James Halstead has now released their final results for the year ending 2014.

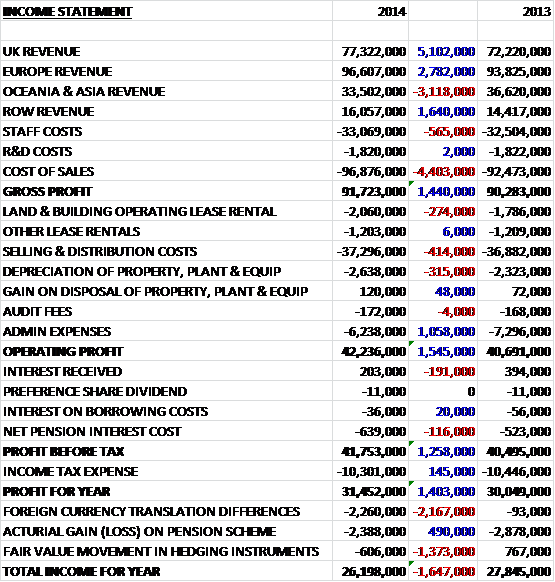

Revenues improved across most regions with UK revenue up £5.1M and ROW revenue up £1.6M, somewhat offset by Oceania & Asia sales which were down £3.1M on last year. Staff costs increased slightly and cost of sales also increased to give a Gross Profit some £1.4M higher than last year. We also saw an increase in depreciation and selling/distribution costs which were broadly offset by a fall in admin expenses to give an operating profit £1.5M higher. An increase in pension costs and a reduction in interest received were counteracted by a slightly lower tax bill and the final profit for the year was £31.8M, some £1.4M higher than in 2013. A steady rather than exceptional performance.

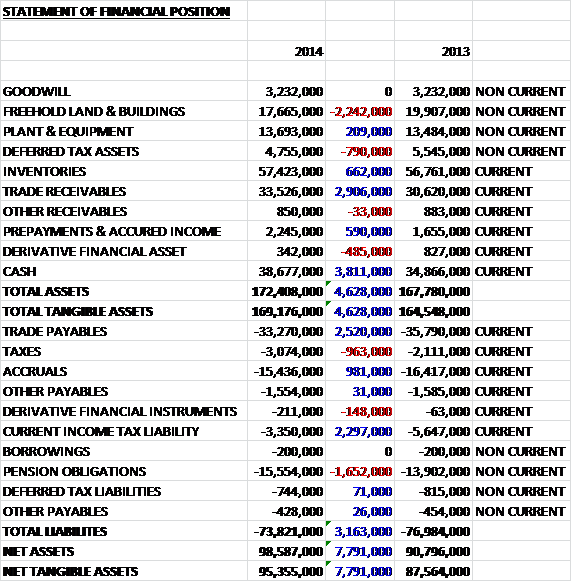

Total assets increased by £4.6M when compared to the end point of last year driven by a £3.8M increase in cash levels and a £2.9M hike in trade receivables, somewhat offset by a £2.2M fall in the value of land and buildings. Liabilities fell £3.2M during the year as a £2.5M increase in trade payables, a £1.3M growth in tax liabilities and just under £1M in accruals were partially offset by a £1.7M increase in pension obligations which gave a net tangible asset level of £95.4M, a decent £7.8M increase over 2013.

