Vertu Motors owns and operates a number of vehicle dealerships, the group also sells used vehicle warranties which are in house products that can be taken out over 12, 24 or 36 months with income received at the start of the policy and initially recognised as deferred income. They have now released their final results for the year ending 2014.

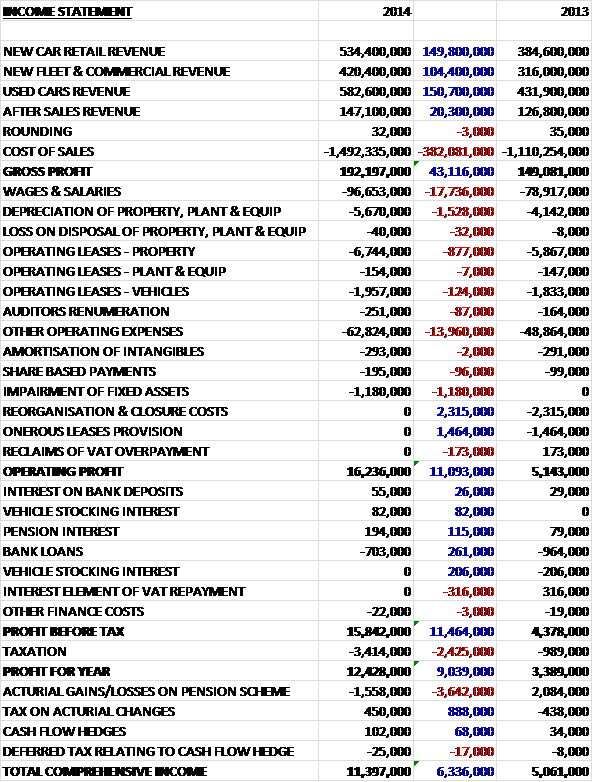

Revenue was up considerably across all sectors and cost of sales increased to a lesser degree to give a gross profit some £43M higher. Operating costs also increased with staff costs increasing by £17.7M due to increased commissions from improved profitability, increased headcount to take advantage of higher demand levels and further investment in contact centres and central functions to support the group’s growth. Other expenses were up nearly £14M, partly as in line with other retailers, the group experienced increased occupancy costs such as rent and rates. There was a one-off impairment of fixed assets relating to four vacant properties, which cost the group £1.2M but this was offset by the lack of £2.3M of closure costs and £1.5M in onerous lease costs that occurred in 2013. Overall, operating profit was up £11.1M which is a good performance. As would be expected, tax was higher but finance costs fell, mainly due to lower interest charges so that the profit for the year stood at £12.4M, a remarkable increase of £9M when compared to last year.

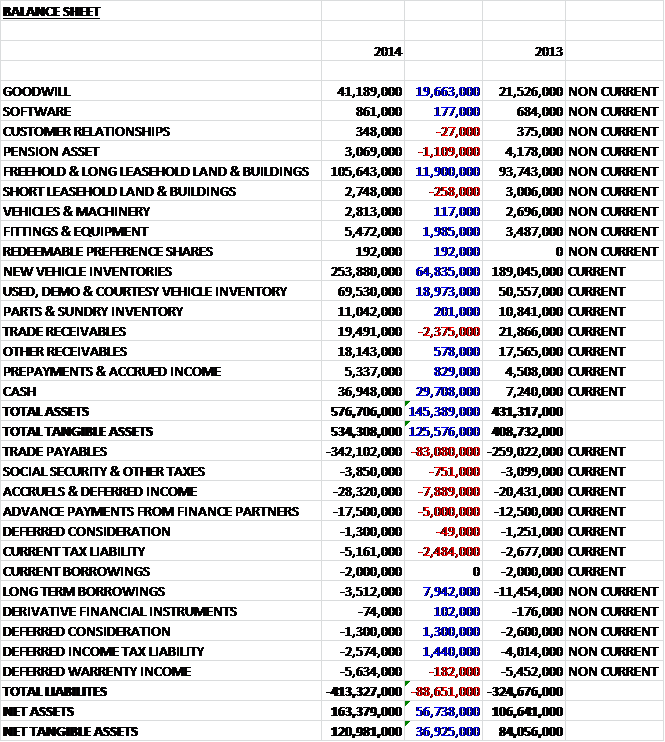

When compared to the end point of last year, total assets increased by £145.4M. The increase was driven by an £83.8M increase in inventories, a £29.7M growth in cash levels, a £19.7M hike in goodwill and an £11.9M increase in freehold buildings, partly due to the group purchasing the freehold of two leasehold properties. Liabilities also increased, predominantly due to an £83.1M growth in trade payables but increases in deferred income and advance payments from finance partners also took their toll, somewhat offset by a £7.9M fall in borrowings. The resultant net tangible assets increased by £37M to £121M as the group issued more shares to pay for the acquisitions, although it is worth noting that the group also has £80M of off balance sheet operating leases.

