Victoria Oil and Gas has now release its interim results for the year ending 2015.

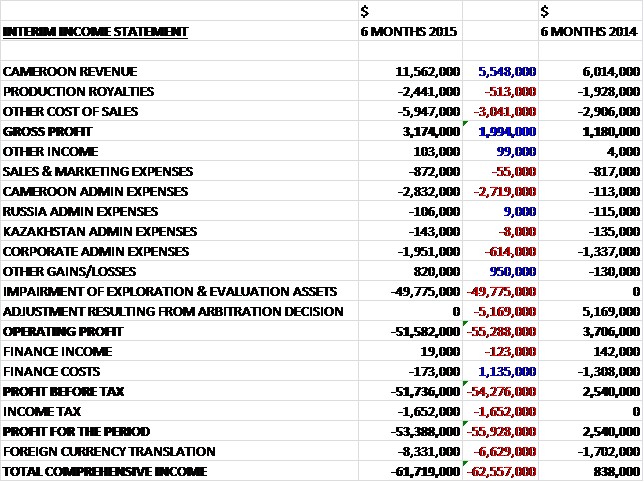

Revenues at the Cameroon assets increased by $5.5M when compared to the first half of last year but cost of sales also increased to give a gross profit nearly $2M higher than last time at $3.2M. Admin expenses then increased which were partially offset by a an $820K “other gain” to give an underlying operating profit about $344K more than last time before the big one-off factors came into play with the lack of the $5.2M arbitration decision adjustment and the $50M impairment of the Russian exploration and evaluation assets which meant that the operating loss was $51.6M during the period. A fall in finance costs was more than offset by an increase in tax to give a loss for the year of $53.4M, a $55.9M reversal on the first six months of 2014.

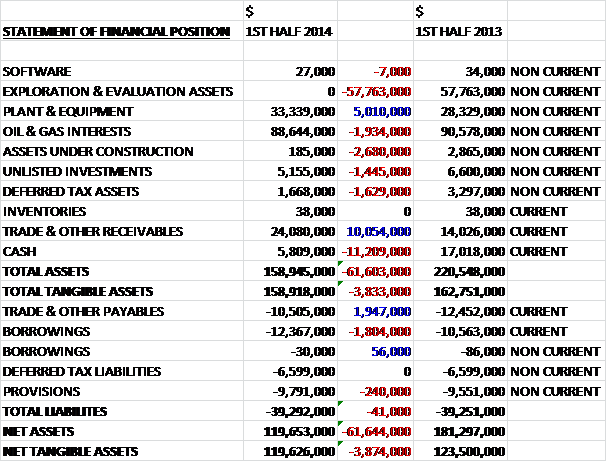

When compared to the end point of last year, total assets at the half year point were some $61.6M lower, driven predominantly by the full $57.8M impairment of the exploration and evaluation assets. We also saw an $11.2M decline in cash levels, a $2.7M fall in assets under construction as they were transferred to plant &equipment, a $1.9M decline in oil and gas interests, a $1.6M fall in deferred tax assets and a $1.4M decrease in the value of the unlisted investment. These falls were somewhat counteracted by a $10.1M increase in trade & other receivables which included $18.2M due from RSM, $17M of which was received after the period end, and a $5M growth in plant and equipment. Liabilities remained broadly flat as a $1.7M increase in borrowings was offset by a $1.9M fall in trade and other payables to give a net tangible asset level some $3.9M lower than last year at $119.6M.

