During the period, Creston has changed its segmental makeup with the divisions now consisting of Communications & Insight which delivers a range of digital technology based marketing solutions with services including advertising, brand strategy, CRM, digital marketing, local marketing, market research, PR and social media marketing. The Health division provides an integrated communications solution to the healthcare and pharmaceutical sectors and offers services including advertising, advocacy, digital marketing, PR, reputational management and medical education. The group has now released its interim results for the year ending 2015.

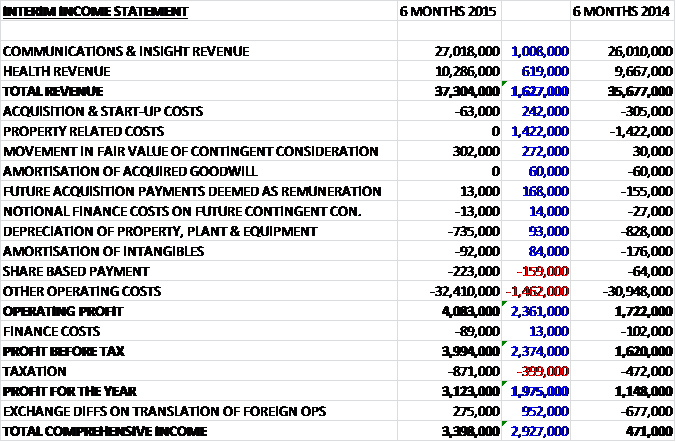

Overall revenue increased year on year with a £1M growth in communications & insight revenue and a £619K increase in health revenue. We then see a reduction in most one-off costs such a £242K fall in acquisition costs and the lack of £1.4m charge for property related items. We also see a £168K positive swing in future acquisition payments, partially offset by an increase in share based payments and a £1.5M growth in other operating costs. Finance costs were broadly flat but taxation did increase on last time (and management expects a slightly higher rate going forward due to higher levels of tax on the growing US income) to give a profit for the half year of £3.1M, some £2M more than in the first half of last year, although it should be noted that if we take the non-underlying costs out from last year the performance would be broadly similar.

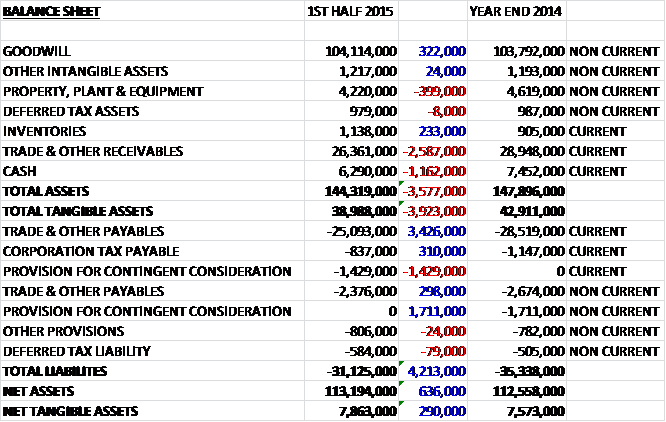

When compared to the end point of last year, total assets fell by £3.6M driven by a £2.6M fall in receivables and a £1.2M decline in cash levels. Liabilities also fell during the period due to a £3.7M decline in payables and a net £300K decline in the provision for contingent consideration which has now become due within the year. The end result is a small £290K in net tangible assets to £7.9M.

Before movements in working capital, cash profits increased by £1.8M to £4.8M. This was eroded somewhat by a fall in payables and after a smaller tax bill, the net cash from operations increased by £8.4M to £2.2M. This was easily enough to cover the capital expenditure, which fell year on year to give a free cash flow of £1.8M. The group then spent the majority of this on dividends but also spent £1.2M the purchase of treasury shares which meant that there was a £1.1M cash outflow for the period to give a decent cash pile of £6.3M at the period end.

The Communications and Insight business posted a profit before tax of £3.2M, a growth of £500K when compared to the first half of 2014 but on an underlying basis, after the impact of higher property costs last year, this represents a £400K fall in profit. Significant new business wins during the period included work for McCarthy & Stone, Sony Mobile, Arthritis Research, Allianz, BskyB, Bentley, McCain, Activision, Vertu, Sainsbury’s Energy and the Department for Work and Pensions. Revenue from international work grew by 4% to make up 20% of the division’s overall revenues and this is an area that management are looking to grow following the partnership agreement with Serviceplan.

The Health business showed a profit before tax of £2M, an £800K improvement when compared to the same period of last year which included a revaluation credit for the contingent consideration for DJM Unlimited due to project delays and cancellations partly in relation to a failed clinical trial, without which profits would have increased by £200K to £1.7M. In the US the health business maintained its good new business performance with wins during the period including work for the National Meningitis Association, Parent Project Muscular Dystrophy and CDC. In the UK new client work during the period included major wins from Sanofi, Baxter, Bayer, Pfizer and Novartis.

The group is somewhat susceptible to currency exchange changes and the strengthening of Sterling against the US Dollar had a material impact on results. During the period the fact that results included the full effect of higher property costs relating to the co-location of the group’s London based companies affected profits. There is a slight cautionary warning that the increased reliance on digital revenues, which accounted for over half of sales, can lead to “variability in annual income over the course of a client relationship”. An example of this is an instruction that begins as a large website design and build will usually progress to a content management, hosting and maintenance instruction.

The earn out obligations of about £1.4M in cash become due in July 2015 and there are other potential charges next year as the launch of Creston Unlimited and the group-wide rebranding of their service offerings has an associated project cost of £500K, the majority of which will be incurred in the second half of the year.

