St. Ives has now released its interim results for the year ending 2015.

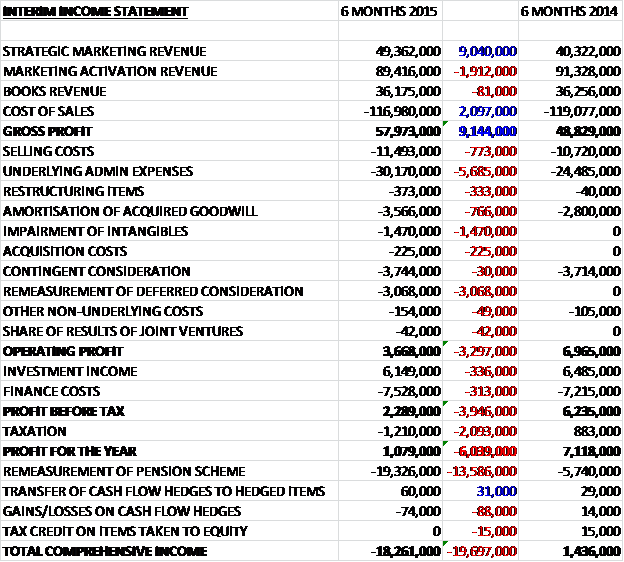

When compared to the first six months of last year, revenues increased as a £9M growth in strategic marketing sales was partially offset by a £1.9M decline in marketing activation revenue and flat books sales. Cost of sales actually fell during the period so that gross profit was some £9.1M higher at £58M. Selling costs increased by £773K and underlying admin expenses were up £5.7M but it is difficult to analyse this company due to the huge number of “one-off” costs that are incurred with various impairments, re-measurements and amortisation. During the period there was a £3.1M remeasurement of contingent consideration, and a £1.5M impairment of intangibles, along with a £766K increase in the amortisation of acquired goodwill to give an operating profit almost half that of the same period last year at £3.7M. Things got worse with a decline in investment income, an increase in finance costs and a tax charge which pretty much halved pre-tax profit so that profit for the year was some £6M lower at £1.1M. The underlying profit for the period has been calculated at £11.6M though, a £4.5M increase on the same period of last year with the underlying profit margin increasing from 8.3% to 9.3%.

When compared to the end of last year, total assets at the half year point fell by £12.9M driven by a £5.6M decline in property, plant & equipment, a £4.9M fall in intangible assets and a £2.8M reduction in trade & other receivables, partially offset by a £923K increase in goodwill. Liabilities increased during the period as a £23.2M increase in pension obligations and a £1.1M growth in deferred income was partially offset by a £6.6M fall in deferred tax liabilities, a £5.4M decline in trade & other payables and a £2.4M fall in deferred consideration payable. The end result was an £18M decline in net tangible assets to a negative £40.9M. Clearly this looks very disappointing but it can be entirely attributed to the increase in pension obligations.

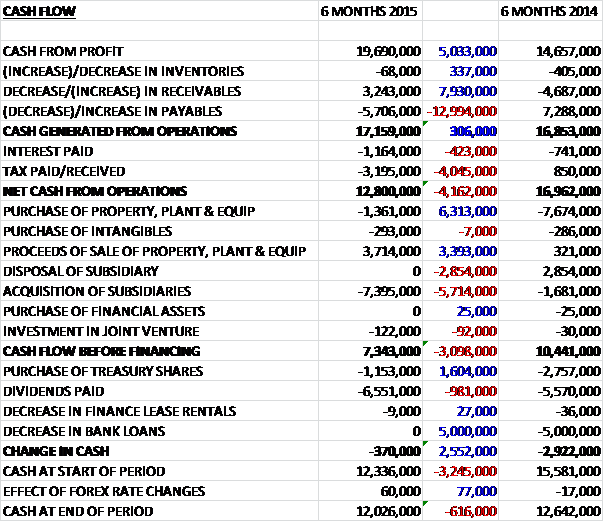

Before movements in working capital, cash profits increased by £5M to £19.7M. This was eroded slightly by a decrease in payables but cash generated from operations was £17.2M before the large increase in tax paid and the £1.2M paid in interest meant that net cash from operations fell by £4.2M to £12.8M. The group actually had a net cash income from its property, plant and equipment transactions so the bulk of the cash was used to purchase a subsidiary, presumably relating to deferred consideration (£7.4M) to give a free cash flow of £7.3M. The rest of this cash was used on dividends and the purchase of treasury shares to give just a £370K cash outflow to give a decent cash pile of £12M. So, not much has been spent on capital expenditure but this cash performance was quite healthy.

