GSK has now updated the market on its performance in Q3 2014.

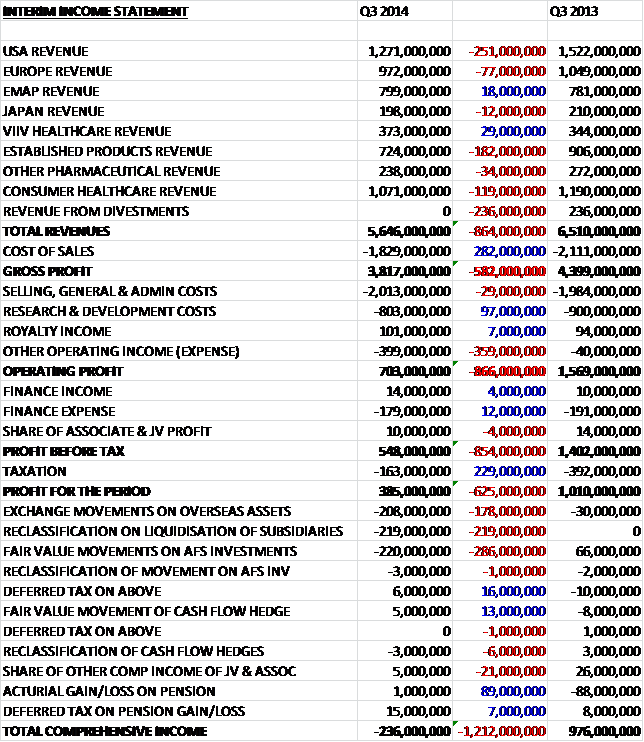

Revenues fell across most markets with US sales down £251M, Established product revenues down £182M and European sales decreasing by £77M. The only sectors to improve over Q3 last year were ViiV healthcare, up £29M and Emerging Markets, up £18M. Cost of sales also fell but gross profit for the quarter fell by some £582M. General and admin costs were broadly flat whilst R&D costs fell but these were dwarfed by a £359M increase in “other” operating costs which included a £114M charge to account for an additional year of US branded prescription drug fee. Taxation, as would be expected, fell by £229M to give a profit for the quarter of £385M, a vast £625M reduction on the total in Q3 2013.

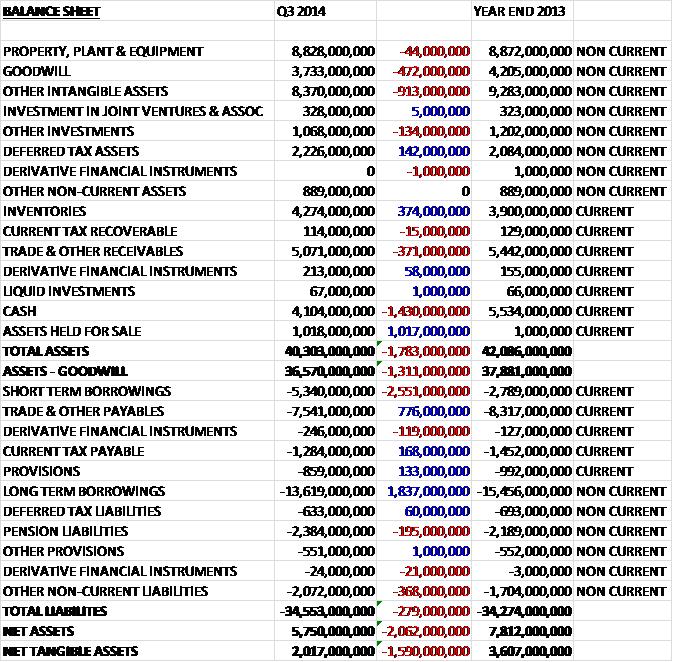

When compared to the end point of last year, total assets at the nine month point of 2014 collapsed by £1.783BN. This fall was driven by a 1.43BN decline in cash, a £913M fall in other intangible assets, a £472M reduction in Goodwill and a £371M decline in the value of receivables. These falls were partially offset by a £1.017BN increase in assets held for sale, mainly relating to £936M in relation to the Novartis transaction, and a £374M hike in inventories. Liabilities increased somewhat during the period driven by a £714M increase in borrowings, a £368M increase in other liabilities and a £195M increase in pension liabilities, partially attributable to the stronger dollar in relation to US pensions, counteracted by a £776M decrease in trade and payables. Overall then, this all meant that net assets collapsed by more than two billion pounds to £5.75BN.

