Victoria Oil and Gas is a hydrocarbon developer with flagship assets in Cameroon. From gas production wells in the city of Douala, the group supplies energy products to major industries in the region through a pipeline network built by Victoria. They also produce thermal gas, condensate and gas for electricity generation. The company also holds 100% of the West Medvezhye oil and gas project near Nadym in Russia. They have now released their final results for the year ending 2014.

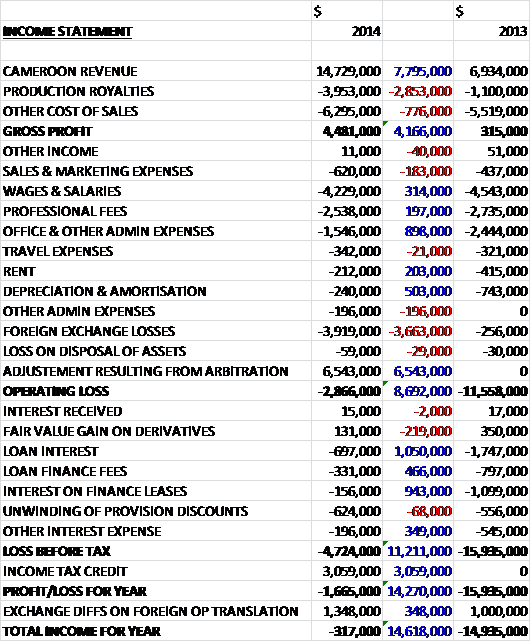

The only assets that produce any revenue are those in the Cameroon and sales there were some $7.8M higher than last year. Production royalties increased by $2.9M and other cost of sales grew by $776K due to increased depreciation charges, to give a gross profit $4.2M higher than in 2013. An increase in sales and marketing expenses were more than offset by a decline in admin costs as RSM regained their participating interest and became liable for 40% of the costs incurred on the Cameroon project, but a £3.7M adverse movement in foreign exchange took its toll, offset by the adjustment from the arbitration ruling so that the group recorded an operating loss of $2.9M, some $8.7M better than last time. As far as finance costs are concerned, loan interest decreased by more than a million dollars to $697K and there were also large falls in finance lease interest and loan finance fees. The group managed to get a $3.1M tax credit which meant that the loss for the year was just $1.7M, a massive $14.3M improvement on last year but a loss nonetheless.

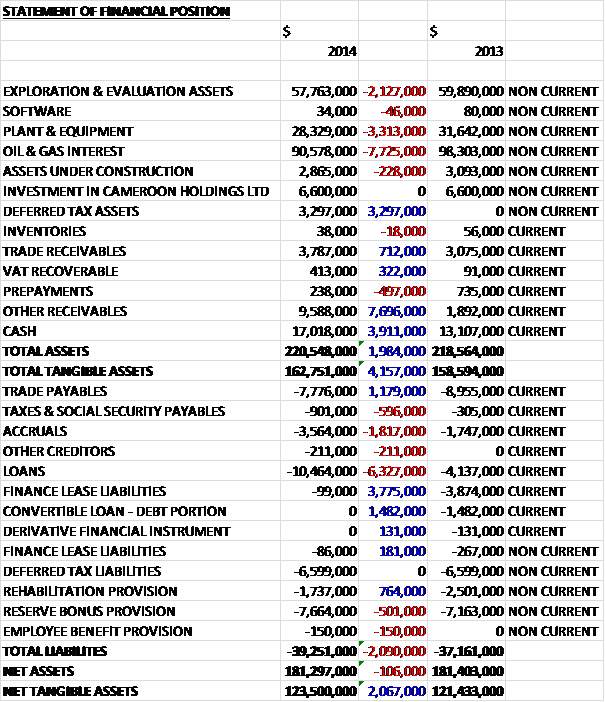

When compared to last year, total assets increased by nearly $2M driven by a $7.7M increase in other receivables, relating to money owed by RSM, a $3.9M growth in cash levels and a $3.3M hike in deferred tax assets as previous tax losses can be offset against future profits as it seems the venture is becoming profitable, partially offset by $7.7M decline in oil and gas interests due to the adjustment following the arbitration decision along with higher depreciation, a $3.3M fall in property, plant & equipment, due to the arbitration decision, and a $2.1M decline in exploration and evaluation assets, all of which relate to the West Medvezhye project in Siberia. Liabilities also increased due to a $6.2M increase in loans and a $1.8M growth in accruals, partially offset by a $3.8M decline in finance lease liabilities and the eradication of a $1.5M debt portion of a convertible loan. The end result is a $2.1M increase in net tangible assets to $123.5M which seems like a pretty strong balance sheet to me.

