Omega Diagnostics sells a wide range of specialised products, primarily in the immunoassay, in-vitro diagnostics market with three divisions. The Allergy & Autoimmune division specialises in the research, development, production and marketing of in-vitro allergy and autoimmune tests used by doctors to diagnose patients with allergies and autoimmune diseases. The Food Intolerance division specialises in the research, development and production of kits to aid the detection of immune reactions to food. It also provides clinical analysis to the general public, clinics and health professionals as well as supplying the consumer food defective test. The Infectious disease division specialises in the research, development and production of kits to aid the diagnosis of infectious diseases. The group was founded in 1987 by current CEO Andrew Shepherd and is listed on the AIM exchange. They group has now released its final results for the year ending 2014.

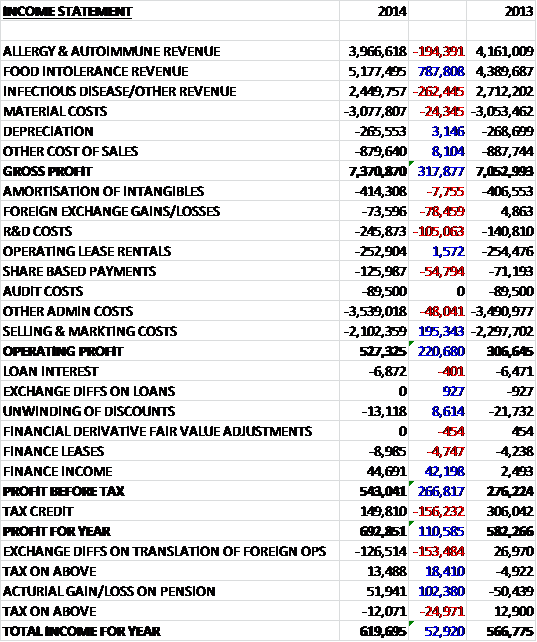

When compared to last year, revenues were up as a £788K increase in food intolerance sales was partially offset by declines in other areas. Cost of sales increased somewhat, so that gross profits were some £318K higher at £7.4M. There was then a small negative shift in foreign exchange and a £105K increase in R&D costs, plus a £55K increase in share based payments that were counteracted by a £195K decline in selling and marketing costs so that operating profit increased by £221K to £527K. A decent increase in finance income was offset by a £156K fall in tax credits to give a profit for the year of £293K, a £111K increase when compared to 2013.

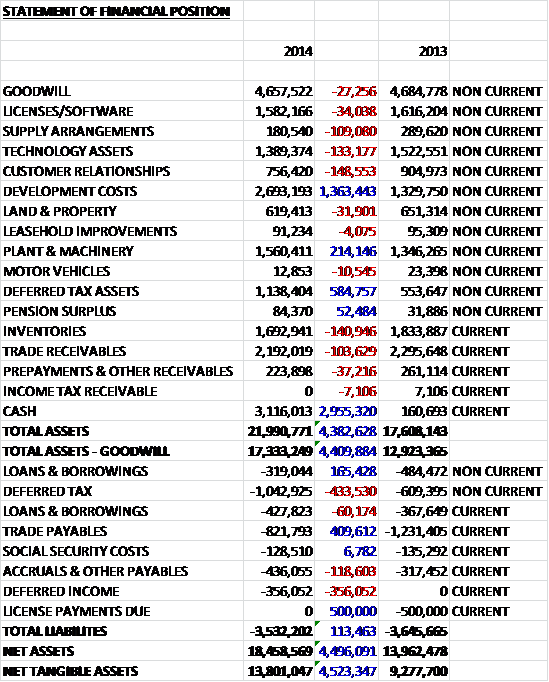

When compared to the end point of last year, total assets increased by £4.4M driven by a £3M increase in cash levels, a £1.4M growth in development costs relating to the Visitect CD4 project and the Allergy iSYS project, and a £585K increase in deferred tax assets, partially offset by modest falls in most of the other asset types. Liabilities fell slightly year on year with the elimination of the £500K of license payments, a £410K fall in trade payables and a £10K decline in borrowings, offset by a £434K increase in deferred tax liabilities, a £356K growth of deferred income, relating to the UNITAID and Scottish Enterprise grant funding, and a £119K increase in accruals and other payables to give a net tangible asset increase of £4.5M, although it is worth noting that there was a £4M placing of shares during the year but this is a strong looking balance sheet nonetheless. There was £1.3M of operating lease commitments not on the balance sheet, which isn’t particularly relevant given the asset levels.

