Photo-Me has now released its interim results for the year ended 2015.

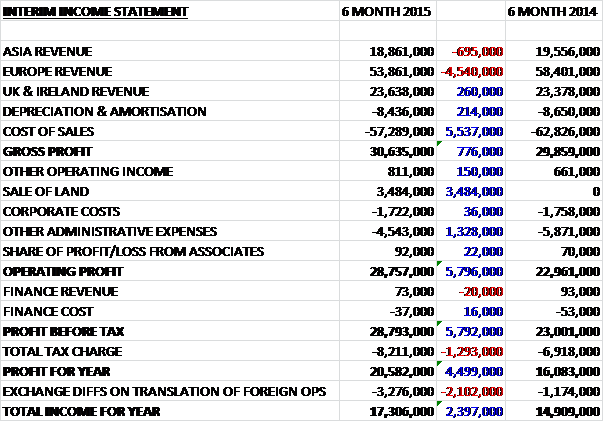

These results have been changed to reflect the new segmental split. Overall revenues were down on the first half of last year with Asian sales falling £700K, European revenues declining £4.5M due to currency issues and the declining minilab business, and UK and Ireland sales increasing by £260K. Cost of sales also fell, however, so gross profit was some £776K higher. Admin expenses fell by £1.3M and there was the one-off profit from the sale of vacant land at the Bookham head office, which was £3.5M and helped profit before tax increase by £5.8M before a higher tax bill meant that the profit for the half year was some £4.5M higher than the same period of last year at £20.6M. Underlying pre-tax profits increased by 10% to £25.3M. It is worth noting that the first half of the year is traditionally strongest for the group in terms of profits.

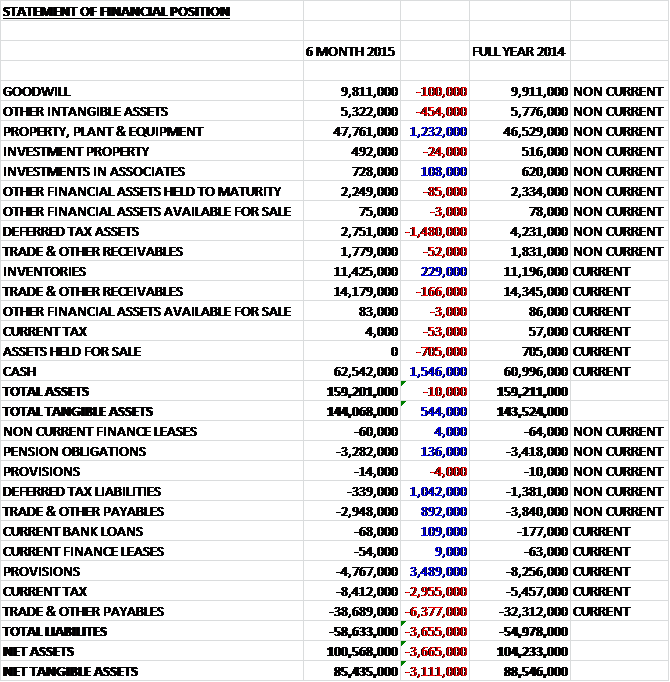

When compared to the end point of last year assets remained unchanged as a £1.2M increase in property, plant & equipment and a £1.5M increase in cash was counteracted by a £1.5M fall in deferred tax assets and the elimination of £705K of assets held for sale (obviously moved into cash). Liabilities, however, increased during the same period as trade and other payables increased by £6.4M and current tax liabilities were up £3M, somewhat offset by a £3.5M decrease in provisions and a £1M fall in deferred tax liabilities. Overall, this meant that net tangible assets decreased by £3.1M to £85.4M.

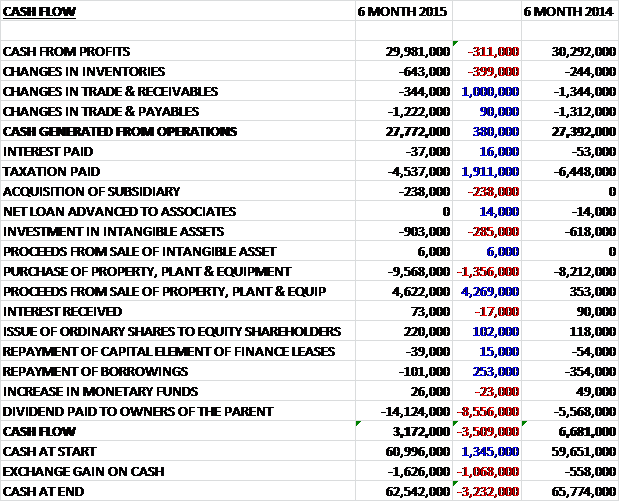

Before movements in working capital, cash profits were down £311K to just under £30M. After working capital was taken into account, however, the cash generated from operations was £27.8M, a £380K improvement on the first half of 2014. Somehow, the group managed to pay nearly £2M less in tax but spent more on capital expenditure (£900K on intangibles and £9.6M on tangible assets). There was small acquisition at £238K and the sale of land netted £4.6M in cash to the group which helped it to a £3.2M cash inflow after £14.1M was paid in dividends. Had the group not sold the land, dividends would not quite be covered by considering there was a £62.5M cash pile at the end of the half-year, this is not really a concern at the moment.