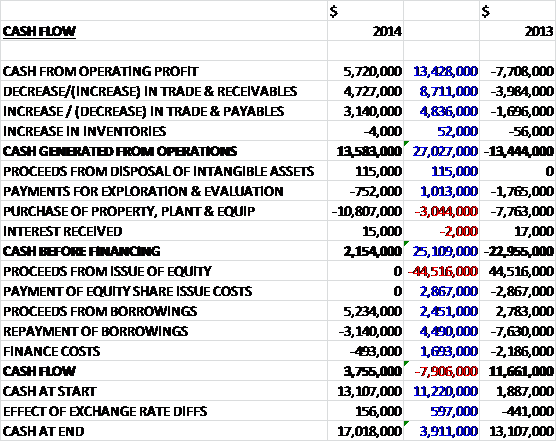

Before movements in working capital, there was a $13.4M positive swing in cash profits to $5.7M. Favourable movements in both receivables and payables meant that cash generated from operations was $13.6M, a $27M improvement. The vast bulk of this cash was spent on property, plant and equipment relating to the expansion of the pipeline network in Cameroon, with a further $752K going on evaluation and exploration which gave a cash flow before financing of $2.2M. There were $493K worth of finance costs and about $2.1M worth of new loans to give a cash flow of $3.8M for the year and a cash total of $17M at the end of the period which actually seems like a pretty good performance to me, although it seems a lot of the good performance is due to the receivables obtained from RSM. As of mid-October the cash levels stood at just $8.5M.

The group supplies customers gas for thermal use such as in boilers, process plants and furnaces. There are currently 18 customers in the medium to heavy industry category consuming the gas. Gas condensate is used as a cleaner and solvent, lantern and stove fuel and as a dilutent in heavy oil production. It can be taken by road tanker to various other parts of the country and 14,107 bbls were produced during the year. Gas is also supplied to generators for customer’s factories and plants. The first six Gensets were installed during the year at four customer sites, resulting in an immediate increase in gas supply. The group is looking to expand its gas to power business and develop the model as per customer needs. The aim is to also supply gas to Gensets at power stations in Douala which should help with the security of supply in the city and finally the group is evaluating a compressed natural gas project where it is transported by road tanker to customers without the capital intensive requirement of a pipeline. It is believed that this business will be commercially viable within a radius of about 200km of operations. The group has a good first mover advantage but other companies are drilling in the area so there could potentially be some competition in the future.

The Cameroon operations enjoyed a pre-tax profit of $4.6M, a $12M improvement on last year. The Logbaba gas project is 60% owned by the group and 40% by the troublesome RSM. The project achieved operational break even on a cash flow basis in February with an average 3.2 mmscf/d production rate achieved. By early July it had increased to 3.9 mmscf/d and the first Gensets were rolled out to major customers in Douala. It is thought that the group is currently only using about 20% of the capacity of the gas processing plant so sales have plenty of room for expansion. The group is going to undertake additional works on well La-106 in early 2015 to unlock further gas supply from the upper zones of the Logbaba structure.

Having seen the grid power supply issues that affect a lot of their customers, the group has begun the development of a gas to power strategy, hence the Genset scheme. A contract was signed with Energyst International for the operation and maintenance of six caterpillar generation units which have been rented in order to circumnavigate the import duty on shipment into Cameroon. Unfortunately the customs agents disputed this technique and the first Gensets were held at the port of Douala for over six months before being released in early 2014. These initial sets were used to prove the concept of the power generation model and following the success of the trial, the group is looking to source bespoke size Genset for future customers.