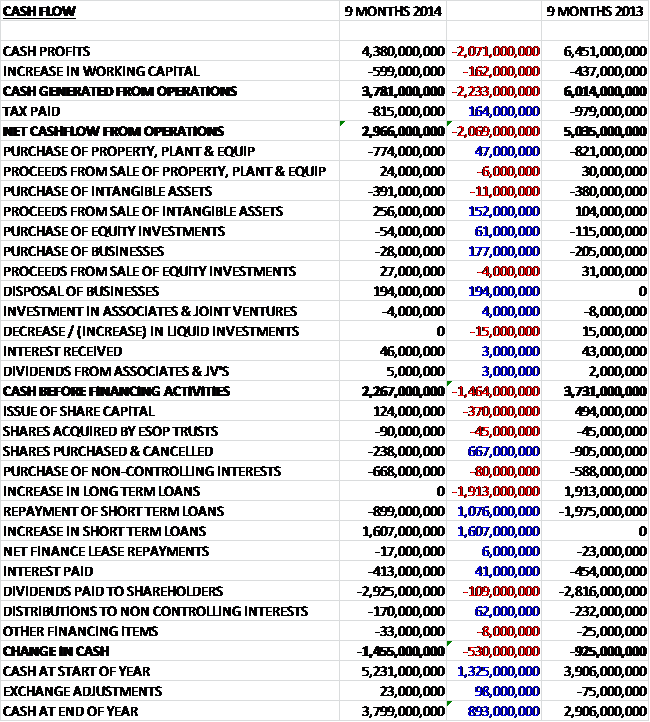

Before movements in working capital, cash profits were down by more than two billion pounds at £4.38BN. After the increase in working capital and the tax was paid, the net cash income from operations was just under £3BN, a £2BN fall when compared to the first nine months of 2013. Of this £3BN, £774M was spent on property, plant and equipment; and £391M was spent on intangible assets before £256M was recouped by flogging off intangible assets and £194M from the disposal of a business. The group also spent £668M on the purchase of non-controlling interests relating to 25% of the Indian subsidiary and 30% of the Indonesian Consumer Healthcare business not already owned, and £238M spent purchasing and cancelling shares. GSK also brought in some cash by gaining over £700M of new loans. After £3BN was spent on dividends the overall result was a £1.455BN outflow of cash to give the group £3.8BN of cash at the end of the period. It can be seen from this cash flow that although there is a fairly strong operational cash flow, the dividends are not covered by cash flow and the total outflow was some £530M worse than last year.

Respiratory sales fell 8% this quarter. Seretide/Advair revenues fell by 13% to £976M, Flovent/Flixotide sales decreased by 6% but Ventolin sales increased by 16%. Relvar/Breo Ellipta, now launched in the US, Europe and Japan saw sales of £15M. The US was particularly badly hit with sales down 18% reflecting the continued price and contracting pressures. The increase seen in Ventolin sales included benefits from wholesaler and retailer stocking patterns and favourable adjustments to previous accruals for returns and rebates. European sales were down 3% reflecting increased competition but sales in Emerging markets were up 13% benefiting from a strong comparative performance in China as the effects of the government investigation are annualised. In Japan, sales grew by 3% with growth from Veramyst and Xyzal offsetting declines in Adoair and Flixotide.

Oncology sales grew by an impressive 35% to £311M. In the US, revenues grew by 44% driven by increases in Votrient and Promacta sales along with the newly launches Mekinist and Tafinlar. In Europe, sales increased by 26% as Votrient sales increased by 5% and Promacta sales grew by 33%. In Emerging markets sales grew by 33% and in Japan they were up 19%. Cardiovascular sales fell by 3% as a 24% increase in Duodart sales was counteracted by a 4% decline in Avodart sales, a 41% collapse in Levitra sales and a 31% decrease in Prolia sales due to the agreement with Amgen to terminate the joint commercialisation in a number of European markets, Mexico and Russia. Regionally, sales in the US fell 18% and European sales fell by 1% but these falls were partially offset by a 15% increase in Emerging Markets and a 14% hike in Japanese sales.