Asian and ROW underlying operating profits were £3.5M, an increase of £1.2M compared to the first half of last year. The group now operates in eight countries with the latest additions being Vietnam and the US with testing ongoing in Thailand. The bulk of the profits in this division are made in Japan and these were 50% higher on a constant currency basis. The outlook in the country is good as the Government is introducing new e-ID cards for every resident in Japan from 2016 which could use photos from the group’s booths. There will be a trial of two laundry units in Japan in early 2015 as the region is seen as a promising market for the machines. Gradual progress was made in China where sales rose 40% on a constant currency basis but the roll-out has been slowed down as the group re-sited unprofitable units to better locations which halted the losses from the country that occurred last year.

Europe operating profits were £18.4M, an increase of £200K when compared to the first half of 2014. The relative poor performance was due to adverse currency movements. The photobooth estate increased by 5% year on year with the main growth areas being France, Germany and Switzerland with the higher margin Starck booths increasing to 2,118. The roll-out of the laundry product continued to progress well and at the end of the period the group had sold 370 units (53 during the period) and operated 374 (an increase of 172). The results from the units in France and Belgium were decent and for the more established machines, takings increased by 22%. During the period, sales at the laundry business unit were £2.9M, an increase of £1.3M.

The laundry units are being pushed into Portugal and Ireland and the gradual expansion of manufacturing capacity in Hungary is going to plan. The group also has a new design for the Starck kiosks which is expected to be launched next year and a new chrome finished Starck photobooth has been developed for higher end locations. Work continues on the 3D figurine photobooth, which sounds intriguing, and an upgraded poster machine. Additionally, the group is trialling a carwash concept, initially targeting Carrefore supermarket sites and will report further plans for the concept in 2015.

UK and Ireland operating profits were £5.1M, an increase of £800K when compared to the first half of last year. The growth in photobooth numbers was 5.7% year on year while there was a 29% reduction in amusement machines which do not generate much revenue. The growth in profits from the photobooths was partly as a result of the absorption of the Morrison estate into the portfolio. There were 32 laundry units in operation at the end of the period, 18 of which were in Ireland and initial results are apparently promising.

During the period the group acquired Copyphot, a small company operating photobooths in Switzerland. The group paid £402K in cash for £402K of net assets which seems a good deal to me. The momentum in the business as a whole is good and it is performing in line with expectations. The board are confident for the outlook of the business over the rest of the year and remains optimistic about future prospects, especially in relation to the opportunities for the laundry business.

An interim dividend of 2.34p per share, representing a 30% increase, was declared which, not including any special dividends, give a yield of 3%. The group ended the period with a staggering £64.7M of net cash compared to £63.1M at the end point of last year. Underlying profits were up overall, and would have been even higher had the currency movements been more favourable but net assets fell due to an increase in trade and payables, perhaps as a result of seasonable changes. Before working capital movements are accounted for, the cash profits fell slightly on the same half of last year but here is still plenty of cash for the capital expenditure requirements with the rest spent on dividends. There remains a huge cash pile and the new products offer decent growth prospects, it is also good to see China achieve a profit. This company represents my largest holding and given the slight stutter in operational cash generation I am not buying more but I am happy to hold all the shares I have in anticipation of further growth and more special dividends.

On the 14th January it was announced that Schroders sold 648,530 shares worth about £1M to leave them with just under 18% of the total share capital. It is a shame to see them selling but they retain a large holding and unless there are any further shares, this is still quite an endorsement in the company.

On the 26th February the group announced a trading update covering Q3. Profit before tax in the quarter was 12% ahead of the comparative figure last year and if reported at a constant currency basis, was even stronger, increasing by 19%. Turnover at a constant currency basis rose by just 3% so on a reported basis that probably fell again. The roll out of the laundry product continued to progress well with a total of 898 units deployed so far with the group apparently on track to deploy about 2,000 by the end of 2015. The expansion of the manufacturing capacity progressed with a second production line operating in Hungary since mid January. The results from France and Belgium saw machines that had been in operation for more than a year increase turnover by 21% year on year. Ireland and Portugal have also been targeted with 45 machines now in operation there with Ireland delivering the highest average monthly turnover per machine of any country with the machines being located on petrol stations and near campsites.

The group is also trialing 25 new Starck booths which incorporate a 3D figurine photobooth which it plans to launch in the second half of 2015 – not much use for passport photos perhaps but quite an exciting novelty product nonetheless. The carwash concept trial is continuing at five sites and has already received strong interest from a supermarket chain in France. The group remain optimistic that the concept can be rolled out with a further report at the final results stage. Despite the strengthening of Sterling against the Euro in particular continuing to provide headwinds, management are confident of delivering results at least in line with expectations for the year and is committed to a 30% increase in the total dividend for the current year. This is all good, exciting stuff and I am confident to keep holding what is my largest holding.

On the 21st May it was announced that Norges Bank had sold 374,199 shares at a value of about £533,196 to take their holding down to under 3%, which is a shame.