During the first part of the year, pipeline expansion was seen as the priority but operational priorities were subsequently reviewed and it was decided that the group should concentrate on near-term customer connections and to utilise the current pipeline infrastructure more economically with new pipework only prioritised if it could rapidly connect customers. In January 2014 the group signed a collaboration agreement with ENEO, the private-public partnership that operates Cameroon’s national electricity work to examine ways of increasing power supply by the use of Logbaba gas. The first project involves working with ENEO and some Genset providers to connect gas to rented Gensets for power generation at two power stations, Bassa and Logbaba in Douala. Currently these stations use Fuel Oil and by installing these units for an initial two year period, it should allow ENEO time to determine longer term solutions. The roll out of power should begin in early 2015.

Gas supply agreements were signed in January with Dangote for the provision of gas to a major cement plant under construction in Douala, and SOCAVER, the bottling plant operated by SABC. Following the period end, all six Genset were installed at customer sites with successful connection to the gas supply and Socapursel, a food manufacturing business, was also connected for thermal gas usage. The pipeline to the Dangote construction site was completed, ready for gas connection that is expected to occur in late 2014. A renegotiated agreement was signed with Energyst covering the supply of future Gensets, giving the group the flexibility for outright purchase or sale and leaseback arrangements to new customers as well as the existing rental model. Work has begun on the delivery of the next phase of Gensets to other thermal supply clients and new customers.

All pipe laying operations have now been outsourced to Britanica with a fixed cost per metre agreement with all work approved by Victoria management. Condensate production increased during the period as higher levels of gas were produced for delivery and 14,107 bbls of condensate was produced to be sold to refinery in Limbe, just north of Douala with the average price achieved during the year $106.14 bbl. The Wouri river crossing, connecting the far shore with the Logbaba pipeline started in July which will extend the reach of the gas supply network to a major new industrial area in the city. About 1.5km of pipeline on the far shore has already been laid so that three customers are ready for connection to the main pipeline when it is completed.

The Russian operation had a pre-tax loss of $336K, a $300K improvement on 2013. The West Medvezhye licence has been on the back burner for a while as the group concentrates on Cameroon but they have completed geochemical, passive seismic surveys and reprocessed seismic data in order to identify the location and size of prospects and to ultimately decide on the next drilling locations. The 100% owned asset has proven and provable reserves of 14.4 mmboe and the best estimate put prospective resources at around 1.4 bboe. Recently, relations between Russia and the West have deteriorated which clearly puts this project under some risk. The Kazakhstan operation suffered a pre-tax loss of $3.3M, a $3M widening when compared to last year. There is no other mention of this concession in report so I have no idea what is going on here.

An issue that has affected the group is that of the arbitration decision involving RSM, the partner on the Logbaba gas and condensate project. Some history to the dispute is that RSM failed to make cash calls as they became due to fund its portion of costs which led the board to believe that RSM had defaulted in meetings its obligations and had forfeited its 40% participating interest in the project which was a view that was challenged by RSM. In December 2013, the ICC found that RSM was in default for its non-payment of the cash calls but ruled that the forfeit of its interest had not been established to the level of certainty required under Texas law. Last year the accounts were prepared in the assumption that RSM had already forfeited its interest, so this has had to be changed for the accounts this year. This has led to a credit of $6.5M relating to RSM’s share of prior period operating expenses and led to a $13.7M negative adjustment to the balance sheet this year.

Following the arbitration decision, RSM has paid $4.1M in settlement of one outstanding cash call but the group has issued further cash calls of $24M relating to incurred expenses since the end of the first arbitration and $2M relating to an advance on RSM’s forecast expenses. Not surprisingly RSM failed to pay these cash calls as they fell due and the group issued notices of default for the overdue calls which led to further arbitration proceedings in January 2014. A settlement was reached whereby RSM will pay $16.3M towards the cash calls with an agreement for an audit to determine the final balance payable which meant that the group withdrew its notices of default against RSM. To date, RSM has paid the group a total of $20.8M towards its share of costs at the concession. The main financial effects to Victoria of RSM resuming its 40% participating interest is that the group is entitled to 100% of revenues from sales of hydrocarbons until its initial work commitment costs are recovered, after which RSM will become entitled to its share of revenues; the group’s responsibility for certain post-exploration costs is reduced to 60%; and the group is required to pay a royalty of 0.8% to RSM until they become entitled to their participating share of revenue.

