Compass has now released their full year results for the year ending 2014.

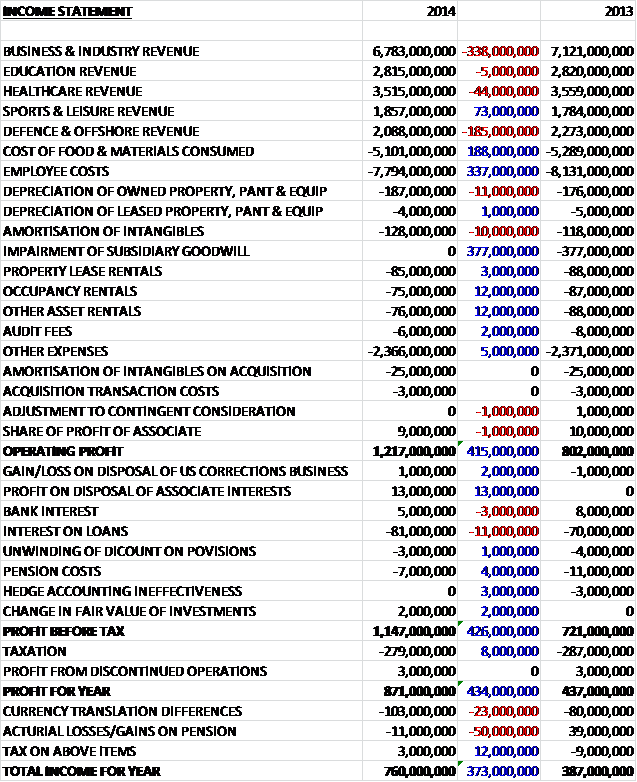

Revenues across most business sectors fell with Business and Industry down £338M and Defence & Offshore falling £185M. The only sector to increase sales was Sports and Leisure, up £73M, although it should be noted that this predominantly shows the effect of Sterling strength as constant currency revenues were 4.1% (2.1% like for like growth) ahead of last year. Some major costs also fell with the cost of food and materials down £188M and employee costs some £337M lower. This year also benefited from the lack of a £377M goodwill impairment that occurred in 2013. This all meant that operating profit was some £415M higher than last year with the profit for the year £434M higher at £871M which was flattered by last year’s goodwill impairment but still higher on an underlying basis.