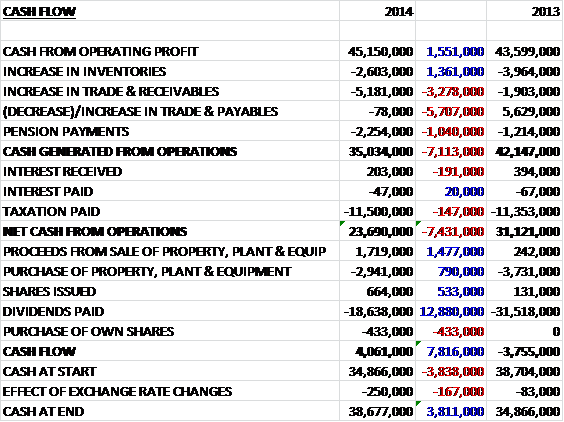

Before movements in working capital, cash profits were some £1.5M higher than in 2013 at £45.2M. Adverse working capital movements, however, particularly a large increase in receivables and a swing to a decrease in payables, along with a £1M hike in pension payments meant that cash generated from operations was £35M, down by £7.1M when compared to last year. An increased tax bill meant that net cash from operations was actually £23.7M, £7.4M lower than in 2013. Of this cash, only £3M was spent on capital expenditure with the purchase of some property, plant and equipment and the group also made £1.7M by selling off fixed assets. The vast bulk of the operational cash flow (£18.6M) was spent on dividends and even there the group enjoyed a £4M cash inflow to give a balance of £38.7M at the year end point. Despite the less than stellar growth this year this company is still throwing off a lot of cash in the form of dividends.

The group has had a good split of different projects and is even active in Iraq where they have supplied flooring to the Baghdad Medical Hospital and General Hospital of Samawa along with temporary flooring for the workers on construction projects in Qatar. In India the group has supplied products to the Aditya Birla Memorial Hospital in Jaipur.

In the Nordic regions sales were on a par with previous years and there has been good progress with the introduction of product manufactured at Teesside. During the year the group have installed the most Northerly Polyflor in the world in Longyearbyen in student apartments. Objectflor in Europe has seen a sales growth of nearly 4% despite a contracting market with slight erosion to margins which has led to a 5% decline in profits at the division, although winning the accolade of “Best Quality Product” at the Domotex exhibition in Germany can’t do any harm. In France the group enjoyed a turnover some 9% ahead of last year and have installed flooring in the Louis Vuitton HQ in Paris and the Monaco government offices and despite the tough market conditions in the country, management expect continued growth in the country.

In China projects for new builds have been buoyant but in Australia and New Zealand these projects have been scarce. Australian turnover was on a par with last year but margins have suffered and profits in the country declined considerably, although margins have begun to recover in the second half of the year. New Zealand did not fare well as turnover fell by 6% with the shortfall felt in commercial sheet vinyl due to the lack of school and hospital projects. This did mean, however, that margins improved as these are low margin products and the group made a modest profit in the country where they have won a three year contract with Housing NZ to supply flooring for social housing.

In Canada the group sold flooring to the Royal Bank of Canada’s retail outlets, the Rogers retail chain and Goodlife Fitness gyms along with larger one-off projects at the new hospital in Montreal, the McGill University Health Centre. The performance in the latter months of the year showed some improvement as emerging markets continue to demand fashion retail outlets which makes this a fast growing sector. The new financial year has continued with positive growth as some confidence has returned to many markets which hopefully can be sustained.

At the current share price, the P/E ratio stands at 18.5 reducing to 17.6 on next year’s forecast which is not too bad considering the big cash pile the group is sitting on. A final dividend of 7p (17% increase) gives a yield of 3.6% rising to 3.8% next year on consensus forecasts which again, is pretty decent. This is not a bad update, with steady profits, an increasing asset base and positive cash flow which is predominantly spent on returns to shareholders but it appears that the group is finding growth harder to come by with some of their markets in the doldrums. A decent dividend yield, however, encourages me to continue holding these share for now, however.

On the 5th December the group released a trading statement covering the first five months of the year. It is expected that this year will be a new record in terms of turnover and profit and so far this year the group are 5% ahead of last year with regards to sales with growth in both the UK and overseas. The half year results are expected to be in line with expectations.

On the 30th January the group released a statement covering the first half of the year. Following the good statement last time, it was confirmed that sales were around 6% ahead of the same period last year. The recent weakness in the Euro is not helpful for their exports but the low price of oil and strong Sterling performance have a compensatory effect regarding input costs. Confidence in the full year is unchanged and remains positive. This sounds good, I have added to my position here.