During the year, the group has revised its corporate structure with three segments including: Strategic Marketing, focusing on high growth marketing segments of data, digital and consulting; marketing activation, delivering communications through print and in store marketing services; and books, representing the book printing business, Clays. These segments replace the two last year consisting of just marketing and print so should offer some more clarity on the performance of the business, although I am not sure I like the names given to the segments!

Underlying profits at the Strategic Marketing business were £7.1M, a growth of £2.4M when compared to the first half of last year. The data business saw sales fall by £3.2M to £16.7M as a significant one-off software sale in the previous half year was not repeated and the work mix in Response One changed. Although these factors affected revenues, their loss did mean that margins improved in the division. The Occam business recently launched a cloud based data management product which has already attracted clients such as Mitsubishi Motors and Northern Rail with product led solutions being seen as a growth area for the business. Response One developed its service offering to provide end to end communications strategy and planning and has also launched an entry level version of Reciprocate, the UK’s largest donor data pool to further strengthen their work in the Charity sector.

The digital business performed well, increasing sales by £6.7M to £17.9M. Amaze continued to grow its e-commerce capabilities with a number of new business wins and the group is investing in this business to grow and develop a dedicated e-commerce practice. In addition they have launched a digitally led CRM practice, AmazeOne. Branded3 performed well and had a number of significant business wins including growing the online presence of Travelex and driving customer engagement for a number of Bauer Media brands. Realise, which was acquired last year, has integrated well into the group and delivered a strong performance since acquisition, including wins for the World Tourism and Travel Council, the design and build of a number of websites for Rothschild and transforming the online and offline experience for Greyhound in the US.

The Consulting business saw sales increase by £6.9M to £16.1M with Incite, the customer research consultancy, delivering significant revenue growth due to the continued expansion of the business into overseas markets. In addition, an office was opened in Shanghai during the period that is expected to start trading in the second half of the year. The retail and brand consultancy, Pragma, delivered significant growth for the period driven by its expansion of its airports practice with major projects for clients including Luton Airport in addition to a number of international client engagements including Vivarte, the largest non-food retailer in France. Hive, the newly acquired healthcare consulting business has integrated well into the group and is trading in line with expectations.

Underlying profits at the Marketing Activation business were £5M, a £200K increase when compared to the same period of 2014. The Marketing Print businesses saw revenue in line with the prior half with growth in Service Graphics and SIMS due to new business wins including Pernod Ricard, Johnson & Johnson, Toni & Guy and Metro Bank, more than offsetting a decline at SP caused by the ongoing pressures within the grocery retail sector. The Field Marketing business also continued to face pressure within the grocery retail market. The group did, however, invest in new data and technology capabilities and expects to bring these to market in the second half of the year and by bringing the business into the same management structure and the Marketing Print operations, the aim is to improve the operational effectiveness of the segment.

Underlying profits at the Books business were £4.2M, which was flat year on year. Sentiment in the physical book market as a whole seems to have improved with e-reader penetration appearing to have levelled off within both the UK and the US with physical book volumes stable for the first time in a number of years. During the period the group reached an agreement with Penguin Random House to provide 100% of their monochrome book production under a new multi-year contract which represents a significant market share gain for the business and helps to secure about 80% of the segment’s workload for the next three to six year. I am not sure what the margins are like on this project but it does seem like a very good achievement to me.