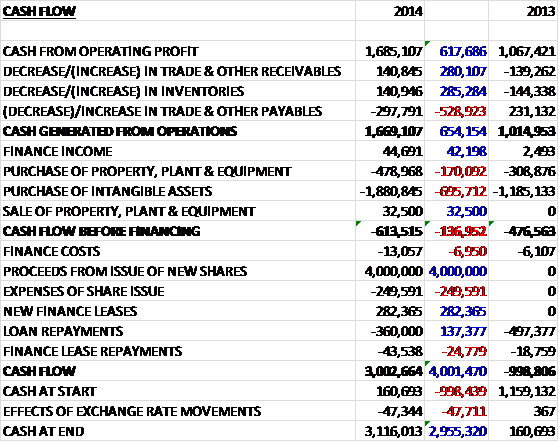

Before movements in working capital, cash profits increased by £618K to £1.7M before working capital movements broadly cancelled each other out to give an operational cash flow of £1.7M, an increase of £654K. All of this cash was used to acquire intangible assets so the purchase of property, plant and equipment relating to the CD4 manufacturing assembly unit and equipment to fill bottles with individual allergy reagents for the iSYS system, sent free cash outflow to £614K. Cash reserves were looking very precarious at the end of last year so the group needed to raise £4M from the issue of new shares before a net increase in finance leases was more than offset by some loan repayments to give a cash flow for the year of some £3M to give a cash pile of £3.1M at the period end. This is an improving performance and the group is not far off from being able to fund itself through its operational cash flows.

The Allergy and Autoimmune business produced an adjusted profit of £152K, a £173K improvement when compared to the small loss last year. Allergy sales fell by £100K to £3.5M and autoimmune product sales fell by £90K to £450K. The allergy sales were derived almost exclusively from the German business which is operating in an environment of reimbursement restrictions. The strategy has been to reinforce customer relationships through training, service and account management to secure the business and to prioritise allergy testing over other testing in a market that has declined by 5% over the past two years. The group continues to sell autoimmune products into markets where automation is ever increasing but despite these headwinds, most of the country markets have maintained their position and the performance drop-off is attributable to a reduction in Iran where reimbursement restrictions have occurred due to the devaluation of the currency.

The Food Intolerance business produced an adjusted profit of £1.7M which was an increase of £500K when compared to 2013. Sales of Food Detective grew by 35% to £1.7M and there was a particularly strong sales performance in Poland and Brazil. Total volumes of the tests were at a record level of 106,312 per annum and excluding component sales to China, the average selling price per kit increased from £22.01 last year to £22.55 this year. Sales of Genarrayt reagents grew by 15% to £2.1M with strong performances in both the Spanish and French markets but there has been a broadening base of other markets with the top five markets now accounting for 63% of sales compared to 70% last year. The group sold a further 13 instruments during the year, taking the cumulative number of installations to 132 instruments and revenue per instrument (for some reason excluding Spain) increased by 7% to £13,746 so I assume if we include Spain, one of the largest markets, revenue per instrument probably fell. The Foodprint lab service achieved sales of £640K compared to £610K last year and the group produced nearly 8,000 patient reports at an average price of £79.55 per report (a small decline from the £80.65 per report in 2013). There are plans to further grow revenues with the introduction of a new dried blood spot test and the broadening of the portfolio in nutritional assessment.

The Infectious Disease business produced an adjusted loss of £95K which was a deterioration of £268K when compared to last year. The decline was due to the loss of business from a UK customer who experienced financial difficulties and the devaluation of the Iranian currency reducing sales through the distributor there. After the period end, the UK customer in difficulties has started to make small orders again as its situation improves. Mitigating these headwinds is good growth in India and Brazil.

The group really seems to be focusing on infectious disease diagnostics as a strategy, particularly in parts of the world where resources remain constrained and there is a substantial unmet need. The main focus at the moment is HIV and the group has developed the Visitect CD4 device which requires no power or refrigeration facilities and can provide a result in 40 minutes. Beta studies in Kenya and India have provided patient data to determine what, if any, aspects of the test requires further optimisation. As the test nears commercialisation, the group will continue to partner with major NGOs and global health organisation. The group also have access to a POC test for Syphilis which can differentiate between active infections and past infections – something that previous tests have struggled with. They have recently increased in house resources and capability to move this project forward.

