Air Partner has now released its final results for the year ending 2015.

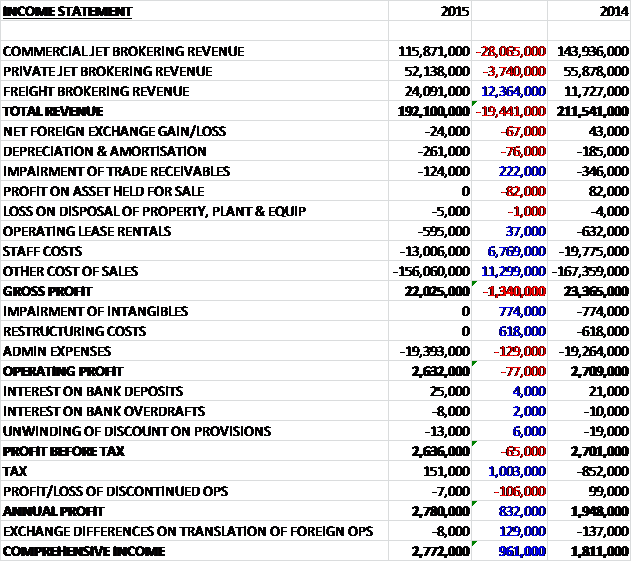

Overall revenues fell by £19.4M as a £12.4M increase in freight brokering sales was more than offset by a £28.1M decline in commercial jet sales and a £3.7M fall in private jet revenues. Cost of sales also fell, however to give a gross profit just £1.3M below that of last year. Underlying admin expenses increased slightly but there was a lack of impairments and restructuring costs that occurred last year which meant that profit before tax fell by 65K to £2.6M. Due to a tax rebate this year compared to a tax payment last year, however, the profit for the year actually increased by £832K to £2.8M.

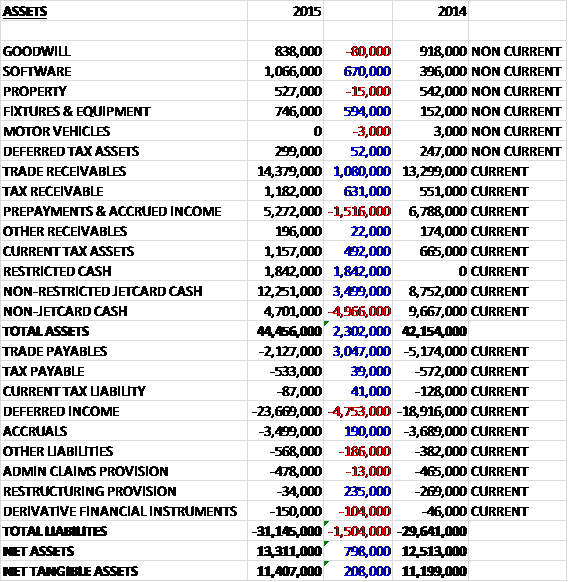

When compared to the end point of last year, total assets increased by £2.3M, driven by a £3.5M increase in non-restricted Jet card cash, a £1.8M growth in restricted cash and a £631K increase in tax receivable, partially offset by a £5M fall in non-Jetcard cash and a £1.5M decline in prepayments and accrued income. Liabilities also increased during the year as a £4.8M increase in deferred income relating to the increased Jetcard sales was partially offset by a £3M fall in trade payables. The end result is a net tangible asset level some £208K higher at £11.4M. It should be noted that the fall in non-jet card cash was driven by a number of ad hoc commercial jet projects in Germany and the servicing of a major government aid contract in the final quarter of the year, which have had a temporary effect on cash balances. There are also £2.4M of operating leases not included on the balance sheet but this relatively modest figure should not cause too much of a problem.

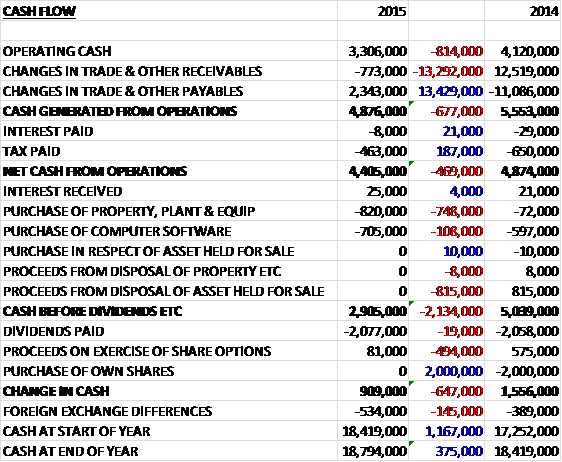

Before movements in working capital, cash profits fell by £814K to £3.3M. The operational cash flow was then improved by an improved payables situation and a reduction in the amount of tax paid so that net cash from operations fell by £469K to £4.4M. This was more than enough to pay for the tangible assets and CRM software to give a free cash flow of £2.9M. The bulk of this was spent on dividends to leave a £909K cash inflow for the year which seems like a decent performance.