As usual for St. Ives there were a raft of non-underlying costs recorded. Restructuring items included redundancies of £178K, other restructuring costs of £176K and costs relating to empty properties of £338K, whatever that is. There was a profit on disposal of property, plant and equipment of £49K relating to the sale of a property recorded in the books segment, offset by a £40K loss from the sale of properties in Blackburn, Leeds and Plymouth relating to the Marketing Activation segment. There was a £3.6M charge relating to the amortisation of acquired customer relationships etc in the two marketing businesses which tests the meaning of non-underlying items in my view, but they are non-cash I suppose. There was contingent consideration of £3.7M in respect of acquisitions treated as remuneration and an additional £3.1M change in deferred consideration relating to the Hive acquisition. There was an impairment charge of nearly £300K relating to goodwill and £1.2M relating to customer relationships where there has been a higher level of customer churn in the Field Marketing business than expected. Finally there was £255K of costs associated with acquisitions. I suppose it is good that the group gives such guidance on these costs but there always seem to be so many clouding the real performance achieved.

As touched upon above, following the acquisition of Hive last year there is deferred consideration payable in three tranches based on the EBITDA achieved for 2014, 2015 and 2016. The basis of estimated EBITDA for 2014 was reviewed in the period resulting in an increase in the estimate of deferred consideration payable which has just been added on to Goodwill (as it would have to be) of the acquired company.

Trading in the second half of the year has started well and is in line with expectations. An improving economic climate, allowing clients to increase their marketing spend, makes the board confident of a positive outcome for the full year. The group’s strategy for further growth involves organic growth through collaboration between existing brands, such as the work done for Johnson & Johnson which involved a collaboration between the print management business and the search and digital agency and the work for HSBC who are now a customer of five of the businesses within the group; internationalisation into large and high growth markets such as the new office in Shanghai and further acquisitions which the board are on the look-out for.

With an increase of 5% to the interim dividend, at the current share price the shares yield a decent 4.1% with 4.3% predicted for the full year. At the end of the period, net debt stood at £43M which was relatively unchanged when compared to the position of £42.7M at the end of last year. Overall then, there are some disappointments here. Reported profits collapsed due to those non-underlying costs but underlying profits were up but although that contingent consideration increase in non-underlying it will certainly be paid in cash, either in the second half of the year or in the first half of next year with the current amount of deferred consideration payable within a year being a pretty hefty £10.2M Net assets fell due to the increase in pension obligations but cash flow was not bad, even though dividends were barely covered. The strategic marketing division seems to have done well but I am not sure how much of that increased profit has come from organic growth and the other marketing division has suffered somewhat from the pressures in the grocery market. The books division seems to be doing fairly well though and the shares do yield a decent dividend. On the face of it though, I can see more cash cost pressures in the immediate future despite the long term story looking pretty good.

The chart is quite interesting. The shares had been on a mini-rally since mid January this year but these results have put an end to that. I will wait on the sidelines to see what happens here.

On the 17th March it was announced that the group had acquired Chicago based consultancy Solstice, specialising in mobile first digital product design and engineering services. The acquired group comes with 200 spread across offices in Chicago, New York and Buenos Aires with a client base including Fortune 1000 business, with particular strength in the financial services, manufacturing and distribution sectors. Last year, Solstice generated EBITDA of £2.7M on revenues of £16.5M with gross assets of £5.1M. The group has acquired the business for an initial consideration of £24.7M made up of £20M in cash with the rest in St. Ives shares. Further consideration of up to £25.3M may become payable dependent on profit performance in the years ending 2015, 2016, 2017. The acquisition will be earnings enhancing in the current financial year.

This seems like a decent acquisition but my concern is that St. Ives seems to be stretching itself somewhat with yet another acquisition and my real concern is the build up of deferred consideration. There are no details of how easy it will be for the acquired group to hit those profit targets but £25.3M over three years will be a substantial drag on top of the consideration already on the balance sheet.

On the 11th August the group released a trading update covering the full year. Overall results are expected to be in line with expectations. Trading across the Strategic Marketing segment was positive and significantly ahead of last year. It continues to extend its range of services, primarily through acquisition. The integration of Solstice Consulting is progressing well and the group is investing in additional headcount to support their plans for growth in this segment.

Trading conditions in the Marketing Activation segment have been challenging due to the ongoing pressures within the grocery retail market. As a result, it is expected that revenues will reduce when compared to last year but margin should be maintained as new business wins, cost reductions and efficiency improvements help to mitigate the pressure. Within the books business, there has been an improvement in sentiment within the physical book market with book volumes stable for the first time in years. It is expected that revenue in this sector will be broadly in line with last year and for margin to be maintained.