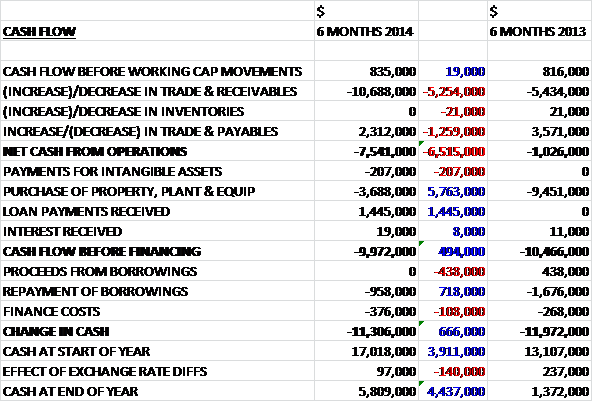

Before movements in working capital, cash profits were broadly flat at $835K. A huge increase in receivables, relating to the RSM situation as they did not pay any of their part of expenses pending the findings from Deloitte, meant that the net cash outflow from operations increased by $6.5M to $7.5M. The group then spent $3.7M on property, plant and equipment, relating mainly to the pipeline network in Cameroon, somewhat offset by a $1.4M receipt of loan payments received from the group’s unlisted investments. The group also paid back nearly one million dollars in borrowings and after finance costs of $376K there was an $11.3M outflow of cash for the six month period to leave the cash position at the half year point of $5.8M. Following the post balance sheet date receipt of receivables from RSM, however, this should now be a bit healthier.

The profit before tax of the Cameroon operation was just $169K, a big decline from the $4.7M enjoyed last year. During the year the group signed a legally binding term sheet with ENEO, Cameroon’s integrated utility company, to supply gas to two power stations, Logbaba and Bassa, located in Douala. The power stations will generate up to 50MW from Gensets supplied by Altaaqa. The agreement includes “take or pay” consumption rates at a price of $9/mmbtu and the power stations will consume about 9mmscf per day in the dry season and 3mmscf per day in the wet season. The contract is for two years and extendable by mutual agreement and it has the potential to treble the group’s current gas production with the 2015 production likely to amount to 10.4mmscf per day. So far this year, the group has been achieving a production rate of between 3.9 and 4.4mmscf per day, an increase from the 3.9mmscf per day reached at the end point of last year.

The group has already built and tested gas pipelines to both of the power stations with a completion certificate being issued for the Bassa station and the work at the Logbaba station should be complete in a couple of weeks. The project is scheduled to be online sometime during Q1 2015 which is a pretty quick turnaround really. There were a couple of issues during the period as the group managed to secure the release of some Gensets from local customs and the Wouri river crossing was delayed but the group does now have access to a wide base of thermal gas customers on the other side of the river. The company is also in the process of making the final connections to the Dangote cement plant, a major new thermal supply customer on this side of the river.

Post period end, the group conducted a workover of well La-106 where they performed cement remediation work. Initial flow tests of the well were 5 to 6mmscf per day and this well can provide back up to the La-105 well. Later on the specialist equipment and personnel used on the workover was utilised to add perforations to well La-105. The sands above the Upper Logbaba D Sand were perforated and in total 57 metres of additional perforations were shot. After shooting the perforations, a production log was run in the well to determine the contributions of the new zones to flow and as a baseline for future logs. The newly perforated zones are performing well and will significantly contribute to production in the future as the lower sands deplete. The company is also making plans for the drilling of future wells at Logbaba that are aimed at increasing reserves and production to meet the growing gas demand in Cameroon.

In all, the total gas sold during the period was 716mmscf with 13,221 bbls of condensate produced. Due to the fixed price contracts, the gas prices have remained unchanged during the period but the global downturn in oil prices has negatively impacted to condensate sales prices as it is linked directly to the price of Brent Crude. The loss before tax at the Russian project was $49.9M as the asset was completely impaired, this compares to a $129K loss in the first half of last year. The profit before tax in Kazakhstan was $113K, an improvement from the $430K loss incurred last time but I still have no idea what is going on in the country as the reports never make reference to it!

As has been seen, although the group continues to seek avenues for deriving value from the Siberian asset through a farm out, joint venture or sale it is considered that given the political issues in Russia and the weakness of the world price of oil it will be significantly more difficult to realise its carrying value. As a result of this, the directors have taken the decision to completely write down the asset. There may be an adjustment in future periods depending on the current efforts to derive value from the asset.