Through a partnership with Australia’s Burnet institute the group have secured an exclusive global license to the simple, lateral flow POC device that confirms whether a patient’s CD4 count is above or below 350 cells which has the opportunity to significantly reduce the number of patients lost to care as a result of the length of time between testing and receiving HIV treatment. The group has established a UK manufacturing facility for the product which has been fully validated under ISO approved procedures. Also, they have leased a facility in Pune, India where the interior build of a manufacturing base is under construction which has been part funded by a £400K grant from the Burnet Institute. This Indian facility will enable the group to produce and test locally, avoiding an import duty that applies to for Rapid Test imports into the country. In addition, going forward, this manufacturing base is expected to be used to make other rapid tests for the local market where cost per test is a major barrier to market entry.

In India, 140 patient samples have been tested to date and based on an interim analysis of the data the test has produced results on venous blood samples which match the company’s performance design parameters. Results to date on finger stick blood show a similar overall diagnostic performance but with slightly lower levels of sensitivity which is being investigated as the trial proceeds. The trial in Kenya has been extended beyond the initial 200 patients because test performance was just below optimal performance on both venous and finger stick blood so additional devices have been sent to Kenya for further evaluation. The Kenyan site has also received further training from Omega staff and the board expect that these additional tests will allow them to determine and correct the root cause of the difference.

In addition to the test itself, the development of an Android smartphone app to record and transmit the test results has been completed and is undergoing field trials. It is expected that this app will be available in the new financial year which will offer integration into cloud host databases. This mHealth solution has apparently been met with great enthusiasm by NGOs and global health organisations as the test/app combination offers a complete solution from test site to management HQ. There seem to be numerous potential applications for the CD4 device and as well as HIV and syphilis, the group is also looking at Schistosomiasis which is caused by a worm present in many tropical countries affecting about 200M people. The group is working with an expert in this disease area and good early progress is being made in the development of a new lateral flow test. It is anticipated that field trials could commence in the second half of the year.

The plan for the allergy business is to become a leading provider of allergy tests into clinical labs in a global market estimated to be worth over $500M per annum, dominated by one company. The group have exclusively licensed the use of IDS’ automated iSYS instrument for allergy testing and have invested in a long development programme covering initial feasibility, lock down of assay protocol, optimisation and claim support work. They have also set up an in-house manufacturing facility for reagent filling. During the second half of the year, the first allergens finally emerged from the programme following a successful claim support phase. There are now eight allergens that can be run on the iSYS instrument that show comparable results to the market leading competitor and a further 16 which have now completed optimisation. The strategic aim is to launch with a panel of 40 allergens followed by a programme of menu extensions to achieve a number two market position. The initial commercialisation plans involve working with IDS in markets where it has a direct presence, followed by expansion into other territories through third party distributors. The progress on the iSYS instrument has been slow going and the CEO’s frustration is notable.

No customer accounted for 10% or more of group revenues. A lot of the group’s sales are made in Europe, particularly through the German subsidiary, which means they are susceptible to exchange rate differences, however.

During the year the group has appointed Bill Rhodes as a non-executive director. He joins having spent many years at medical technology company Becton Dickinson. The largest shareholder by far is Legal and General, holding about 18% of the group but the directors also have quite a few shares, with two of them holding more than 2% of the company so this looks like a healthy investor base.

Trading in the new financial year to date has been in line with management expectations with a marginal growth in food intolerance testing being offset by the marginal decline in allergy and infectious disease testing. The future landscape is dominated by the Visitect CD4 test and the chairman has stated that they will make significant progress this year in terms of gaining market acceptance for the device but this will depend on the NGO/aid market and individual country approval processes. It is believed that prospects for the group overall are positive.

At the current share price the company trades on a P/E ratio of 22.2, reducing to a decent value 13.3 on next year’s consensus forecast. No dividends have been proposed for this year. Overall then, this is quite a good update. Profits were up slightly, and net assets were up even when we take out the £4M received from the share placing. The operational cash flow improved but the group still does not have any free cash flow and is not yet in a position to fund itself out of operating cash. The Food Intolerance business is the one performing well with decent, improving, profits but the other two sectors continue to struggle due to customer problems, continued German headwinds and Iranian currency issues. The two new products, Visitect CD4 in infectious diseases and iSYS in allergy tests both seem like exciting prospects but the problem with the Kenyan trial for the former product and the slow progress on getting allergens for the latter may mean that these products are not as quickly forthcoming as management expects. In conclusion, this is potentially a very exciting company but the short term issues make it a bit too risky for me at the moment.