In Commercial Jets, the reduction of the cost base, the recruitment of new staff and improved trading conditions has led to some confidence in the outlook for the division after a poor year. Private Jets continued to progress, driven by the popularity of the Jetcard product and the Freight division showed strong improvement from the low base of last year as the global economy continued to improve and the group have added to the sales team in this division.

Underlying operating profit at the Commercial Jet business fell by 31.6% to £2.7M. The reduction was due to few material one-off contracts, particularly in the UK and the US, together with the impact of a reduced tour operating programme in the French business. The CEO has now personally taken responsibility of the UK commercial jet division and a number of steps have been taken to re-focus operations, reduce costs and invest in new, experienced staff. These actions have apparently contributed towards the improved trading performance in the second half of the year. During the year Italy achieved its highest ever profits as a result of a successful tour operating programme and Germany achieved its strongest ever set of results due to a number of car launches.

Despite the reduction in tour operating revenues in France, strong progress was made in Italy and Austria with an increased programme in France for 2015 indicating that the set back there may be temporary. Oil and Gas activity produced consistent revenues compared to last year with a 24% increase in gross profit with a good contract win in the second half of the year with a major exploration company. During the year, worldwide government relationships continued to generate contract wins but generated lower levels of profits that the group expects will continue going forward.

In Private Jet broking, the underlying operating profit fell by 51.3% to £800K. The amount of deposits on Jetcard increased to £14.1M from £8.8M last year. Revenues from the card are not recognised until the customer has flown the hours so despite a 153% increase in new deposits and a 2% increase in renewals from existing customers, utilisation increased by just 3% year on year. The increased deposits this year bode well for revenues next year, however. In ad hoc brokering, the picture has been more difficult. The US business suffered as a result of decreased flying by one of the group’s major corporate clients and in Europe the overall market has contracted slightly reflecting uncertainty in the Eurozone. The group has taken action to reduce the cost base in these areas to mitigate these trends.

The Freight broking division made an underlying operating profit of £400K, an improvement on the £100K loss made last year. This growth reflects new business wins generated by the investment made in more sales staff. The Red Track technology which aids the aircraft on the ground business, and the continuation of the work with government global aid agencies has helped build strong relationships with freight forwarders which has been a key contribution to the turnaround seen in the division.

Some examples of the contracts that have been undertaken by the group include flights chartered for football teams where they source the aircraft, arrange the arrival and departure process, brand the interior of the plane with the team colours and deliver bespoke catering to meet the nutritional needs of the players. Departure times are flexible due to the possibility of the matches going in to extra time. Another contract involved the hire of a private jet for a wedding. The jet was stocked with the bride’s favourite food and champagne, some 50 guests were flown in by VIP aircraft and after the wedding itself, the bride and groom were flown off to their honeymoon with the jet dressed with “just married” headrest covers. When the couple decided they wanted to extend their honeymoon for a couple of days, the group arranged the private jet flight home (how the other half live, huh?!).

At the other end of the scale, following the outbreak of Ebola in West Africa, the group flew over 100 aid flights to the region along with building equipment that was used to build five treatment centres. Over a period of nine weeks, the group flew a client’s 20,000 guests from different airports to a product launch in Greece which included gate buffets at airports, direct transport of luggage to hotels, and en-route hotel check in. Another project involved a jet card owner who booked an aircraft to the French Alps that could land near their favourite ski slopes and carry their ski equipment with the service including a weather watch for the client and 20 minute check in. In Madagascar, following a power blackout, the group flew a generator system from a UK warehouse to the affected region, including a 500Km truck journey to arrive at the destination on time.