After the end of the balance sheet date, the group appointed John Bryant as an independent non-executive director. He has commercial and financial experience in developing and managing new businesses with over 40 years’ experience in the oil, gas and energy services sectors. Also in December, Deloitte released its final report regarding the RSM issue. It was decided that RSM was due to pay $10.1M for their share of cost and RSM have now transferred $10.6M to the group as of February. To date there is now just $1.2M of receivables still to be paid to the group which is real progress and it seems this may finally be resolved shortly with the Chairman stating that both companies are now working together to unlock the full potential of the Logbaba field.

Overall then, this was an OK update. The impairment of the Russian asset is clearly disappointing and leaves the group with all their eggs in one basket, being Cameroon. The cash performance was rather disappointing but after the period end, the agreement made with RSM will reverse those increasing receivables and really help cash flow in the near term. When RSM has paid off all of its expenses, however, they will revert back to being entitled to a percentage of revenues from the Cameroon field which may affect profits somewhat. The deal signed with ENEOS seems to be a really good one, and potentially transformational, increasing gas sales by as much as three-fold. In conclusion, I must say I am a but torn here, the new gas deals are exciting but there is still considerable risk tied into just one asset in Africa, albeit a relatively stable African company.

After the share consolidation at the end of last year, the shares have been trading sideways for some time – there is no rush for me to buy in here yet.

On the 9th March the group announced that it has issued completion certificates to ENEO for all pipeline construction work and pressure reduction and metering stations at both the Lopgbaba and Bassa power stations. The work was completed ahead of schedule and the group is ready to connect to the Gensets that being installed by Altaaqa. About 1.4km of pipeline was connected to the Magzi-Bassa valve station. The pipeline is now gassed up and ready for the delivery of gas and this means that the group has completed all of its contractual responsibilities under the agreement. A total of 22 Gensets have arrived and been cleared through customers, 16 of which are now onsite at the Bassa station with the other 6 at the Logbaba powerstation. The remaining 17 Gensets are scheduled to arrive in Douala on March 15th and will be installed at the Logbaba station. The target completion date remains the end of March so hopefully those extra Gensets will be cleared through customs at the same pace as the last lot. This is all good news, there were numerous opportunities for over-runs here on this very important project.

On the 23rd March it was announced that the group is now supplying about 4.5 mmscf per day of gas to the Altaaqa Gensets installed at Bassa power station. following the pipeline connection to the site and the successful installation of the Gensets, 20MW of power generated is now being fed into the grid. Total gas production for the group has risen from 4.5mmsc/d to about 8.5mmsc/d. With the Bassa power supply online, Altaaqa will now focus on completing the installation of the Gensets at the 30MW Logbaba power station with the original schedule of completion by the end of March now slipping slightly to the end of April due to shipping delays. Despite the delays, things seem to be sliding into place for the company and I have made a small purchase here.

On the 17th April it was announced that gas supply to industrial customers in the Cameroon had risen to 9.4 mmscf/d on a seven day average basis following the increased production to feed the Bassa power station. This marks a more than doubling of the production rate from the beginning of the year. The take or pay obligations have now been satisfied at the Bassa power station following consistent generation of 20MW of power. The completion of the Logbaba power station has now entered its final phase, with all remaining gensets being released from customs and installed by Altaaqa. This installation is expected to be completed soon.

On the 23rd April the group announced that it had commenced supply of gas to the Logbaba power station and 30MW of power is now being generated there. This means that the group’s responsibilities to deliver gas to both stations have now been met that triggers the take or pay conditions in the contract with ENEO. The average gas production since the station went online now stands at 14.5 mmscf/d. This all seems very positive, I wonder what the next target is?

