Sainsbury has now released its final results for the year ending 2015.

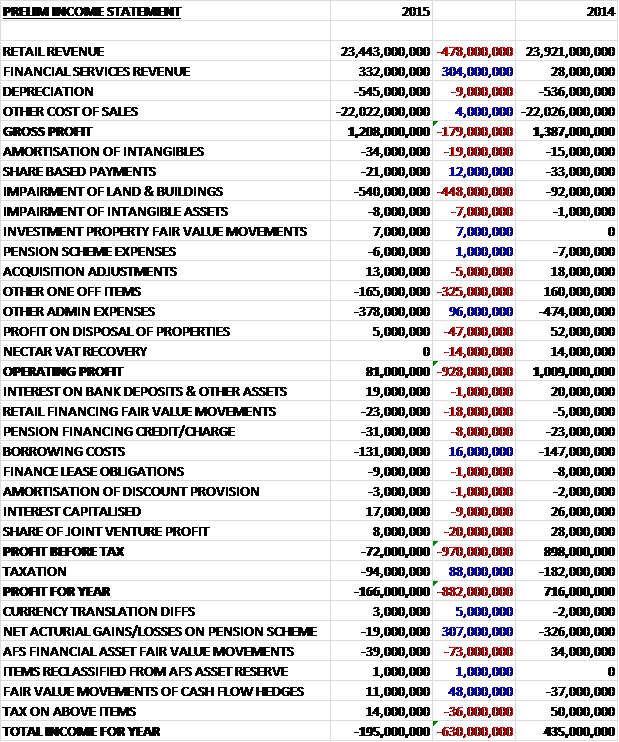

Overall sales fell when compared to last year as a £304K increase in financial services revenue, reflecting a whole year of ownership of Sainsbury’s Bank, was more than offset by a £478K decline in retail revenue. Cost of sales was broadly flat year on year to give a gross profit some £179K lower than in 2014. We then see underlying admin expenses fall somewhat but the real damage is done by the £540K impairment of land & buildings, and the £165K of other one-off items to give an operating profit of just £81M, a decline of £928M when compared to last year. Profits at the joint ventures collapsed by £20M and various increases in finance costs were offset by a reduction in tax to give an overall loss for the year of £166M, a negative £882M swing when compared to 2014.

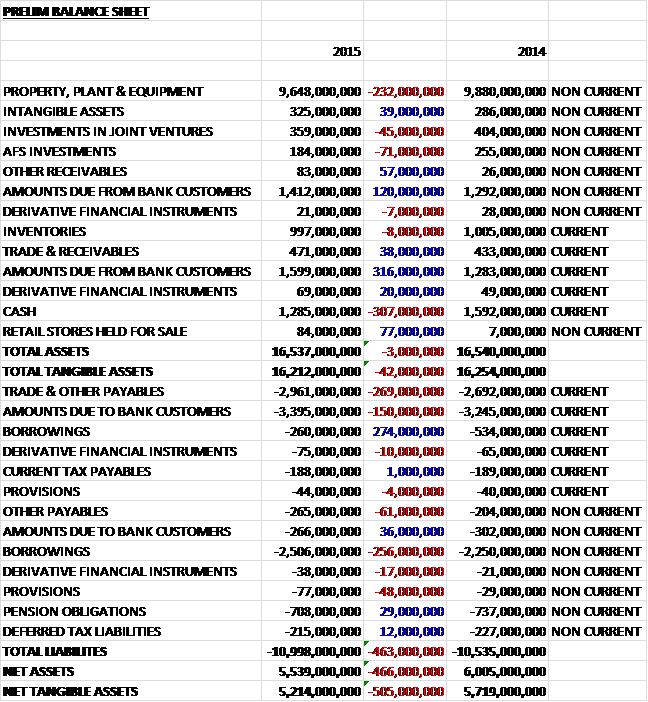

When compared to the end point of last year, total assets fell by just £3M as a £307M decline in cash, and a £232M fall in property, plant & equipment was mostly offset by a £436M increase in the amounts due from bank customers and the £77M increase in the value of retail stores held for sale. Liabilities increased during the year, driven by a £269M growth in current payables, a £114M increase in amounts due to bank customers and a £61M increase in non-current payables was partially offset by a £29M fall in pension obligations to give a net tangible asset level of £5.214BN, a £505M collapse when compared to 2014.