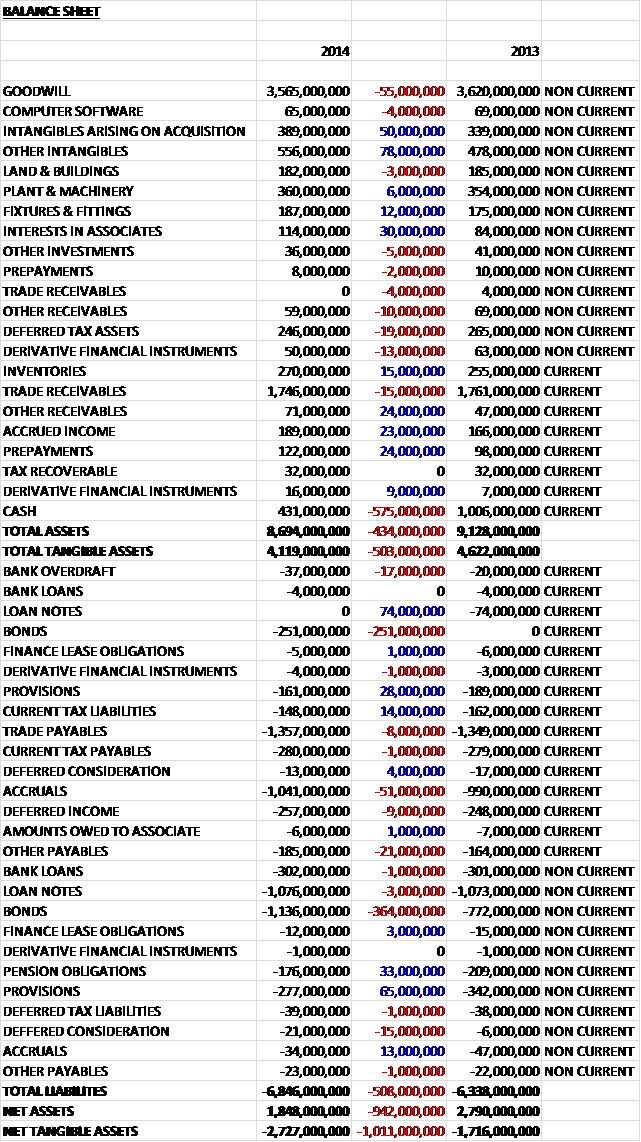

When compared to last year, assets fell by £434M driven almost entirely by a £575M reduction in the cash levels, partially offset by some increases in the value of tangible assets. Conversely, liabilities also increased driven by a more than £600M increase in bonds, offset by a £65M fall in provisions. This meant that net tangible assets collapsed by over one billion pounds to a negative £2.727BN which seems a bit precarious even for a company of the stature of Compass.

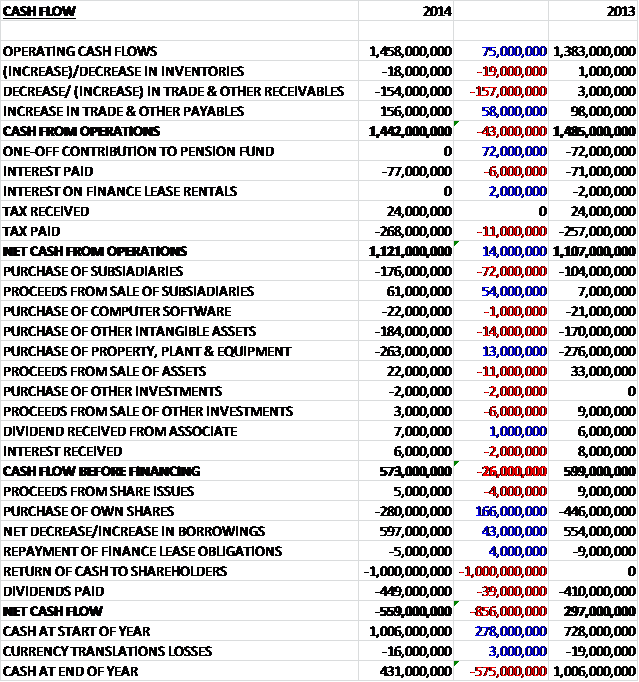

Before movements in working capital, cash from operations was £75M higher than last year but this was reversed by an increase in receivables so that after working capital movements, operating cash flow was £43M lower. Tax and interest reduced this further but the lack of a one-off £72M payment to the pension scheme that occurred last year meant that net cash from operations at £1.121BN was £14M higher than in 2013. A net £115M was spent on acquisitions, just over £200M on intangible assets and a net £241M was spent on tangible assets. This left a free cash flow of £573M. The bulk of this was given back to shareholders, in total £1.449BN was returned and another £280M was spent on share buy backs which is expected to complete during 2015. Clearly this is much more than the free cash flow so the group took out another £597M in new loans which still left a cash outflow of £559M. I am not sure I really understand the rationale of taking out new interest baring loans to return cash to shareholders.

Before exceptional items, operating profit at the North American business was £666M, an increase of £9M on the previous year or £49M on a constant currency basis. During the year continued progress on efficiencies and leveraging of the overhead base have partly been reinvested in the business to support organic growth. In the Business and Industry sector, there were good levels of new business wins including contracts with Amazon.com, T Mobile and SAP as well as the provision of support services to United Technologies – like for like volume remained flat. Organic revenue growth in the Healthcare sector was solid with good levels of new business wins. In the food service business there were new contracts with the Parkland Health and Hospital System and Baptist Housing senior living in Canada. New support service contracts included NYC Health and Hospital and the CJW Medical Centre.