Although the aviation market can suffer as a result of geo-political uncertainties, for Air Partner this can be an opportunity, for example, the movement of troops and equipment in military conflicts, evacuation of personnel form disaster zones, the transport of aid and the repatriation of citizens in response to politically driven immigration programmes. Overall, though, demand for commercial passenger traffic and cargo is growing globally, but this is not the case in Europe due to the ongoing difficulties being faced by certain Eurozone members. Freight traffic is one the rise generally. Similarly, the private jet outlook is mixed. The US is a strong, albeit competitive market while the picture in Europe is less buoyant, shrinking by 0.5% when compared to 2013, partly as a result of the instability in Russia and Ukraine

One issue that has the potential to adversely affect aircraft broking is that the rise of technology has enabled some customers to book their flight without using a broker and there are some companies attempting to offer this solution, cutting out the need of a broker at all. Often, though, passenger needs are challenging and jet itineraries are often complex and subject to change which is something that currently can only be managed be experienced brokers. The group has also seen operators looking to charter aircraft direct to customers which could be an issue if it is a trend that continues to increase. The main risk in the short term, however, remains global economic conditions with charters continuing to be impacted by economic instability in major world markets.

The main reason that the group managed to improve profits when compared to last year is the tax rebate. The group has received £500K from an R&D tax claim arising from its investment in technology projects, £200K from a one-off tax credit arising from the treatment of Jet Card deposits in the US, and £200K from the recognition of deferred tax assets from capital allowances and losses in France. Although some of these are one-offs the group is actively reviewing its tax structure going forward which might results in further improvements to the amount of tax paid.

There have been a number of board changes. Tony Mack retired from the board at the last AGM but remains as life president of the company, whatever that means. Gavin Charles left the business from his role as CFO with Neil Morris, the former group financial controller, being appointed as his replacement. Non-executive director Chuck Pollard resigned in December after spending five years in his role in order to take up a position of CEO at Arthur J. Gallagher International. He is replaced by Peter Saunders. Peter is also non-executive director at Canadian Tire Corp, Godiva Chocolates, Total Wines and Jack Wills having been former CEO at Body Shop, so that is quite an eclectic list but he brings experience in marketing and customer service.

So far this year, trading is in line with expectations with an improvement seen in France and the momentum generated in Italy continuing, and taken with the level of forward bookings, including the large oil and gas project that will commence this year, the board begin the year with a degree of optimism. After a 10% increase in the total dividend paid this year, the shares are now yielding an impressive 6.2% and the P/E ratio stands at 13.4, which doesn’t seem too bad. Unfortunately I could not find any broker estimates for next year.

Overall then, this is a mixed set of results characterised by a very poor first half of the year, followed by improvements in the second half. Profits were actually up but this was due to a tax rebate and the lack of the restructuring costs that occurred last year. Net assets increased slightly, which was encouraging and despite a fall in both the operational and free cash flow, the group remains nicely cash generative. The commercial jets division suffered due to less large one-off contracts and a poor performance in the French travel agency business. The private jet profits fell due to less usage from a major US client and general malaise in Europe, but increased jet card deposits bode well going forward.

There are a number of headwinds, the fact that there are some users cutting out the involvement of brokers is concerning and the market remains susceptible to general economic conditions, plus the ongoing problems in Russia is affecting private jet usage there. So far this year, however, trading has been decent with a large oil and gas contract won at the end of last year and an improvement in conditions in France driving the performance. The dividend yield is excellent, and it seems fairly well covered by earnings so I am happy to remain holding here.

