International Greetings designs, manufactures and distributes gift packaging and greetings, stationary and creative play products and has customers around the world, with Walmart being a major one. It is worth considering that a portion of the group is owned by non-controlling interests with the directors and their immediate relatives having an interest in nearly 50% of the voting rights, and this year their interests accounted for £718K of profits. They have now released their final results for the year ending 2014.

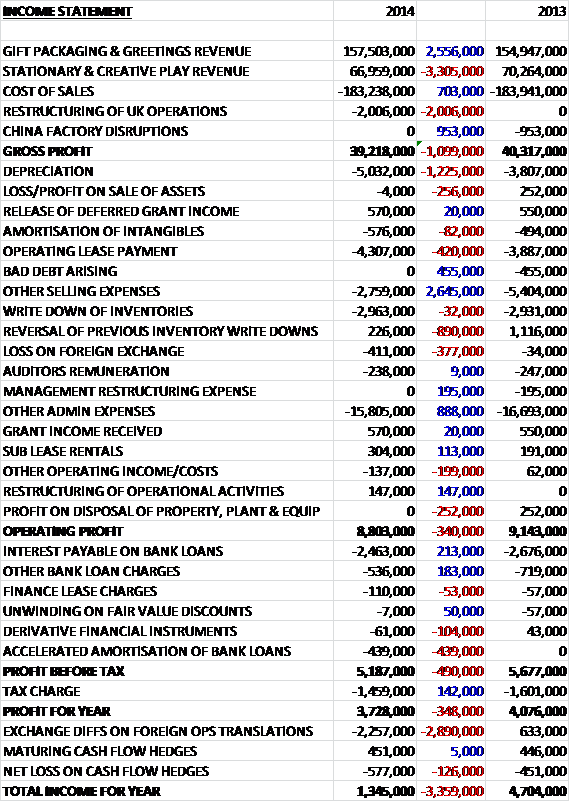

Overall, revenues fell when compared to last year as a £2.6M increase in Gift Packaging and Greetings sales was offset by a £3.3M decline in Stationary and Creative Play turnover but on constant currency basis, revenues actually increased by 0.4%. Cost of sales fell slightly and the £950K charge for the Chinese factory disruptions due to a strike did not repeat, although there was a £2M charge for the restructuring of UK operations including a major upgrade to the Wales factory (the bulk of which is accelerated depreciation on redundant assets and only £800K is to be paid out in cash for redundancies), to leave gross profit some £1.1M lower than last year, although when the one-off costs are discounted, it was broadly the same as in 2013. Depreciation and operating lease payments increased but there was no bad debt arising, and other selling expenses fell by £2.6M. Compared to last year, some non-cash items were lower as the reversal of previous inventory write downs fell by £890K and the loss on foreign exchange increased by £377K but other admin expenses fell by £888K which couldn’t prevent operating profit falling by £340K. As far as finance costs were concerned, loan interest and tax payments fell, offset by a £439K accelerated amortisation of bank loans to give a profit for the year of £3.7M, a decline of £348K compared to 2013.

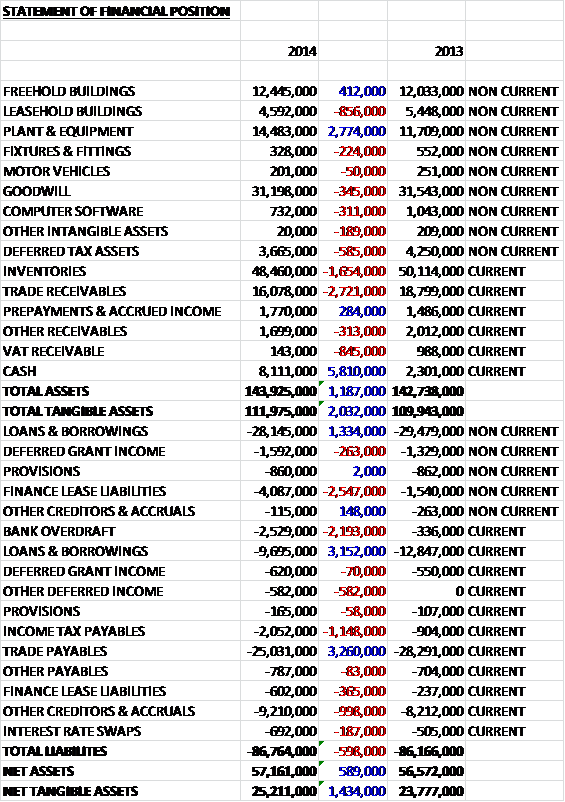

When compared to last year, total assets were just £1.2M higher driven by a £5.8M increase in cash levels and a £2.8M growth in the value of plant and equipment. These increases were partially offset by a £2.7M fall in trade receivables and a £1.7M decline in inventories. Liabilities also increased as finance lease liabilities were £2.9M higher due to two new finance leases being entered into to fund new printing machines in Wales, income tax payables were £1.1M lower and other creditors and accruals fell by just under £1M, offset by a £3.3M reduction in trade payables and a near £1M fall in borrowings so give a net tangible asset level some £1.4M higher at £25.2M, although it is worth noting that there are £21.8M worth of operating lease payments not on the balance sheet.