A number of board changes took effect during the period and after the period end. Barrie Brien was promoted to CEO in April and Kathryn Herrick joined the board and group as CFO in July. David Grigson stepped down as Chairman in September and was replaced by Richard Huntingford, an existing director for the past three years. From November, Kate Burns joined the board as non-executive director and brings with her good experience in digital media and technology with senior level experience at Google and AOL and the will be replacing David Marshall who steps down after being with group since 2001. This is an interesting one as David was Chairman when the group formed and is the Western Selection director, which is one of the large shareholders – does this mean that Western Selection are no longer interested in maintaining their position on their board or even their shareholding?

After the period end the group signed a partnership agreement with the German owned international marketing communications group, Serviceplan. The business has no UK or US presence and so Creston will serve their clients in these markets with Serviceplan assisting Creston’s clients in Europe with the plan of referring each other’s clients depending on their location and sometimes jointly pitching for clients. Already the two companies have successfully partnered to win CRM assignments for Danone in Germany and the Middle East.

Going forward, the group are looking to invest and evolve their offer through organic growth and selective acquisitions and they look to deliver more digital based marketing solutions. The growth momentum reported in the second half of last year has continued and it is anticipated that revenues will increase in the second half of this year. While the board remain cautious in light of the global macro-economic climate it is reported that current trading is in line with expectations for the full year.

The shares are currently yielding 3.5% after a 13% increase in the interim dividend. At the period there was no debt and the group had a net cash position of £6.3M, a decline of £1.1M when compared to the end point of last year.

Overall then, this seems to be a pretty decent update. Reported profits increased when compared to the first half of last year but underlying profits seem to be broadly similar. Similarly, net assets showed a modest improvement but the cash flow seems to be much better with an increased operational cash flow and enough free cash to cover the dividends. It does not cover the shares purchased for the treasury, however, so there is still work to do to stop that cash pile being depleted. Again, there have been some changes at the board level with David Marshall leaving and Kate Burns arriving. Kate seems to have a lot of good relevant experience so she seems to be a good appointment and while the loss of David is probably not much of a problem, the fact that he represents a large shareholder who no longer has representation on the board could suggest that Western Selection will look to offload their shares.

Going forward, the guidance seems mixed. Whilst revenues are thought to increase in the second half, there are also a few cash costs to watch out for such as the earn out obligations and the expense surrounding the launch of the Creston Unlimited brand. Also, I am not sure I like the statement about the variability in annual income over the course of a client relationship comment. Whilst this really is to be expected, pointing this out seems as though it could be paving the way for a profit warning. In any event, I am keeping a watching brief on the shares.

On the 3rd February the group released an interim management statement covering Q3 trading. After a decent H1 in which revenues grew by 5%, growth in Q3 was lower, with group revenues up just 1% giving a year to date increase of 3%. The Communications & Insight business performed well but within the UK Health business, revenue performance was affected by some client budget cuts and project delays which are likely to continue into Q4. As a consequence of this, the board expects full year group revenue growth to be below current expectations. Operating costs have been reduced and based on current trading, the board expects group headline profit before to tax to be broadly in line with expectations.

The group continued to win new business with Mclaren and Superfast Broadband, along with contracts with Vue, Barilla and La Roche which were added after the end of the half year. In addition work with Sony Mobile and Novartis has been expanded. As mentioned previously, digital work can lead to variability in annual income over the course of a client’s relationship which means the group is pursuing a departure from pure marketing services to include consultancy led marketing advice which should lead to greater pipeline visibility in the future.

Going forward, whilst the marketing services sector remains vulnerable to the impact of macro-economic events, the board is confident that the group is well placed to deliver long-term growth. I do rather agree with them but I see some short term volatility caused by the “revenue warning” issued here and continue to watch from the sidelines.

As we can see, the last updated halted the appreciation of the shares but they seem to have stabilised since then.

On the 9th April it was announced that DBay Advisors had purchased 161,000 shares in the company at a value of about £188K to give them a 19% interest in the company. This was a modest purchase but notable because DBay really seem to be building a stake here – I wonder what their plans are?

On the 22nd April the group released a trading update covering the full year results. They are expected to be in line with (reduced) expectations with revenue growing by £2M to £76.9M, an increase in headline profit and EPS and a cash level of £8.3M at the year end. The group also announced the acquisition of 51% of How Splendid Ltd, a London based design and development consultancy. There is an initial cash consideration of £8.7M that will be funded from existing cash resources and the acquired group is expected to retain net assets of £2.1M, including cash of £1M. There is a deferred payment of up to £7M in June 2017 based on average profit levels. Creston will have a call option over 24% from April 2017 for a value of up to £8.6M and the remaining 25% from April 2019 for £11.9M.

Last year, Splendid received revenues of £4M and profits of £1.2M but this year it has experienced material growth so actual revenues and profits are higher than this. The acquisition will be earnings enhancing in the current financial year which is good to hear. The acquired group has a variety of clients including Barclaycard, Boots, EBay, Gamesys, News UK, Skrill, SSE and Star Alliance and focuses on the user experience between a brand and a customer. There are expected to be significant cross selling opportunities with this acquisition which seems a really good fit. I have some reservations about the potential total cost of this deal but there is little doubt that it seems like a good, earnings enhancing acquisition and this will encourage me to look at the shares with more interest going forward, despite the rather lacklustre results that are likely to be reported in June.

On the 5th June the group announced that Nigel Lingwood will join the group as non-executive director and become senior independent director. He currently works as finance director at Diploma, a role he has been in since 2001 where he has seen the growth of the business from a FTSE small cap company to a FTSE-250 constituent. He will replace Andrew Dougal who will step down as a non-executive director after being with the company since 2006. This certainly seems like a high-calibre appointment but I am not sure how much time he can dedicate to the role given his senior position at Diploma.