One risk that the group faces is the political and regulatory risk of the territories in which it operates. Africa and Russia both present their fair share of these risks. There does seem to be a bit of customer risk with five clients contributing to 10% or more of the group’s revenue this year including the most important at 24%, which does actually spread the risk somewhat since the largest customer in 2013 made up 29% of total sales. The group seems to be having an increasing problem with late receivables. This year, average trade receivable days increased from 62 in 2013 to 115 with some $381K not impaired but overdue by more than 120 days. Likewise, there were $234K of other receivables older than 120 days compared to none last year and $866K is considered uncollectable and part of the cost pipeline. About 78% of trade receivables are owed by companies considered low risk buy the remaining 22% are made up of local Cameroonian companies that do not have state participation and are considered higher risk. Apparently if the funds owed are not forthcoming from RSM the company may have to look for further funding. Finally, another risk is clearly the fact that the group relies on just two wells in one producing region for all of its revenues. If something were to happen to the Cameroon wells, the consequences could be very serious for Victoria.

The borrowing structure seems to be rather complex. In January 2014 the group signed a loan agreement with BGFI of Cameroon worth $8.3M to fund pipeline extensions, customer connection work and installation of Gensets at customer premises. The facility is for a 6 month term, renewable for a further six months with interest payable at 7.25% per annum. A year after it was taken out, if the loan remains unpaid it converts to a three year term loan at the same interest rate repayable in monthly instalments. There is $5M outstanding on the loan currently and the intention is to let it run over into the three year loan. In 2007 the group created a $10M convertible loan note facility with UAE based Noor Petroleum, where a former company director was on the board. A total of $3M was drawn down against the loan in by the start of 2009. Under the terms of the agreement, the notes were due for repayment at the end of 2012 and bore interest at 2.5% per annum, payable biannually and convertible into shares of the company at a price of 16.5p. The loans remain outstanding but are no longer convertible into shares as the 2012 deadline passed. They are payable on demand and now accrue interest at 6.5% per annum with the balance outstanding now being $4.4M.

The group has a number of royalty obligations in place regarding the Logbaba projects. They are 8% to the state of Cameroon, 0.8% to RSM until they become entitled to their participating share of the interest (see above) and 8.3% which were assumed on acquisition of Bramlin or arose under commercial contracts for the provision of drilling and other services.

The group are making an effort to change the way that the company is perceived by trying to move it away from being an exploration and production company towards being an Energy Utility. I remain unconvinced about this but they have strengthened the board with the hiring of James McBurney as an independent non-executive director. Previously James headed up the European Natural Resources investment banking group at Bank of America and the board are looking to make additional appointments in the near future. The group are also planning to consolidate their shares to significantly reduce the number of shares in issue and have appointed a new broker and financial advisor. John Scott resigned as CEO during the year and the chairman, Kevin Foo took over as interim CEO as well as his current duties. I would suggest that the appointment of a full time CEO would enhance the group’s credentials.

As has been seen, now that the Cameroon operation is generating revenue, the board have recognised some tax losses against future profits with a $3.3M asset being recognised. The group does still have $8.5M of unused tax losses associated with this project though.

Overall then, this is an interesting company. The growth in supply of gas to customers in Cameroon seems to be a good approach and gives them a bit more to their earnings than just and exploration company. The reliance on the one assets, though, is a bit of a concern and the political problems in Russia are likely to make development of the second asset rather difficult. The ongoing issues with their partner on the Cameroon asset is a concern too. I suspect they will eventually scrape together the cash to pay for their part of the costs but in that eventuality, Victoria will lose a proportion of the earnings. Conversely if RSM do default then the group are likely to have to tap up shareholders for further cash to fund development. At this point there just seem to be a bit too many risks for me to jump in just yet but this has been added to my list.