Immuno-inflammation sales grew by 46% but remained small at £65M. This was driven by a 14% increase in Benlysta sales. Other Pharmaceutical sales fell by 8% reflecting generic competition to Dermatology products in the US, and a 54% decline in sales of Mepron following the start of generic competition in March. ViiV Healthcare sales increased by 18% with the US up 32%, Japan up 48% and Europe increasing by 12%, somewhat offset by a 13% decline in Emerging Markets. The ongoing roll out of Tivicay resulted in sales of £78M and Epzicom, which benefited from use in combination with Tivivay increased by 13%. Selzentry sales, however, fall by 6% during the quarter. The launch of Triumeq is now well underway and registered sales of £9M. These increases were offset by a 48% fall in Combivir sales and a 58% collapse in the sales of Trizivir.

Established Product sales fell by 14% with declines in all regions except Emerging Markets which benefited from an improved performance in China. Generic competition to Lovaza, down 58%; Seroxat, down 11% and Valtrex, down 29% all contributed to the decline. Vaccine sales were flat with sales in the US falling 3% following the return of a competitor product, offset by strong performances in Emerging Markets and Japan. Infanrix was down 12% with declines in the US reflecting the return of a competitor vaccine that experienced supply problems in 2013. Boostrix sales increased by 37% with growth in all regions but in particular, benefiting from the phasing of tenders in Emerging Markets. Cervarix sales declined by 17% due to declines in Emerging markets; Fluarix sales fell by 8% reflecting the later phasing of seasonal shipments; sales of hepatitis vaccines fell by 6% due to supply constraints that affected the US and Emerging markets in particular; Rotarix revenue was up 2% due to a strong performance in Japan and Synflorix sales grew 34% reflecting the phasing of tenders in Emerging Markets.

Consumer Healthcare turnover fell by 3% in the quarter and was adversely impacted by a number of supply problems and a continued slow-down in emerging markets. The supply issues will continue until the end of the year but steps have apparently been taken to combat them. Wellness sales fell by 8% due to supply issues that affected Smokers Health products particularly badly. Oral Health sales grew by 2% as the continued growth of the Sensodyne brand was partially offset by a decline in Aquafresh. Nutrition revenue grew by 4% driven by an 8% increase in Horlicks sales, particularly in India. Skin Health sales fell by 13% due primarily to supply interruptions to Bactroban in China and sales of new products accounted for 8% of turnover during the quarter. In Q4 2013, Breo Ellipta was launched in the US for COPD and Relvar Ellipta was launched in Europe for COPD and asthma in Q1 2014. Tivcay was launched in the US and Europe and Triumeq was also launched in both territories during Q3 2014.

There have been a number of movements in the pipeline this quarter. A malaria vaccine candidate has been submitted for EU regulation; Fionase, an allergy relief, has received FDA approval for over the counter sales in the US; FDA approval has been received for Arnuity Ellipta (Asthma), Triumeq (HIV) and Promacta (Anaemia); Triumeq has also received EMA approval for use in the EU and a number of potential treatments have received good Phase III results but the darapladib atherosclerosis and Tykerb adjuvant BC programmes were stopped.

The main problem for GSK is that the contract changes to Advair have affected US sales more than was expected and the rate of the decline is expected to continue for the foreseeable future. This is the one major blockbuster drug that the group have and the declining sales really are a major problem. In the quarter Advair sales were £976M with the next most important drug the vaccine Infanrix selling just £212M (itself in decline). Additionally sales in Consumer healthcare seem to be being affected by supply issues but conditions in China have improved and ViiV Healthcare seems to be doing OK. In response to the declining Advair sales the group have reduced costs in admin and R&D and expect to be able to make £1BN in annual cost savings at an initial cost of £1.5BN. Due to some of the new Respiratory products, however, the group expects the division to return to growth by 2016.

At the end of the period the group had provided £500M for various legal and other disputes. During the period the People’s court in China ruled that GSK China had offered money or property to non-government personnel in order to obtain improper commercial gains and had been found guilty of bribing non-government personnel. As a result of the court’s verdict, the group has paid a fine of £301M to the Chinese government which will hopefully draw a line under the problems in the country.