Good organic revenue growth in the Education sector was driven by increased participation and new business wins including food contracts with McGill University in Canada, Rowan University and the Rochester City Schools District. New support services contracts included the Sacred Heart University as well as the provision of additional services to Texas A&M. The Sports and Leisure business delivered double digit organic revenue growth due to good new business and high attendances at sporting events. New contract wins in this sector included the NHL’s Phoenix Coyotes, the Columbus Clippers and Texas A&M Athletics. The service business to the remote sector delivered decent organic revenue growth.

There is a good pipeline of contracts across all sectors but the growth of the business is supported by the retention model where a semi-independent team takes a pre-emptive approach to retaining contracts by engaging with clients early and proactively negotiating contracts and in North America, where this approach has been embedded, retention rates are above the group average so this process will be further rolled out across the other territories.

Operating profit before exceptional items at the Europe and Japan business was £409M, a fall of £11M on last year. There has been good levels of new business in the UK, Spain and across the Nordics but the planned exit of some uneconomic contracts have impacted retention rates during the year. A new contract was won with the Ville de Cannes and the Philharmonie de Paris and contracts with Chelsea FC and Somerset House were retained in the UK. Other retained contracts include ENI in Italy, Lundbeck in Denmark and the International School of Luxembourg.

The rate of like for like volume decline slowed compared to last year but the group has seen differing trends across the region. In North East Europe, like for like volume is broadly flat but in the UK, Germany, the Netherlands and Southern Europe, volumes were negative. Meanwhile, there has been some pressure on volumes in France and Italy but Japan remained unchanged. Progress on efficiencies and cost reduction helped combat some of these volume falls and on a constant currency basis, operating profit actually increased by £5M.

Before exceptional items, operating profit at the Emerging Market business was £226M, a decrease of £16M on 2013. In line with expectations, Australia delivered flat organic revenue growth due to the slowdown of the offshore and remote sector. In contrast, Education and Healthcare continue to see good levels of new business with a contract win with Children’s Health Queensland to provide services at the Lady Cilento Children’s Hospital. In Brazil, there were good new business wins across all sectors including food service contracts with Usiminas and Vale. Moderate pressure on volumes is being compensated by improved retention and an increase in first time outsourcing. Elsewhere in Latin America there has been good organic growth driven by several large new offshore and remote site contracts, including Bechtel in Chile.

Strong organic revenue growth in Turkey was driven by new business wins and like for like revenue growth. New contracts included the food service provision for Aksa, a food and support service contract with BP along with the retention of Philip Morris and Bosch. Elsewhere in the region the group have further developed their relationship with Chevron and have a freed a new international agreement, retaining the Angolan business. There was also a large contract win in South Africa to provide food to Netcare, a chain of 52 hospitals. India and China both delivered good double digit growth driven by strong new business wins. The group won food service contracts with Intel and Capgemini in India and with Lenovo and Tencent in China as well as several international schools including the International School of Beijing.

In May the group disposed of its retail cleaning business in the US. It was sold for £31M, with £24M received in cash at the time of the sale which generated a loss of £1M. The group completed a number of small acquisitions during the year on which they spent £138M, of which £107M was spent during the year and the newly acquired companies contributed £3M to profits. After the end of the balance sheet date the group acquired East Coast Catering, a Canadian company that provides accommodation, food and support services for remote sites in the energy and mining sector. The acquired group generated revenues of £28M last year.

The group can be susceptible to general economic conditions as like for like volume and therefore organic revenue growth can depend on the number of people at the client’s site. The group concentrates on the largest costs, the cost of food that makes up one third of costs and labour, which makes up the bulk of in unit costs. This year, organic revenue growth sat at 4.1%, the lowest percentage for at least three years but still fairly decent. Although the historic litigation relating to the supply of UN contracts it is worth considering that litigation involving the group’s competitors over the matter is still ongoing.

During the year Carol Arrowsmith joined the board as a non-executive director. She was previously a partner at Deloitte and Vice Chairman of their UK business. The other addition was Paul Walsh who succeeded Roy Gardner who retired as Chairman.

Looking forward, the pipeline of new contracts is healthy and the board expect to see further good performance in all regions. As far as investment is concerned, the group are looking to invest cash in growing organically, returning cash to investors and to invest in small to medium sized infill acquisitions. It was also pointed out that due to a full year of the higher debt levels, finance costs for next year are likely to be around £115M compared to loan interest of £81M this year.

