Red24 has now released its interim results for the year ending 2015. The group is now organised as a single unit so profits are measured geographically which is a bit of a pain. They have still published revenue figures split by sector, though, so I have used those here.

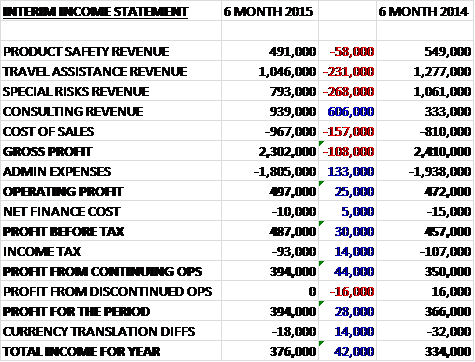

Overall revenues increased with as a £606K increase in Consulting sales was partially offset by declines in all other sectors. Cost of sales also increased, however, to drive gross profit down by £108K. Admin expenses declined from last year, however, to reverse the fall in gross profit and at the operating profit level, the result was some £25K higher. Small reductions in finance costs and tax payment (as less profits were made in South Africa) meant that the profit from continuing operations was £395K, a £44K improvement on last year and a £28K improvement when the profit from discontinued operations is added on to the 2014 results.

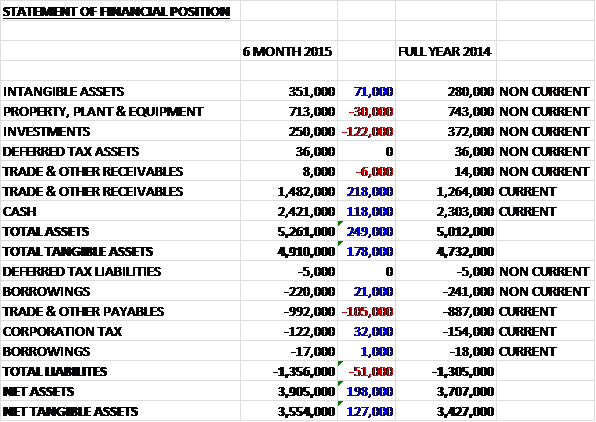

When compared to the end point of last year, total assets increased by nearly £250K driven by a £212K increase in trade and other receivables and a £118K growth in cash levels, somewhat offset by a £122K reduction in investments as the group sells part of its stake in Linx. Liabilities saw a small increase due to a £105K growth in trade and other receivables, somewhat offset by small falls in various other liabilities to give a net tangible asset level of £3.6M, an increase of £127K over the past six months.

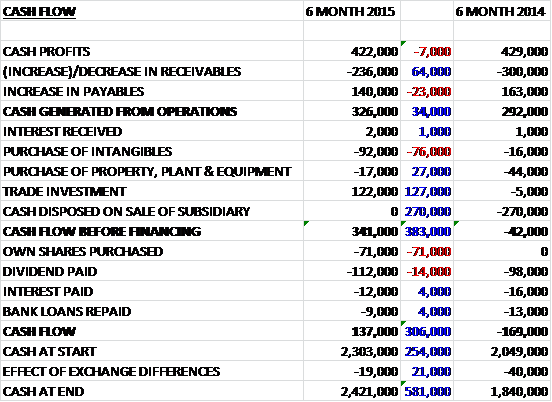

Before movements in working capital, cash profits were only £7K lower at £422K but a smaller increase in receivables than during the same period of last year meant that cash generated from operations was £34K higher at £326K. The group spent £92K on intangibles and £17K on tangible assets but this was paid for by a £122K cash inflow relating to the sale of part of the stake in Linx so before financing, free cash flow was a healthy £341K. The group spent £71K on share purchases and the bulk of the rest of the cash was spent on dividends with the resulting cash inflow of £137K a £306K reversal on last year which is a fairly pleasing result.

UK profits were £324K, more than double the £152K figure recorded during the same period of last year. South Africa profits fell by £133K to just £62K during the first six months of this year. US profits, at just £8K, are modest but they did increase by £5K. Travel assistance maintained revenues during the period but this is the revenue stream that will be most severely affected by the exclusion of the identity theft service that was given to HSBC. The Special Risk business has been fairly busy so far this year with a larger number of smaller crises while the newly opened Munich office is meeting expectations, although revenues suffered somewhat due to the lack a major incident in Syria that occurred last year. Consulting revenue has been excellent so far this year as demand for both close protection and evacuation planning services has increased with a Far East client needing a large evacuation of several hundred staff from North Africa. The product safety business showed a decline in revenues despite the launch of an analytical tool and new training modules, possibly reflecting a maturing market.