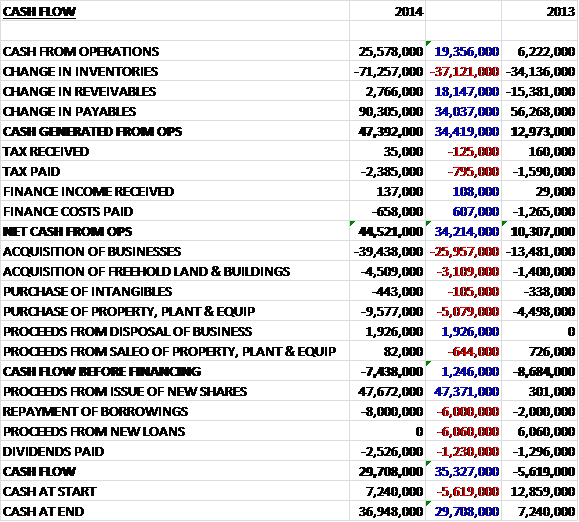

Before movements in working capital, cash profits were an impressive £19.4M higher at £25.6M. A huge increase in payables, partly due to accelerated receipts from manufacturers and consumer finance partners only partially offset by a big increase in inventories meant that after working capital is taken into account, cash generated from operations jumped up to £47.4M. After tax and finance costs, this stood at £44.5M, a jump of £34.2M when compared to last year. The bulk of this cash was spent on the acquisition of new businesses with £39.4M spent on this. Property, plant & equipment accounted for £9.6M as the group opened new outlets and refurbished existing ones and the acquisition of land and buildings cost £4.5M so that the cash flow before financing was an outflow of £7.4M. In order to pay for this, plus £8M worth of loan repayments and £2.5M in dividends the group issued new shares which netted £47.7M to give a positive cash flow of £29.7M and a cash figure of £36.9M at the end of the year. It is worth noting that this level of cash represents the annual reduction in working capital prior to a plate change month (March) and the year-end cash level is about £15M higher than the normalised cash balances throughout the rest of the year. Despite this, though, if it wasn’t for the acquisitions, which admittedly are part of the group’s strategy, there would be a very strong fee cash flow figure here.

The after sales sector makes up by far the most profitable business with margins in 2014 standing at 43%. Next are used cars with margins of 10.8%, then new cars at 7.6% and finally new fleet and commercial with thin margins of just 2.4%. The online space is an increasingly important part of the business and the group operates a number of websites around the Bristol Street brand and have recently invested in them to include enhancements to the online service booking facility and vehicles sold due to leads generated from the websites increased by over 2,000 to 11,410. In addition, Vertu have entered into a partnership with Haymarket Media to jointly operate “What Car Leasing” which allows external franchised dealerships to advertise on the platform for a monthly fee in exchange for sales leads for new cars on personal hire contracts.

During the year, new retail car volumes sold grew by nearly 20% on a like for like basis which was stronger than the 15% achieved by the UK market as a whole. Volumes of sales on the Motability scheme fell by 1% on a like for like basis as other, higher margin, markets were favoured but due to the strength of the market, investment is being made in the sales team. Like for like group sales of new fleet vehicles increased by 9.5% against the UK market of 5.6% and sales of commercial vehicles were up 29.2% against 15.1% and although margins remain slim in these products, a focus on local SME’s is driving it upwards slightly. Group like for like used vehicle sales were up 7.1% and the UK market as a whole remained stable despite some slippage from used car sales into new cars as customers felt more confident about the economic outlook. Further developments to deliver greater sales include a new contact centre to undertake follow up calls to customers who have visited a dealership but did not make a purchase.

Like for like revenues in all aftersales activities increased by 4.3% with service revenues increasing by 6.8% with slowly strengthening margins (an impressive 43.1%). The accident repair sector stabilised during the year after a period of contraction in demand as capacity reduction rebalanced the supply/demand levels. Revenues in Vertu’s accident repair centres grew by 5.6% on a like for like basis and margins improved to a massive 65% in the nine centres the group owns. Further margin improvement is being sought due to better measurement and monitoring of paint usage. The revenue for the supply of parts grew by 3.4% on a like for like basis and parts represent about 27% of total aftersales profitability. The sector benefits from increased volumes at the group’s service and accident repair business and it is also a distributer of parts to other businesses. The group now has over 55,000 customers paying monthly for service and MOTs via their three year plan products and service plans sold on behalf of the manufacturers are helping the Vertu take business from independent suppliers.

In the past the group has been acquiring volume franchised dealerships in order to grow a scaled automotive retail group. This year they have diversified from this strategy with the Jaguar Land Rover acquisition detailed below. They also acquired their first VW dealerships to further diversify their outlets but this represents a broadening of the franchise competition rather than a change of direction. Therefore the basic strategy of the group is to acquire a diverse range of dealerships, absorb them into the group, increasing profitability through synergies and increased customer retention which then leads on to more high margin after sales work. There is apparently a strong pipeline of acquisition opportunities across a number of manufacturers, including the possibility of adding new franchises to the portfolio.