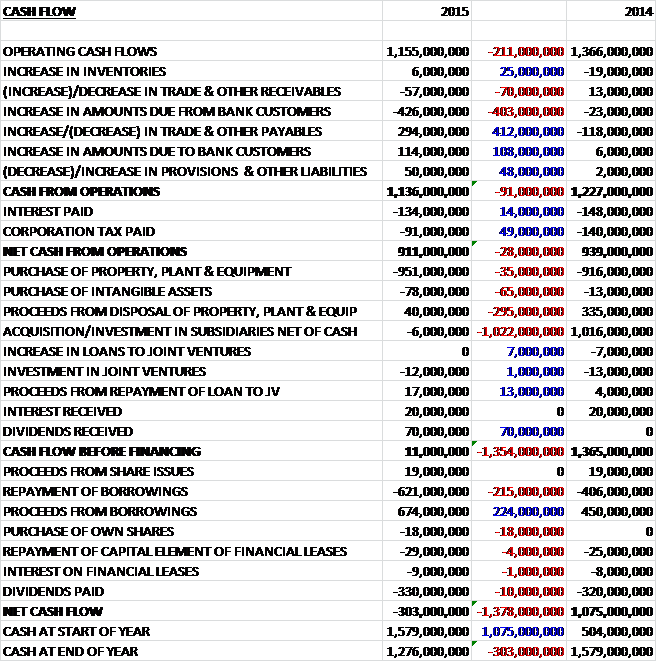

Before movements in working capital, cash profits fell by £211M to £1.155BN. After an increase in the amounts due from bank customers was offset by an increase in payables and a hike in the amount due to bank customers, the net cash from operations of £911M was some £28M lower than in 2014. This cash does not cover the capital expenditure but when £40M of proceeds from the sale of assets, £70M of dividends and some proceeds from the joint ventures are taken into account, the cash flow before financing stood at £11M. The payment of dividends was then the main cause of the £303M cash outflow recorded during the year, although the cash pile of £1.276BN at the end of the period seems to give decent coverage.

There is no doubt that this has been a difficult year for Sainsbury, underlying profit before tax fell by nearly 15% to £681M and market share declined by 25 basis points to 16.5% with increased competition from discounters. Underlying operating profit at the retail operation stood at £604M, a decline of £154M when compared to last year as like for like sales fell by nearly 2% due to continued challenging market conditions and retail price deflation and the group invested in the customer offer in order to remain price competitive, partially offset by £140M worth of cost savings. The underlying operating margin declined by 58 basis points to a rather thin 3.07%.

Underlying operating profit at the financial services operation was £62M, an increase of £38M when compared to 2014, mainly due to lower market savings rates which resulted in a reduction in interest payable, along with increased lending and lower bad debt levels. In January 2014, the group took full ownership of Sainsbury’s Bank and they are part way through the transition to become a standalone bank. During the year there was a 13% increase in the number of Sainsbury credit cards being used in store and whilst reduced advertising activity has resulted in overall customer awareness of the bank declining slightly, the number of active accounts has increased by 6% to 1.7M. The loans business had a good year with a 13% year on year increase in sales volumes and the travel money business saw sales growth of 24% and they opened their 168th travel money outlet.

Due to increased competition, car and home insurance sales volumes declined during the year but pet insurance grew by 64%. The ATM estate grew by nearly 7% and the bank’s website visitors grew by over 12% to over two million visits per month. Unfortunately it seems that the costs of transferring the bank are higher than initially expected with costs expected to rise by between £80M and £120M going forward, taking overall spend to between £340M and £380M. The migration of savings customers is hoped to occur in 2015 but this cost overrun is considerable and disappointing. The tier 1 capital ratio fell from 13.6% to 12.7% reflecting the increased customer lending and one-off costs from the bank transition.

Underlying operating profit in property investments stood at £15M, a decline of £1M year on year. Despite the £900M decline in the property valuation, the group is looking to maximise the value of the property assets by working with partners to deliver new residential, leisure and commercial opportunities whilst adding trading space to the estate. They are delivering 1,500 new homes across London, partly through the £500M project with Barratt at Nine Elms. This project will deliver 737 new homes, a new Sainsbury store, restaurants and office space. Plans have also been developed for a replacement store at Whitechapel Square alongside 600 new homes and improved public space surrounding the station. These mixed use development schemes are expected to deliver profits of around £200M over the next two years, which sounds like a good return.