There were contract wins to support business travel clients in Oceania and to support medical assistance clients in North America which will help mitigate the debilitating loss of an HSBC contract which will have an adverse effect on the level of recurring revenues in the second half of the year and beyond, although the board are confident about the ongoing prospects for the business. It would be useful to know some background on why the bank has decided to stop taking the identity theft service and while the board see their offering as in tune with customer demand rather than the more “compensatory” approach from their competitors, this was obviously not the case for HSBC.

There has been a hint from management that they may be on the lookout for acquisitions, particularly in overseas markets so this could be something to keep an eye on. Going forward, the group are winning a number of new contracts and seeing steady growth in response work on existing contracts but apparently the UK regulatory environment is not conducive to their customers releasing new financial services. Despite this, however, the board see a recovery from the loss of the HSBC contract as fairly speedy.

Lorraine Adlam has joined the board as a non-executive director. She has worked with high growth companies in the insurance markets in the past and was previously Chairman at Howden Insurance Brokers. She should be able to identify new opportunities. A small increase to the interim dividends means the shares are yielding 3.4% at the current share price, increasing to 3.7% on next year’s estimate.

Overall then, we see a small profit increase but only due to the good performance from the consulting business as the other sectors seemed to struggle, net assets increased due to a hike in receivables and operating cash flow was up due to a better control of working capital. Indeed, the cash flow was pretty good with spare free cash flow at the end of the period. The group are obtaining cash from the sale of the Linx investment in instalments but I can’t seem to find a total receivable from this deal. The main issue during the period, however, is the loss of the identity theft HSBC contract which will really kick in during H2 and continue in to next year. Until there is evidence that the group can replace this lost revenue, I find it hard to contemplate buying in here so I will continue to monitor the situation.

On the 11th February the group released a trading update. They stated that prospects improved over recent months with a number of new business wins and a busy quarter for operational responses in the special risks area. As a result the board now expects the company’s financial performance for the year to be ahead of current expectations with a similar momentum expected to be carried into the new year. The enhanced travel tracker product will be launched at the business travel show later in the month. The product enables clients to monitor and track their travelling personnel on a 24/7 basis and is expected to lead to a growing number of opportunities. I like this update and have decided to use it as a trigger for buying some shares. I could probably wait a few days and get them slightly cheaper but I don’t want to miss out!

On the 27th April the group released a trading update covering the year to 2015. Trading in the latter part of the year continued to improve, particularly in the consultancy and special risk sectors, which means that financial performance for the year as a whole will be ahead of expectations. The loss of the HSBC contract announced previously has been mitigated by reduced costs and new contracts with both new and existing clients. There has also been a significant increase in the year end cash balance with net cash of £3.2M, achieved through improved working capital management and the improved trading performance. The current year has started well with new contracts with insurers in both the product safety and special risk areas. The enhanced travel tracker product has been well received and the board expects growth in sales of the product in the coming year. Recent sales in Germany and Australia have also exceeded expectations and this trend is expected to continue.

This is a very positive statement that gives me confidence in my holding here.

On the 1st June the group announced the acquisition of RISQ Worldwide from Michael Haughey for an initial consideration of £267K which could increase by £485K depending on the performance of the acquired group in 2016 and 2017. RISQ has been established for eight years and has offices in Singapore and Hong Kong. It specialises in corporate investigations, business intelligence, employment background screening and bribery act compliance. Going forward, Michael will sat on and head the group’s business in Asia. Last year, RISQ posted an operating loss of £170K on revenues of £679K but in the current financial year, the performance has improved and the group is in a profitable position with a number of new contracts with blue chip clients which should further enhance earnings.

The group has a significantly different product range which should provide a good opportunity for cross selling that should improve the performance of both businesses and will give Red24 an established presence in the Asia market. Overall then, this seems like a fairly decent acquisition at an affordable price.