Safestyle sells, manufactures and installs replacement PVCu windows and doors for the UK homeowner market. The group has now released its final results for the year ending 2013.

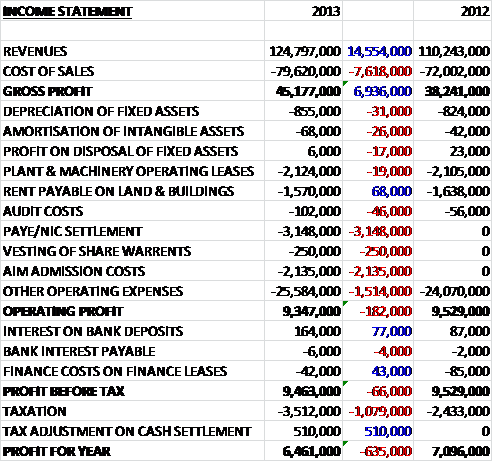

Revenues increased by £14.6M when compared to last year and an increase in cost sales meant that gross profits were up nearly £7M to £45.2M. Operating expenses increased somewhat but the operating profit, down just £182K, was affected by a £3.1M tax settlement and £2.1M of AIM admission costs. The group then made a bit on bank interest and the profit before tax was broadly flat when compared to 2013. There was a higher tax bill this year, though, so the profit for the year was down by £635K to £6.5M, which is not a bad result considering the one-off costs that occurred during the year.

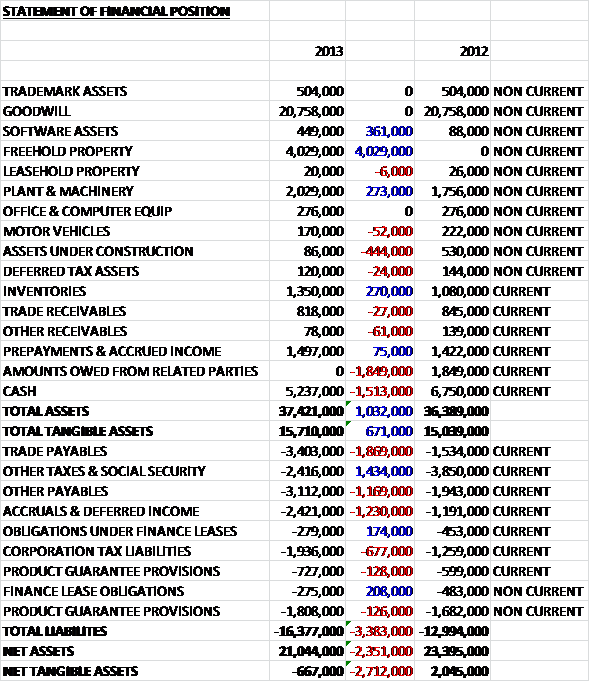

When compared to last year total assets increased by £1M, driven by a £4M growth in the value of freehold property as the group purchased the freehold at the head office in Bradford and the manufacturing facility in South Yorkshire, somewhat mitigated by a £1.8M reduction in amounts owed from related parties and a £1.5M fall in cash. Liabilities also increased during the period driven by a £1.9M hike in trade payables, a £1.2M increase in accruals & deferred income and a £1.2M growth in other payables. This meant that net tangible assets fell by £2.7M to a negative £667K which seems a bit precarious. The chairman suggests the balance sheet is robust but if we take away the goodwill, I do not agree with him.

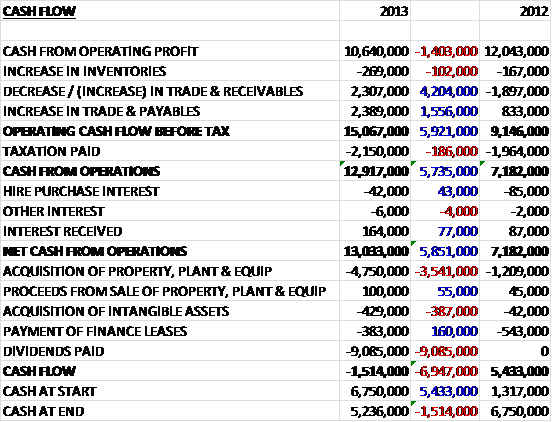

Before movements in working capital, cash profits fell by £1.4M to £10.6M. A beneficial movement in both receivables and payables, slightly offset by a marginally larger tax bill meant that net cash from operations was up £5.9M at £13M. Of this cash, over £5M was spent on capital expenditure with the bulk spent on the acquisition of property, plant and equipment. The remaining cash was spent on £9.1M worth of dividends which took the cash outflow to £1.5M and left the group with £5.2M of cash at the year end. This seems like quite a comfortable cash flow but was flattered by the favourable movements in working capital.

There was a 7.5% growth in the volume of frames installed, a 5.5% increase in the average unit price and a 4.2% growth in average order value. As far as marketing is concerned there is a growing contribution from TV and digital marketing which reduces reliance on canvassing methods after new digital marketing infrastructure was delivered in 2013 that resulted in a 10% improvement in web lead volumes and the cost per lead generated has fallen by 21%. The group has the capability to increase capacity without investing further in manufacturing which should be a good point going forward.

As part of the IPO the group has issued warrants to Zeus Capital for 3% of the total share capital which is exercisable at any time between the 1st and 10th anniversary of the admission to AIM. Another one-off cost is the £3.1M paid to HM Customs to settle a previously unprovided payroll liability. This liability related to 2004/2005 and the directors had previously received advice that they were not liable but the decision was made to settle to avoid a lengthy drawn-out process and to draw a line under the issue as the group joined the AIM exchange.

The group seems to have quite a lot of operating lease commitments on motor vehicles with £1.4M expiring within the year and they are rather exposed to the UK economic performance and that of the housing market. The board see that with improving home owner sentiment, coupled with progress being made within the company they are well placed to see a period of further improvement. Order intake in the first two months of the new year has been strong and there is an encouraging start to the year. Market share increased to 7.85% during the year which actually represents a market leading position in a very fragmented market. The main target is to expand into the South of England.

The group has been making investments in IT infrastructure and manufacturing systems and have completed the first £800K phase of a £1.55M two stage investment to upgrade their PVCu equipment with the second phase scheduled for implementation in 2014 along with further investment in the IT infrastructure. Alongside this, two new sales offices and installation depots have been created in the South East.

At the current share price the 5.5p final dividend represents a yield of 3.2% but based on next year’s forecast this increases to 5.2%. Discounting the one-off costs the underlying P/E is a good value 11.7, falling to 10.9 on next year’s forecast. At the end point of the year net cash stood at £4.7M, a decrease of £1.1M on the end point of 2012. So, after IPO costs and the cash settlement are taken out, the underlying profits improved on last year but if Goodwill is removed then the balance sheet is looking a bit precarious at -£667K and before movements in working capital, cash profits were down but the capital expenditure was easily paid for out of operating cash and dividends were nearly covered which makes me think the spectacular yield is safe. I do think this could be a good investment but am just a bit nervous about the negative net tangible assets.