promising and I am happy with my holding here.

On the 13th March it was announced that non-executive director Grahame Chilton would be stepping down from the board having spent nearly two years with the group. He has accepted the role of CEO at Arthur J Gallagher Intl and as such will no longer have the time to devote to Air Partner, which is fair enough.