During the year the group made a number of acquisitions, the largest being Albert Farnell which consists of three Land Rover dealerships in Leeds, Bradford and Guiseley and was purchased from Co-Operative Group Motors for a cash consideration of £31.2M and the acquisition included £17.4M of Goodwill. In the eight and a half months since acquisition, it contributed some £3.8M to operating profit. In July the group acquired Boston and Lincoln VW from Lookers Motor Group for a cash consideration of £3M, which included just £270K of goodwill. Another acquisition was Brookside, representing three VW dealerships in Nottingham and Mansfield, for a cash consideration of £1.7M. This acquisition comes with a neutral net asset base so pretty much that whole consideration is for goodwill. In the three months after acquisition, Brookside made an operating loss of £462K. There were a few other, smaller, acquisitions which included a Hyundai dealership in Edinburgh acquired from the Phoenix Car Company and another from Archers of Edinburgh. In January 2014 the group acquired Sheffield Nissan and Volvo from Harratts of Wakefield. The total consideration for these smaller acquisitions was £2.9M which included £300K of goodwill.

During the year the group also made a disposal, selling its three loss making heavy truck operations, the Iveco and aftersales outlets in Bristol, Swindon and Gloucester, to Aquila Truck Centres Italia for a cash consideration of just under £2M and 192K of preference shares in Aquila. The group lost £2.3M in net assets, mostly relating to inventories, in the disposal so there was no profit made here. As well as the acquisitions there were also new openings with a new SEAT dealership, one new Volvo dealership, which is a new brand for the group and a new Nissan outlet, which makes Vertu one of the largest Nissan dealerships in the country with ten outlets.

March is the most significant month for UK automotive retail due to the plate change and its impact on new car demand and the seasonality of servicing. This March, just after the year end, UK new car registrations to the retail market grew by nearly 21% with the group’s like for like sales volumes growing at a similar rate. New vehicle margins were slightly lower than last year due to increased discounting but the increased volume more than made up for the margin shortfall. In addition to this, profitability at the acquired groups improved. In March and April the group’s like for like used retail volumes were up 14.5% and margin was maintained which meant a decent profit uptick overall. Service probability since the year end has run ahead of last year and continues to benefit from the customer retention initiatives. The outlook for the new car market in the UK is favourable but growth in the private market us expected to be at lower levels than this year. Continental demand remains weak, despite some Western European markets showing signs of improvement, which means European manufacturers are likely to continue targeting the UK in order to manage European over capacity, particularly as a strong Sterling gives them an even better margin.

There are a number of risks that could potentially affect the business. Profitability is influenced by the economic conditions in the UK such as unemployment and consumer confidence along with fuel prices and tax levels. As most outlets rely on just one or two manufacturers, they are susceptible to any problems with these suppliers and the group seems to be making moves to mitigate this risk by acquiring dealers who specialise in different car marques. Another risk is the value of used cars, which can fluctuate depending on supply and demand and any reduction would lead to write-downs against the value of the group’s used car inventory. Regulations have been relaxed regarding restrictions on the number of dealers operating within a territory which could add competition to the franchised dealer network. Finally, the group is susceptible to exchange rate changes as manufacturers could adjust prices depending on Sterling against Euro and Yen fluctuations in particular.

After the end of the balance sheet date the group disposed of a disused property at Haydn Road, Nottingham for cash proceeds of £600K and with a net book value of £600K, no profit was earned on the disposal. In May the group acquired Hillendale Group which operates a Land Rover dealership in Burnley and a Jaguar dealership in Bolton for £8.2M (£6.2M in cash and £2M in shares).

At the current share price the P/E ratio is 14 which is similar to that of last year. On next year’s forecast, the ratio falls to 11.6 which is historically low for this company, suggesting some upward potential in the share price. There is a modest dividend on offer here with the shares yielding 1.4% at the current price after the pay-out increased by 14% this year, it increases to 1.6% next year. At the end of the year net cash stood at £31.4M, an increase from the net debt of £6.2M recorded last year, although this is of course due to the issuance of new shares for cash. Nevertheless, the balance sheet is very strong.

This has been a good year for Vertu, profits are up, as are net assets, although this is due to the issue of new shares that increased cash available for purchases. Operational cash generation was very strong and although the dividend yield is modest, further improvements to cash income could give room for increased pay outs. The strategy of acquisitions is likely to continue and there is likely to be further diversification into other franchises. The fortunes of the group clearly depend to some extent on external forces but with a strong UK outlook and weak demand in the rest of the EU, the current trend is likely to continue for the time being, albeit with growth likely at a slightly slower rate.