Omega Diagnostics has now released its interim results for the year ending 2015.

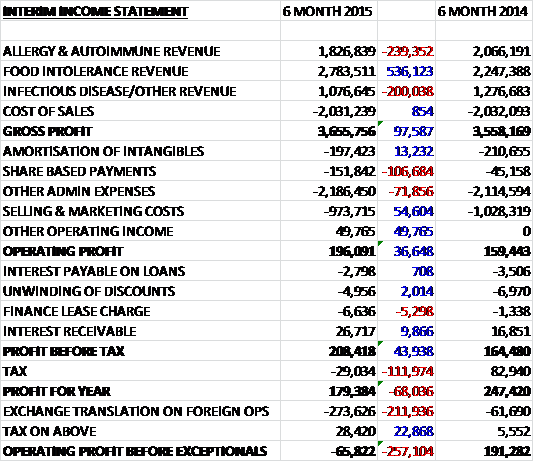

Revenues were up slightly when compared to the first half of last year as the trend seen last year continues with a £536K increase in food intolerance sales being partially offset by declines in the other segments, despite the adverse £250K affect that strengthening Sterling had on revenues. Cost of sales was just about flat to give a gross profit some £98K higher than last time. We then see a £107K increase in share based payments and a £72K growth in other admin expenses, partially offset by the occurrence of nearly £50K worth of other operating income and a £55K decline in selling and marketing cots to give an operating profit of £196K, a growth of £37K before improving finance costs improved profits further to £44K. Unfortunately all this was wiped out by a tax charge compared to the rebate last time due in part to a movement on deferred tax arising from share based payments and a lower R&D tax credit so that profit for the year was £112K lower than in the first six months of 2014 at £179K.

When compared to the end point of last year, total assets fell by £36K due to a £370K increase in intangible assets, a £218K increase in inventories, a £157K increase in property, plant & equipment and a £122K increase in deferred tax assets all being more than offset by a £980K fall in cash levels. Liabilities also fell during the period, driven by a £140K fall in borrowings but the end result is a £284K decline in net tangible assets to £6.9M.

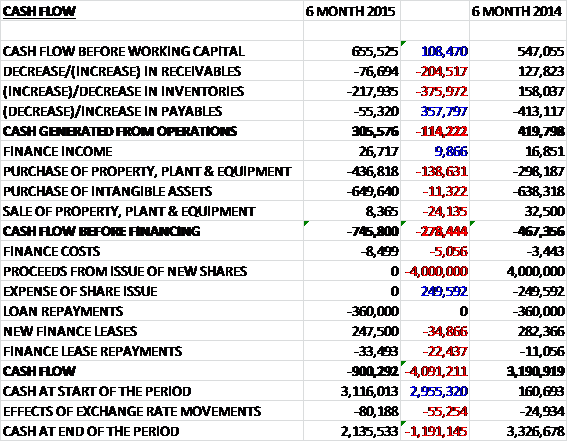

Before movements in working capital, cash profits increased by £108K to £656K but this was then knocked down, mainly from an increase in inventories, to £306K, a fall of £114K when compared to the first six months of last year. This cash flow was nowhere near enough to pay for the £650K of intangible assets and the £437K spent on property, plant and equipment so that there was a cash outflow of £746K before financing, where the group continued to pay back the loan, which was partially offset by a net cash inflow from finance leases to give a cash outflow for the year of £900K and a cash level at the end of the half of £2.1M.

Adjusted profits at the allergy and autoimmune business fell by £170K to just £28K. The business continues to operate with reimbursement pressures in Germany leading to a reduction in sales across some regions. Adjusted profits at the food intolerance business grew by £383K to £956K. There are a number of key customers in the EU, North America and BRIC countries that are supporting a sustainable increase in product volumes that leads to an overall increase in profitability. Adjusted losses at the infectious disease business were £150K, an adverse movement of £172K when compared to the first half of last year. The division was impacted by some raw material supply delays which led to back orders in the period which will have to be fulfilled in the second half of the year.

Following the sub-optimal results of the Visitect CD4 test in Kenya that was reported last time, subsequent batches have yielded variable results when tested on patient blood samples and the group have found that the combination of an outsourced manufacturing process, an in-house assembly process and the need to test finished devices on patient samples at a UK lab has led to lead times which are fairly prohibitive when needing to test product refinements on an iterative basis.

The group have therefore made a number of changes in order to commercialise the device in the shortest timeframe, including access to expert resources in rapid test development and temporarily bringing control of the outsourced manufacturing process in-house. They are also looking to fully understand how the test was manufactured on the semi-manual bench top basis by the Burnet institute in the first place. Understandably the group are focusing all resources on resolving the issues with CD4 before looking to expand into other diseases like Syphilis that was mentioned last time.

Good progress was made on the allergy development programme with 22 allergens having completed their claim support work and a further 5 having completed optimisation which means there are now 27 allergens now ready to be used on the iSYS instrument with equivalent performance to the market leading product. Those five are now in a queue waiting to undergo claim support work with the remaining 13 needed to complete the launch panel having been identified and in various stages of optimisation. An in-house team of scientists have been recruited to increase momentum in this work. The timeline to optimise the remaining 13 allergens is dependent on sourcing allergen extract preparations of sufficient quality to achieve the performance design goals when incorporated into the assay system.

The group are confident of the performance of the core business in the second half of the year, particularly in the food intolerance business where they have built traction with new customers over recent years. The delay to the Visitect CD4 device is frustrating but the actions were taken so that the market launch of the product went without a hitch, which is of course the correct thing to do, and the board remain convinced that there is a good market opportunity for the product and their outlook for CD4 remains unchanged.

These results are a little mixed. Profits would have been improved if were not for the tax charge but whilst net assets improved, net tangible assets fell when compared to the end point of last year. Due to a build in inventory, the operational cash flow was disappointing and no-where near enough to cover the group’s capital expenditure. The food intolerance division continues to go from strength to strength but the other two divisions continued to experience problems with ongoing reimbursement constraints in Germany affecting the allergy business and the infectious disease business now being affected by raw material delays. The real problems seem to be the delays in development of both the CD4 test and the iSYS instrument with the former still looking a long way from commercialisation after disappointing field tests. The iSYS instrument at least seems to be making progress with just 13 allergens still to develop, however I would be very surprised if this happened before the end of the year and in conclusion although I remain confident that this could be a good investment one day, it is hard to see any near term catalysts for the moment and I will continue a watching brief for now.

The chart looks pretty uninspiring at the moment with the share price well below both the 50 day and 200 day moving averages.

On the 1st June the group released a development update. The company has continued to test Visitect CD4 devices on a large number of patient samples with the aim of optimising performance and deciding on a suitable in-house manufacturing process. It has now made three pilot batches of the devices, all of which yielded comparable results that demonstrate the system is capable of meeting the company’s internal performance goals when tested on HIV positive patients and this investigation phase in now complete. The outcome has been the selection of in-house manufacturing processes which are scalable and will be subject to verification and validation leading to the release of test devices for re-evaluation in the field.

With regards to the Allersys device, the group now has 32 allergens that have been optimised to show equivalent performance to the market leading product. Of these, 22 have completed their claim support work. The manufacturing process and recent amendments to the instrument software have been validated for full scale manufacture and the group now has commercial quantities for 27 allergens and associated reagents which have all passed internal quality control procedures. These allergens will be used in beta evaluation sites in Spain and Italy, planned in June and July respectively so it seems some useful progress is being made here and I now own some shares.