Majestic Wines retails wines, beers and spirits through retail outlets in the UK and France along with trade sales in the UK. Of the three divisions, Majestic Wine Warehouse is a UK based wine retailer, Lay & Wheeler is a specialist in the fine wine market and Majestic Wine Calais operates retail units in Northern France servicing the UK cross-channel market. En primeur refers to the process of purchasing wines early before they are bottled and released onto the market which gives consumers the opportunity to secure wines that may be in limited quantity and difficult to acquire after release. Payments to suppliers are treated as prepayments and receipts from customers are defined as deferred income until the wines are available to customers. The group is listed on the AIM market having been founded in 1980 and it has now released its final results for the year ending 2014.

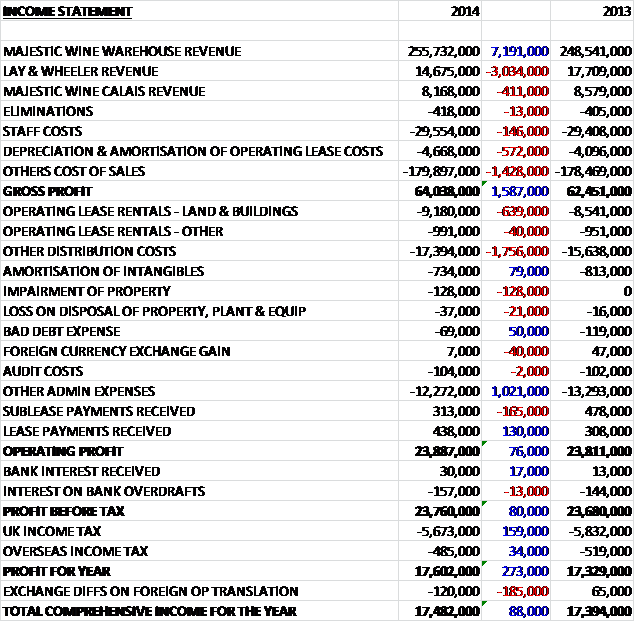

Overall revenues increased when compared to last year as a £7.2M growth in core majestic wine sales was partially offset by a £3M decline in Lay & Wheeler revenue and a £411K fall in Calais revenue. Depreciation and other cost of sales also increased somewhat to give a gross profit some £1.6M above that of last year. We then see a £679K increase in operating lease rentals and a £1.8M hike in other distribution costs due to the ongoing rollout of the store estate, partially offset by lower admin costs due to a lower level of accrual for variable remuneration to the management teams to give an operating profit of £23.9M, which remained broadly flat year on year with just a £76K increase. After finance costs and a fall in the tax paid, the profit for the year grew by £273K at £17.6M.

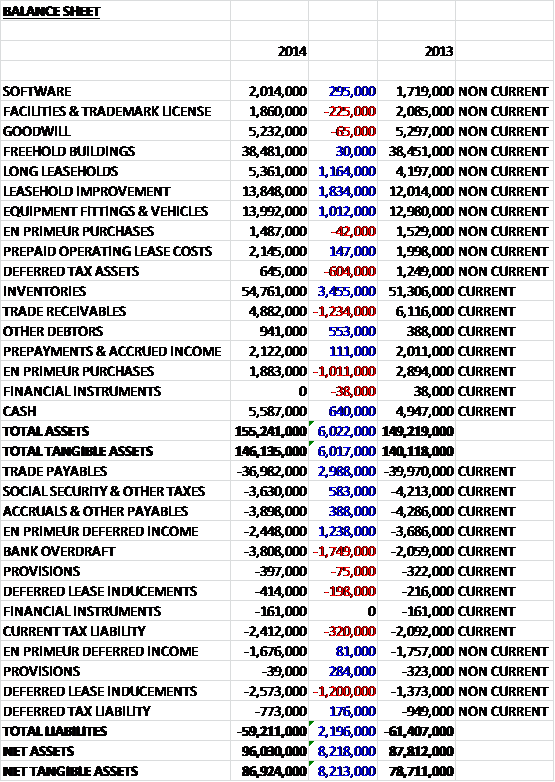

When compared to the end point of last year, total assets increased by £6M driven by a £3.5M increase in inventories, a £1.8M growth in the value of leasehold improvements, a £1.2M increase in the value of long leasehold properties and a £1M increase in equipment and fittings, partially offset by a £1.2M fall in trade receivables and a £1M decline in en primeur purchases. Liabilities fell during the year as trade payables fell by £3M and en primeur deferred income declined by £1.2M, partially offset by a £1.7M increase in bank overdrafts and a £1.2M growth in deferred lease inducements which are rent free periods and premiums received from lessors in respect of operating leases. The end result was an impressive £8.2M increase in net tangible assets to £86.9M which seems looks like a strong balance sheet to me. Having said that, it is worth noting that there are just under £90M worth of operating lease commitments not on the balance sheet with some £5M expected to be received from sub-let properties.