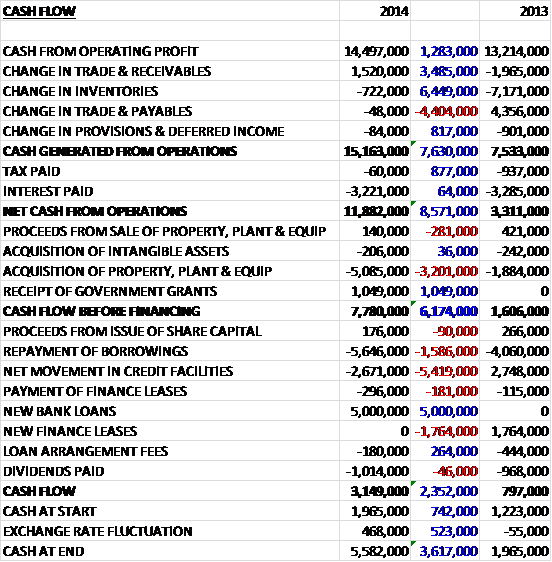

Before movements in working capital, the cash from profits was £14.5M, £1.3M higher than last year. A tight control on working capital, particularly a fall in trade receivables meant that cash from operations increased by £7.6M to £15.2M. After a nominal amount of tax was paid due to the Australian business taking tax relief against last year’s write off of bad debt and some £3.2M in interest, net cash from operations came out at £11.9M, an impressive increase of £8.6M. The bulk of this cash was spent on the acquisition of property, plant and equipment (£5.1M, an increase of £3.2M) and the group benefited from a £1M government grant to give a free cash flow £6.2M higher at £7.8M. The group uses much of this cash to pay back loans, with £646K spent on net borrowing repayments and £2.7M in credit facility reductions. The rest, just over £1M, was spent on dividends to give a cash inflow of £3.1M which is a very decent performance.

Before exceptional items, profits in the UK were £3.5M, a fall of £500K when compared to last year. During the period the group completed an upgrade to their printing capability in Wales which was completed on time and within budget. This investment will result in a consolidation of their three operations there and it is expected that one of those sites will become available for sale with a net book value of £1.25M. The group also completed investments at their facility in China including semi-automated processes for cracker manufacturing and enhanced production capability in gift bags. During the year the group withdrew from a non-core product category in generic books under the Alligator brand in order to focus on the larger licensed product segment. Growth occurred with online customers in the UK, including Ocado and Amazon.

European profits were £2.6M, a £1.4M increase when compared to 2013 this was despite a difficult market and having established relationships with the 10 largest retail groups in the region, the group are looking to expand further. In Mainland Europe the they enjoyed record volumes despite the difficult overall market conditions as they increased their market share, helped by the new equipment installed last year in the Netherlands. Profits in Australia were £2.1M, a £300K reduction on profits before exceptional items in 2013 as last year’s investment in the logistics facilities in the country was somewhat undermined by the slowdown in the Australian economy.

USA profits were £3M, a decline of £800K when compared to last year. This fall was due to very difficult trading conditions in Q4 due to the extreme weather that occurred in the country during that period. Until that point, trading was at record levels in the region as sales developed well throughout the year. The knock on effect of the weather meant that higher margin every day product sales in the US were largely rescheduled and below expectations. The company invested in some automated case packing equipment in their Savannah operation which became fully operational in Spring and should enhance production efficiencies.

No customers accounted for more than 10% of total sales which is good to see and there are still £2.2M of unused tax losses in the US and £300K in the UK which will keep tax below the rate it should be for some time, although it is worth noting that as these are used up, the tax bill is likely to increase. One risk that affects the company is that the business remains highly seasonal with more than half of profits made around the Christmas period so a poor performance around this time would have a devastating effect on the group’s prospects for the full year.

This year some 56% of revenue was made on Christmas products and they increased by £5.8M compared to 2013. Meanwhile everyday product revenue fell by £6.5M compared to last year which was the same overall trend that occurred in 2013 when compared to 2012. In the future the group intends to improve margins by increasing the balance of own brand and non-Christmas products. Another effect on margins is the increasing level of FOB business delivered direct to customers at Chinese ports, especially to US and Australian clients. This business has lower gross margins than the more traditional offering but is a way to drive volumes and reduce risk and costs associated with delivery which can actually improve net margin.

After the end of the balance sheet date the group announced that it had acquired the trade and certain of the assets of Enper Giftwrap for €1.9M. Enper is a giftwrap manufacturer in the Netherlands with sales of €5M and the acquisition will allow the group to widen its customer base in a core product category.

Sadly during the year, CEO of the US operations, Rich Eckman passed away after a battle with cancer, he was with the company for 14 years. Going forward, having completed the first year of a new three year plan, the board expect to achieve double digit cumulative average growth in earnings per share, they are reducing debt and apparently have identified opportunities to grow.

At the current share price, the P/E ratio stands at a decent 14.2 but based on next year’s prediction, this ratio falls to a very cheap 8.1 but there were no dividends announced for the year however when leverage is reduced from the current 2.4 times EBITDA to 2 times, the board will consider re-introducing dividends. At the end of the year, net debt stood at just under £37M, an improvement of £5.1M compared to last year with about £1.4M of this down to weaker exchange rates. Overall then an OK set of results. Profits barely moved but this seems to be largely due to adverse weather in the US and the impact of investment in the factory in the UK, which should benefit the group going forward. Operational cash flow is strong, and it is good to see this being used to play down debt, which is still quite high. Whilst decent progress is being made here, I am not going to buy just yet and will hold of for further news.