In April the group announced a transaction with Novartis involving Consumer Healthcare, Vaccines and Oncology. A new Consumer Healthcare business will be created with GSK having a 63.5% majority interest. In addition GSK will acquire Novartis’ vaccines business excluding flu vaccines for $5.25BN with potential milestone payments of up to $1.8BN and ongoing royalties. GSK is also divesting its Oncology portfolio for a cash consideration of $16BN, of which $1.5BN depends on the results of an ongoing clinical trial. The transaction is expected to be completed during the first half of 2015 and the group are also expecting to be able to divest some of the pharmaceuticals in their Established Products portfolio.

Going forward this year the board expect core EPX on a CER and ex divestment basis to be broadly similar to that of 2013. Currency problems continue to affect the group and the strong Sterling has had a negative impact on core EPS of 8% and if exchange rates were to remain unchanged it is thought that core EPS in Q4 will be adversely affected by 7%. This year there were a number of one-off costs. Restructuring charges of £113M (compared to £83M) included £12M under the Operational Excellence Programme and £81M under the Major Change Programme. Legal charges of £318M (£73M) primarily involved the fine paid to the Chinese authorities.

Net debt currently stands at £14.788, an increase of £2.143BN on the same period of last year. The quarterly dividend has been kept the same this quarter and the expected full year dividend of 80p which represents a yield of 5.5% and the board has signified that they expect to maintain the dividend at this level into next year. Despite the decent yield, there is no doubt that GSK has a lot of issues at the moment, most concerning is the reduction in the Advair sales. The group also seems to be losing cash and it must be possible that the dividend is potentially in trouble if a new blockbuster drug is not found. For the time being, though, I am continuing to hold.

On the 5th November the group announced that it had filed regulatory submissions in the US and Europe for mepolizumab for approval as a maintenance treatment for patients with severe eosinophilic asthma.

On the 4th December the group announced that none of the bids received for some of its Established Products Portfolio were worth pursuing so there goes that idea then.

On the 28th January it was announced that European Commission clearance was received for the Novartis deal. As part of the approval, the group have to undertake certain conditions. The group has agreed to sell its meningitis vaccines Nimenrix and Mencevax on a global basis which generate sales of £36M. In addition, they have agreed to sell their NiQuitin smoking cessation products and Coldrex cold and flu products in the EEA, its local Panodil pain management and Nasin cold and flu products in Sweden and Novartis’ cold sore business in the EEA. These products together generated £109M in 2013.

On the 4th February the group released their Q4 statement. As I am going to start a new thread for the full year results I thought I would do a short update here to cover the latest developments. Overall core operating profits were down by 9% on a constant currency basis compared to Q4 2013. The fall seems to have been driven by US pharmaceutcials, Japanese vaccines and Emerging markets with Europe and Consumer Healthcare showing small growth and ViiV being the stellar performer with profits up 43%. The non-core earnings were much lower due to the fact that the sale of Ribena was included last time and there were some major restructuring charges of £457M. Net debt stood at £14.4BN compared to the £12.6BN last year although cash generation improved in the fourth quarter reflecting working capital improvements and a strengthening US dollar.

The dividend for the year is 80p which represents a yield of 5.3% at the current share price and the company expect to keep this the same next year too. Some of the headwinds facing the group are likely to adversely affect performance during 2015, particularly in the first half but a stronger performance is expected in the second half. Overall, these are difficult times for GSK but there is a decent pipeline and a good yield for the time being so I am holding my shares.

On the 5th February the group announced that it had agreed the sale of its 7.9% stake in Genmab for £194M. Since the divestment of the Oncology portfolio to Novartis, the group consider this stake to be a non-core asset.

On the 6th February the group announced that overall survival results from COMBI-d demonstrated a statistically significant reduction in the risk of death for the combination of dabrafenib and Trametinib compared to dabrafenib monotherapy in patients with metastatic melanoma and no safety concerns were observed. Completion of this study was a requirement for the FDA’s accelerated approval for the combination in the US. The final data will be submitted to regulatory authorities in the coming months. This sounds like a positive result for a product that will be divested to Novartis with the rest of the Oncology portfolio.