Before movements in working capital, cash profits fell by £3.6M to £26.8M before this was eroded by an increase in inventories and a fall in payables, being blamed on the timing of Easter, to give a cash generated from operations some £4.2M lower at £23.6M which after tax became £18.2M. This was easily enough to pay for the net £10.3M of capital expenditure (down from last year due to the lack of the £2.1M for the acquisition of the long leasehold of the new head office that occurred in 2013) and the free cash flow for the year was £8.4M, a fall of £660K when compared to last year. This was not enough to cover the dividends paid out, though, which gave rise to a £1.1M cash outflow during 2014 to lease a cash level of £1.8M at the end of the year which does not leave much headroom, although there was undrawn short term facilities of £2.1M at the year end.

The market in which the group operates has been challenging, as can be seen by the marginal decline in UK sales with a particularly slow January and February being experienced following a positive Christmas trading period. Despite this, they have managed to increase market share from 4.1% to 4.2% during the year with the value of still wine sold at the group increasing by 4.9% compared to a market that grew 1.3% but contracted in volume terms with the increased value coming from inflation due to increasing alcohol duties. In addition costs have increased as the world’s grape harvests were weaker due to poor weather combined with rising demand from the Far East.

The Majestic Wine Warehouses posted an operating profit of £21.4M, an increase of £800K when compared to last year. The average bottle price of still wine purchased increased from £7.56 to £7.94 while average transaction prices increased by £1 to £129. During the year the group opened 12 new stores with two more after the period end to give a total of 206 stores in the UK with the medium term target being 330 locations. The commercial offering has done well with sales increasing by 20.6% to £37.3M and management believe that there are good opportunities to improve market share further with the group investing in the commercial sales team. Online sales grew by 5.8% year on year and now represent over 11% of UK retail sales. This increase represents a slow down when compared to previous years as further investment was made and the new website was launched.

The Lay & Wheeler business had an operating profit of £1M, a fall of £700K when compared to 2013. This decline was due to the fact that last year included sales from the successful Bordeaux 2010 vintage as the wine was delivered to customers but subsequent vintages saw a slower level of demand reflecting their lower quality. As a result management expects that profitability from this business will remain at its current level until another strong Bordeaux vintage is seen – not a growth area for the group then. The Majestic Wine Calais division gave a profit of £1.5M, a small decline of £100K when compared to last year with like for like sales on a constant currency basis declining by 5.7%.

There are a number of initiatives that are being devised by the group. One new feature is the ability for customers to browse the website based on what’s in stock at the local store that day as all the wines, spirits and beers in stock are listed online. Another innovation is recommendations from experts for customers who like one particular wine. The group have improved the click and collect offering with customers being able to pay by Paypal and can collect in store simply by showing their ID. Finally with the new website platform comes a revamped mobile optimised website with the added ability to view all content on each local store’s webpage and enhanced control of customer account details.

The group is somewhat susceptible to foreign currency changes due to the fact that most of the wines are imported from overseas, with a 5% weakening of Sterling against the Euro reducing profits by £848K. The main competition comes from grocers who account for 84% of the wine sold in the UK by volume and this has to be the main issue facing the wine merchants at the moment, although the focus on individual customer service certainly differentiates Majestic from the likes of Tesco and Asda. Another possible risk is the regulatory environment surrounding alcohol and the possibility for further increases in duty which could either squeeze margins or reduce demand as prices increase.

The group has committed to some £2M of capital expenditure for next year which is not an unusual amount. After the end of the balance sheet date the group successfully moved their head office and also relocated their distribution centre to a more modern and larger facility in Hemel Hempstead which has the capacity to handle a significant volume increase from the potential growth of the multi-channel offering. Focus in the coming year will be to make the investments necessary to increase the store footprint, grow ecommerce operations, increase sales to business customers and driving the fine wine offer. In the short term the cost of these investments will lead to flatter profit growth in 2015 with a return to profit growth from 2016 as the benefit from the investments start to take effect.

At the current share price the shares trade on a P/E ratio of 11.6 but this increases to 11.9 on next year’s consensus forecast. The shares currently yield 5.2% in dividends, which is a good return and this is predicted to remain the same next year. At the end of the year net cash stood at £1.8M, a decline of £1.1M when compared to the end point of last year.

Overall then, this is a fairly solid set of results. Profits were broadly flat year on year and net assets increased, although in common with many retailers, there is a lot of finance lease obligations off the balance sheet. Operational cash flow fell year on year and despite being quite cash generative, the free cash flow does not quite cover the dividends which have remained at a historically high rate. Wine retail is quite a tricky place to be as the market is falling in volume terms with prices increasing due to poor grape harvests but against this backdrop, Majestic is improving market share. The core warehouse offering is doing well but performance is not so good at the French operation and Lay & Wheeler due to the relatively poor recent Bordeaux vintages. Going forwards the board have warned that increased investment should lead to flatter profit growth in the coming year and the ever competitive supermarkets are engaging in a major price war, both of which means that I feel Majestic is probably best watched from the sidelines for the moment, despite the decent dividend yield.