The problems facing grocery retailers have been well documented with a structural shift in the way people do their shopping with smaller, more frequent convenience shops combined with larger online orders which is continuing to cause volumes in large, traditional supermarkets to decline. Around a quarter of the group’s stores will have some under-utilised space over the next five year (about 6% of the total space). Half of this will be used to expand the clothing and general merchandise offer with the remaining space being used for concession partners such as Argos, who will open concessions in ten supermarkets this year; and Timson, who will bring their products to more supermarkets. GP and dental surgeries are another option and have proven popular so far.

One area that Sainsbury continues to outperform its rivals is that of perceived quality and provenance. So far, some 3,000 own brand products have apparently been improved and the group was named drinks and seafood retailer of the year at the industry awards and in-store bakery retailer of the year at the bakery retail awards. The own brand offering accounts for just under half of all food sales but it underwent a small decline year on year despite the premium own brand increasing sales by nearly 5%. The group have invested some £50M into lower prices of products and expect to invest another £150M during this year.

The convenience stores have done well during the year, plugging into the new trends detailed above and sales were up 16%. The group are targeting this as an area for growth and plan to add between one and two new convenience stores a week to the portfolio after opening 98 during the last year. The online offering is also being expanded, with better delivery slots and a “dark store” for online orders only on track to be opened in Bromley by Bow in 2016. Although the rate of online growth has slowed due to increased competitor aggressiveness, there was still a 7% increase during the year. The Netto trial continues with five stores now opened and a total of 15 expected by 2016.

One area that management has earmarked for growth is non-food. Clothing and general merchandise grew sales by over 9% and the growth strategy focuses on increasing non-food presence in stores. The trial of selling clothing online has been extended to a number of regions across the country, including London and the South East with a full roll-out of the offer expected in 2015.

There have been a number of one-off charges incurred this year. The store pipeline was reassessed in order to determine whether they have the potential to make decent returns in the new grocery environment which resulted in the decision that some sites will no longer be developed. As a result, a charge of £287M was recognised that included £256M of property write-downs, a £1M impairment of goodwill and £30M of onerous contract provisions. In addition, a £341M charge was recognised with respect to unprofitable stores that are currently trading. This included £284M of property write-downs, £7M intangible asset impairments and onerous lease provisions of £50M. Additionally there was restructuring costs of £15M, costs of £53M to transition the bank to a new platform and £17M in compensation made to employees transitioning to the defined contribution pension scheme after the closure of the defined benefit scheme to future accrual.

The group is taking some action to try and shore up the balance sheet. So far some £140M of operating costs savings have been delivered with a total of £500M expected over the next three years. Core capital expenditure this year was £947M but the group are reducing this to between £500M and £550M in each of the next three years, concentrating on the convenience stores. As a result of operational efficiencies, retail working capital has been improved by more than £300M and the dividend policy is being set making sure there is cover at two times underlying earnings. These actions have been counteracted by a £900M decline in the value of the group’s property due to a reduction in market rental values. The pension scheme continues to be a small drag on earnings with contributions of £49M per year until 2020 agreed at the last valuation, the next one of which is due this year.

Going forward, the group expects like for like retail sales to be negative again next year, driven by continued challenging conditions and food price deflation and contribution from new space is expected to be slightly lower than this year. Cost inflation is expected to be between 2% and 3% with efficiency savings of about £200M. The bank is expected to deliver mid-single digit year on year growth in underling operating profit and capital injections to the bank next year are expected to be about £80M. The share of profit from the property joint ventures is expected to be slightly lower next year and losses on the Netto, Mobile and I2C start-ups are expected to remain around £9M.

At the current share price the underlying P/E ratio stands at 10.5 but this increases to 12.2 on next year’s consensus forecast which seems about right to me. After a 24% cut in the dividend, the shares currently yield 5% but this falls to 4.1% on next year’s forecast as the group maintains the two-times underlying profit dividend cover. Net debt stands at £2.3BN which compares favourably with the £2.4BN recorded last year (including bank debt) and undrawn borrowing facilities of £1BN. Next year, net debt is expected to show another small improvement due to improved working capital controls.