On the 27th May the group announced that it had acquired the Logbaba gas processing plant from Expro Worldwide. The plant currently processes gas extracted from the group’s wells, producing condensate which is sold to a local refinery and clean natural gas which is distributed to customers through the pipeline network in Douala. It has been purchased for $2.578M using cash generated from operations and the board believe that the purchase will deliver significant cost savings. They are now evaluating options for the plant expansion.

On the 9th June the group announced some new customers. They have completed connections and are now supplying natural gas to three new industrial customers from its gas pipeline network including the new Dangote cement clinker plant on the southern shore of the Wouri river; New Foods, a food processing business owned by the Fokou group; and Sic Cacaos, a subsidiary of Barry Callebaut who are a Swiss-owned chocolate group and one of the world’s largest producers of cocoa. The latter two customers have both converted from heavy fuel oil to natural gas and the total estimated additional daily consumption from the three new connections is 0.7mmscf. May figures show a total monthly average of 12.4mmscf per day compared to just 4 in January which reflects some seasonal variations in demand from thermal customers and a steady build-up of gas consumption by ENEO. Likewise condensate production has increased from 1,812 bbls in January to 5,366 bbls in May.

The gas supply to the Bassa and Logbaba power stations is steady and the group are now focussing on additional customers in the Bonaberi industrial area across the Wouri River. They are expecting to exceed their 10.5mmscf per day target for 2015. All of this sounds rather promising, although a lack of any financial numbers is probably keeping a lid on progress in the share price.

On the 23rd July the group released a Q2 operations update. During the quarter the average gas consumption grew from 4.5mmscf per day in Q1 to 12.6mmscf per day with total gas sold romping ahead to 1,120mmscf from 405mmscf and condensate increasing from 6,345bbls to 13,455bbls. Against the same quarter of last year, the comparison was even better. This significant expansion follows the first grid power connections coming on line under the deal with ENEO and new thermal customers being connected. Group cash was $14.2M at the end of the quarter, down from $15.6M at the end of the last quarter with a capital spend of $2.6M on the gas plant acquisition from Expro so underlying cash generation looks to be about $1.2M in the quarter, although it should be pointed out that it is the dry season that generates the most sales. The cash received from gas and condensate sales was $9.8M compared to $5.1M in Q1 and operations remain in line with expectations for the next quarter.

At the beginning of the period, gas supply to both the Bassa and Logbaba power stations commenced and the successful running of maximum supply to both power plants met the requirements set by ENEO to trigger the minimum take or pay condition. This agreement requires the supply of 10.1mmscf per day of gas to generate 50MW of power with ENEO consequently agreeing to take or pay 90% of total usage during the dry season and 30% in the wet season. The Dangote cement plant was the largest of a number of new gas supply connections completed during the period.

As hinted at above, the Lopgbaba gas production plant was purchased from Expro using internal cash generated and the group is evaluating proposals for a long-term contract for the operation and maintenance of the plant with specialist service companies., including Expro itself. The group is also studying options for the expansion of the gas production plant from its existing 20mmscf per day level up to 40mmscf per day.

Initial planning, well design and engineering for drilling the next two wells (LA107 and LA108) has been accelerated due to the demand for gas in Douala and the current schedule estimates spudding of the wells in H2 2016 and completion later in the year. The company is also analysing techniques for conducting 2D and 3D seismic programmes in urban environments and for re-processing and extrapolating key historic seismic data to assist in sub-surface interpretations. The Chairman has stated that they plan to fund this development programme from existing and future cash flows along with local lines of credit.

In addition, the group is in discussion with several groups for the provision of CNG solution whereby a technical partner will undertake all gas compression capital expenditure and logistical operations and it is expected that a preferred partner will be selected in the coming months.

Overall this seems like a decent update. The group is certainly coming along nicely operationally but until we see some actual accounts it is difficult to put a value on the company. It seems as though underlying operations are cash flow positive now the new supply has started and the fact that there is no planned placing to drill the next two wells is welcome news.

Despite the initial positive share price reaction to the update it would seem foolhardy to bet against this chart at the moment so I remain an observer for the time being.