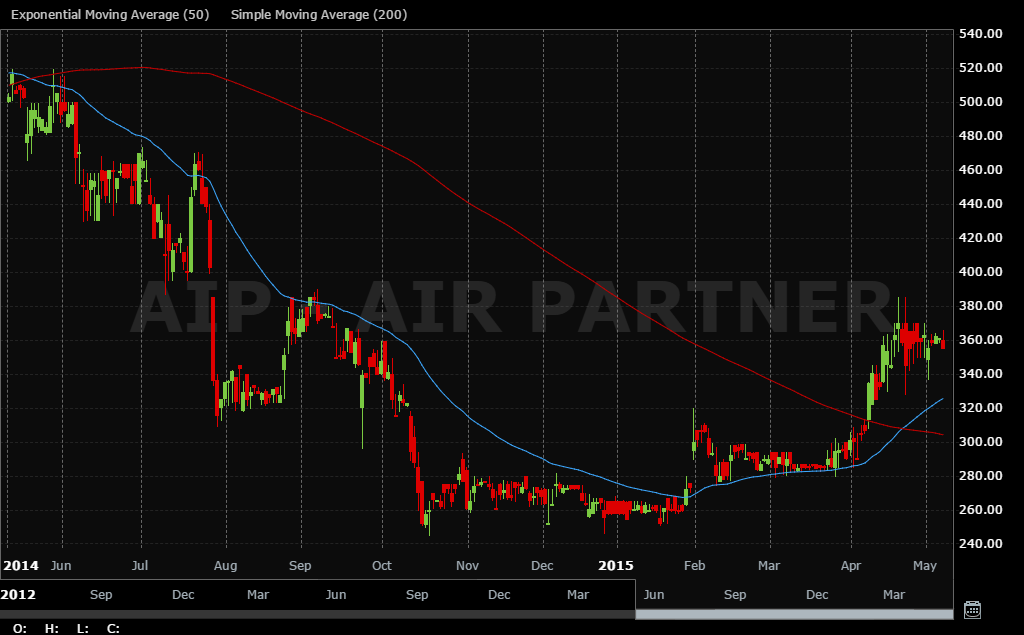

The chart continues to look promising too, the shares have punched up through the 200 day moving average and are well up on their lows at the start of the year but remain considerably lower than at the beginning of 2014.

On the 13th May the group announced the acquisition of Cabot Aviation Services for a total consideration of £1.2M, £600K of which will be paid in cash on completion with the other £600K payable in Air Partner shares over the next five years. Cabot’s main business is acting as an agent and broker to airlines and other aircraft owners such as banks, operating lessors, manufacturers, insolvency practitioners and individuals to dispose of their surplus aircraft. IT also advised clients on the acquisition of aircraft and their fleet management process. Air Partners’ existing aircraft remarketing operations are predominantly in the short-term wet lease market but the acquisition adds significant aircraft sales and dry lease expertise to the group. The acquired company will continue trading as Cabot, retain its CEO and Chairman and absorb Air Partner’s current remarketing operations.

Cabot achieved a profit before tax of £383K in 2015 and should be earnings enhancing to the group during the current year ending 2016. This seems like a great acquisition at an attractive price so should add value going forward.

On the 1st May it was announced that after retiring from the board and becoming life president of the company, Tony Mack sold all of his 700,000 shares which had equated to over 7% of the total equity of shares which is a substantial amount.

On the 4th June the group released an AGM statement. Trading so far this year has been at a similar level to the end of last year and given the forward bookings, the board remains optimistic about their prospects for the rest of the year. The recent Cabot acquisition is starting to show clear benefits to the group’s customers. While there is limited visibility, the group has made a solid start to the year and is maintaining a positive net cash position. A decent update, but it has to be said that there is not that much to get excited about here.

On the 31st July the group gave a trading update covering the first half of the year. Trading has been in line with expectations and pre-tax profit is expected to be at least £2M compared to £1.1M in the first half of last year.

On the 19th August the group announced the acquisition of Baines Simmons Ltd, an aviation safety consultant, for a total consideration of £6M with £5.4M initially in cash and a further £600K of deferred consideration payable in January 2018 dependent on performance criteria. The acquisition has been funded from a combination of existing cash resources and a £3.6M debt facility provided by RBS. Baines Simmons achieved a profit before tax of £700K last year and the group expects the acquisition to be earnings enhancing in its first full year of ownership.

Baines Simmons specialises in aviation regulation, compliance and safety management, advising clients across civil and military markets such as KLM, SAS, Thomas Cook, British Airways, Virgin Atlantic, the Isle of Man government, BAE, the MoD, Rolls Royce, the RAF, Airbus, the European Aviation Safety Agency and the UK Military Aviation Authority. Following the acquisition, the business will continue to be managed by its current executive team and will report its results as a new segment.

Baines Simmons assists clients by de-risking complex organisations, ensuring that high safety performance standards are an integral part of an organisation’s approach to business. They designed, built and continue to support the Isle of Man Aircraft Registry on behalf of the Isle of Man government. Since 2007, over 800 aircraft have registered and airworthiness surveyors have completed over 2,200 surveys, recommending Certificate of Airworthiness for issue, renewal or export.

Overall this looks like an interesting acquisition. It is nicely profitable and seems a good complimentary business are for the group to be involved in, although whether there are many synergies to be had is debatable given it sounds like it will continue to operate pretty much as its own business.