There is now doubt that this has been a difficult year for the group. They recorded an overall loss with a reduction in underlying profits and there was a fall in net assets as payables increased and the property impairments took their toll on the balance sheet. The cash flow seems a little better with operating cash flow marginally down as the group kept tight control on working capital and free cash flow was broadly neutral, although the dividend payment pushed the group to a cash outflow. This is not an unusual state of affairs for Sainsbury though and there seems to be a decent level of cash available. Trading-wise, market share fell and margins were down as continued fierce competition, along with changing shopping habits affected the group.

The group is looking to stem the lost business from the large supermarkets by focusing on non-food items and concessions which seems a sensible enough strategy, although whether anyone will want to visit an out of town department store that sells groceries is open to debate. The bank seems to be trading well but the increased costs of transferring it to the new platform is a real blow. Going forward, next year sales will probably fall further and the bank will need an £80M capital injection so next year is unlikely to show any improvement so I don’t see this as a good investment at this time.

After recovering from the lows at the end of last year, the share price now seems to be trending generally sideways.

Sainsbury has now released its annual report so there are a few items that have some more detail, starting with the income statement.

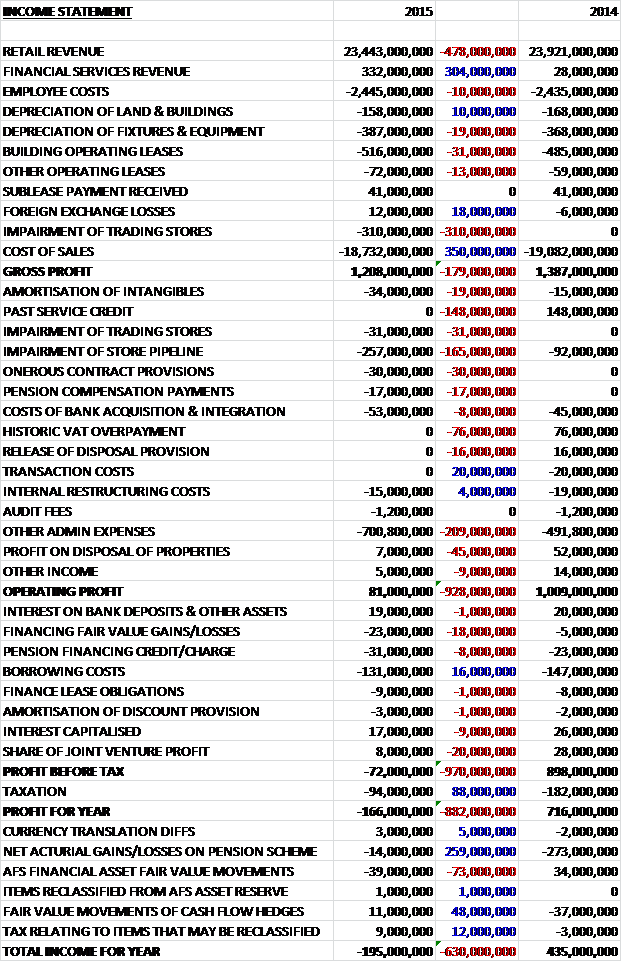

This is a real mess with all the one-off costs. We can see a better split regarding where they sit within admin expenses and cost of sales which shows that underlying cost sales actually fell year on year with the underlying admin expenses increasing considerably. There don’t really seem to be many other new items of note, although the increase in provisions seen on the balance sheet seems to be due to onerous leases relating to the closure/cancellation of stores.

The balance sheet always has more detail in the annual report – I don’t know why different receivables/payables can’t be listed in the prelim results as I feel this split is quite important. Gere we can see that the growth in intangible assets is due to the investment in software and the increase in current receivables is due to prepayments and accrued income, along with “other receivables” rather than trade receivables. As far as current payables are concerned, the increase is due to a hike in trade payables, and accruals partially offset by a fall in “other payables”.

I find it interesting to look at KPIs as this gives an idea of what management is prioritising and in Sainsbury’s case it makes an interesting read. They benchmark their price and quality perception against Asda, Tesco and Morrison’s and although their quality perception is highest amongst those four, their price perception is lowest. Also, they measure product availability at their stores and whilst the supermarket gained a “gold” rating, the rating at the convenience stores was just “bronze” which suggests this is an area that needs prioritising. Sales growth in another area being prioritised and whilst clothing and financial services both grew faster than last year, grocery and general merchandise did not. Other items include EPS, operational cash flow ROCE and gearing, all of which deteriorated during the year whilst cost savings improved.