Quality doesn’t come cheap and at the current share price the shares trade on a P/E ratio of 22.6, falling to 20 on next year’s estimates. At the current share price, after the total dividend was increased by 10.5% the yield stands at 2.4%, rising to 2.6% on next year’s estimate as the group look to grow dividend in line with constant currency earnings. Net debt at the end of the year nearly doubled to £2.331BN. So, this was a solid year for the group. Although the headline profit figures were down, they were up slightly on a constant currency basis with the North American business performing particularly well. I don’t fully understand the logic of taking out new bonds just to return cash to the shareholders, I believe this would have been better provided out of free cash flow as and when it becomes available, so that was disappointing. The values are also fairly full but this share acts as a bit of ballast to my portfolio so while I will not be buying any more I am certainly holding on to my shares for the time being.

On the 5th February the group announced a trading update covering Q1. Organic revenue grew by 5.7% with strong levels of new business and good retention rates across all regions. North America had a strong start to the year with the trends seen in the second half of last year continued into the first quarter of 2015. There were good levels of new business wins, unusually high retention rates and an improvement in like for like sales in some sectors. Europe and Japan returned to growth, driven by good new levels of new business wins and better retention and like for like revenues, whilst still negative, are improving. Emerging markets enjoyed double digit organic growth as a continued trend to outsourcing counteracted volume pressures in some countries due to poorer economic outlooks and an expected decline in the Australian offshore and remote sector.

Although sterling weakened against the dollar in the quarter, it continued to strengthen against many other important currencies such as the Euro, Yen, Aussie Dollar and Brazilian Real. In all, currency movements had a negative translation impact on revenues to the tune of £40M and profits by £2M. Going forward, management maintained their positive expectations for the full year but the economic outlook is uncertain in some of their markets and the lower oil prices may impact the offshore and remote business. Overall, though, this is a good outlook and gives me confidence to keep holding my shares, which have performed very well recently.

On the 6th February it was announced that Chairman Paul Walsh had purchased 5,000 shares at a value of £56,650 and he now owns 16,411 shares in the company.

On the 25th March it was announced that another director purchased shares, this time non-exec Carol Arrowsmith purchased 3,342 shares at a value of about £40K. She now owns 7,438 shares in the company – it is good to see another director buying up shares.

On the 30th March the group released a trading update. So far in the first half of the year, organic revenue grew by 5.5% and operation profit margin improved by about 10 basis points. In North America, there was a strong first half with organic revenues up around 8% with a good amount of new business wins and unusually high retention levels with some improvement in like for like revenues. It is expected that operating margin will increase by 5 basis points in the region. Europe and Japan returned to growth despite a mixed economic backdrop across the region with the performance reflecting increased focus on organic growth and the investments made in the sales and retention teams. Organic revenue growth is likely to be around 0.5% reflecting improving levels of new business wins and retention with recovering (but still negative) like for like volumes. Due to the continued focus on efficiencies it is expected that operating margin will improve by around 10 basis points.

In the Emerging region, strong levels of new business wins in emerging markets are expected to deliver around 14% organic growth which should offset the decline in the Australian offshore and remote sector with organic growth in the region as a whole expected to be about 8%. Due to the weakness in like for like volumes in some markets and the pressures in the offshore and remote business, it is expected that operating margin in the region will decline by around 10 basis points. During the period, Sterling weakened against the Dollar but appreciated against most of the other key currencies which when taken together should have a positive translation impact of £35M on revenue and £5M on profit for the half year. If these rates continue for the rest of the year, foreign exchange translation would benefit full year revenues to the tune of £323M and profits by £31M. Going forward, expectations for the full year remain positive but the economic environment in some of the emerging markets is uncertain and lower commodity prices are impacting the offshore and remote business. Despite this, there is a good pipeline of new contracts and the continued focus on organic growth and efficiencies gives the board confidence in achieving another year of delivery.

All good stuff, I am surprised the foreign currency translation is so positive and the improvement in margins in Europe is good to see. I am very confident holding these shares at this point.