Another area that only becomes apparent once the annual report is published are the huge operating leases that the group has for its stores. These are debts that are not included on the balance sheet and really add a different slant on the balance sheet strength. As we have seen, the group has £5.5BN of net assets but its operating lease commitments are £9.796BN and they increased by £769M year on year which could be cause for concern with some £585M of operating leases due to be paid over the coming year. The group also has some £164M of future capital expenditure commitments and £13M for intangible asset purchases.

Overall then, a little more information but the core premise still remains – I find it hard to justify an investment here with market conditions as they are and the large amount of operating leases just confirms this as far as I’m concerned.

Sainsbury has now released a trading update covering Q1 2016. Excluding fuel, like for like sales fell by 2.1% which was worse than the 1.9% average over last year. Trading conditions are still being impacted by strong levels of food deflation and highly competitive pricing which have led to the falls seen despite a growth in both transactions and volumes as customers benefit from investments made in price and quality. The board are apparently encouraged by some of the early trends that are being seen in their key trading and operational metrics.

During the quarter the group introduced new products in several categories, including areas such as produce and speciality bread and have improved their seasonal fresh offer in time for summer. They are on track to deliver all of their planned quality improvements. The bank saw travel money grow strongly at over 40% and was named best card provider at the Moneyfacts awards. Clothing sales grew by 5% and the clothing online offer proved popular enough to roll it out nationwide over the summer. The group now has 20 grocery click and collect sites and remains on track to have 100 by the end of the calendar year. Groceries online had a record week during the quarter with 256,000 orders and it has increased the number of delivery slots available. Three Argos digital stores were opened during the period with ten on course to be opened by the end of H1, and the convenience business remains in double digit growth after ten more convenience stores were opened.

Overall then the headline figures look pretty disappointing but it is good to be reminded about some of the initiatives being sought by management and the fact that volumes are up has got to be encouraging. I still feel that it is too soon to buy back in here though.

On the 11th June the group announced that CEO Mike Coupe was acquitted by an Egyptian court of all charges brought against him as a representative of the company which hopefully brings an end to a rather bizarre story.

On the 29th July the group announced that Celesio, the owner of Lloyds Pharmacy will acquire Sainsbury’s pharmacy business for £125M. In addition, Sainsbury will receive commercial annual rent payments from Lloyds for each location. In all they have agreed to acquire 281 pharmacies including 277 in store and four located in hospitals.

On the 30th September the group released their Q2 trading update. I suppose the headline figure is that like for like sales (excluding fuel) declined by 1.1% in the quarter which compared favourably with the 2.1% fall in Q1. Both volumes and transactions grew as the decline in average basked spend in supermarkets continued to stabilise. Whilst he market is clearly still challenging, with food deflation impacting many categories, progress is being made.

Taste the Difference volumes grew by over 4% over the quarter with some improvements being made to the taste and texture of the juice ranges and improved ripeness and quality of the avocados. Promotional activity was reduced in favour of lower regular prices and the accuracy of the demand forecasting is improving which is driving better availability and lower than expected levels of waste. The group did announce a 4% pay rise for its staff which is the highest annual pay increase for over a decade – no doubt this is being done for a) propaganda reasons and b) to mitigate the drastic effect the new minimum wage directives will have when they are introduced.

Some 27 convenience stores were opened during the quarter so they are still expanding in this area. Online grocery orders increased by over 15% and they increased the number of click and collect sites to 52. They also launched the Tu clothing website nationwide and the first six weeks of trading have significantly exceeded their expectations with the majority of customers choosing to collect their orders in store. Clothing as a whole grew by nearly 13% with the back to school range proving particularly popular. Sainsbury Bank opened its 200th travel money bureau during the quarter and saw its best ever month for travel money in July with a 35% year on year increase in transaction volumes.

Year to date the group have traded reasonably well with both sales and cost savings ahead of expectations. Should current market trends continue, the board expect their full year underlying profit before tax to be moderately ahead of consensus forecasts.

This is an interesting update, things do seem to be improving and at a faster pace than expected. Despite volume increases, sales value do continue to fall on a like for like basis but this is slowing. Sainsbury just got interesting again in my view.