Sanderson develops and supplies IT software and services which includes market-focused solutions to the multi-channel retail and manufacturing sectors, they currently have 460 customers and they are listed on the AIM exchange and have now released their final results for the year ended 2014.

Revenues for initial license fees are recognised on the provision of software to the customer. Revenue from the provision of professional services including support, maintenance, training and consultancy services is recognised as the services are performed. Hardware sales are recognised on delivery and annual licence, maintenance and support revenues are recognised evenly over the period to which they relate. When amounts are invoiced in advance the unearned element remains in deferred income until recognition is appropriate. Having recently looked at Utilitywise which recognises revenues on multi-year contracts at the start of each project, this revenue recognition is clearly the more sensible way of doing it. It is also good to see that the bulk of the development costs are expensed rather than capitalised, although some £600K was still capitalised during the year.

In manufacturing the group’s ERP software and cloud based solutions support many sectors such as discrete manufacturing, food and drink processing, print and distribution. The range of green IT, factory and warehouse automation solutions to improve efficiency and manufacturing and provide cost saving benefits to customers which include Associated British Foods and Michelmersh Bricks. In multi-channel retail, the group supplies software and services to retail, mail order catalogue, fulfilment, wholesale and online businesses. The group provides integrated e-commerce systems which underpin online operations, in-store technology, and is a major provider of IT solutions to the wholesale and cash and carry industries. The driver for customers to adopt these solutions is to increase efficiency, making cost savings and delivering business growth.

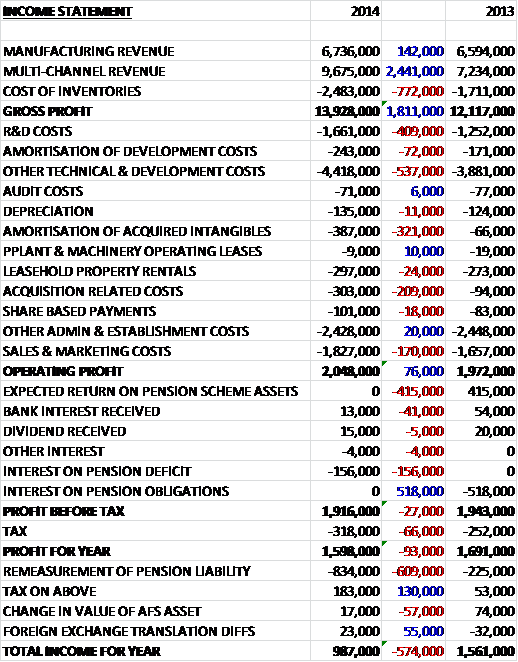

Overall revenue increased year on year, driven by a £2.4M growth in multi-channel retail revenue. Cost of sales also increased to give a gross profit some £1.8M higher than in 2013. We then see that R&D costs increases by £409K and other technical and development costs were up £537K. The group also saw a £321K increase in amortisation of acquired intangibles, a £209K growth in acquisition related costs which were fully expensed during the year and a £170K growth in sales and marketing costs to give an operating profit just £76K above that of 2013. We then see the lack of a £415K return on pension scheme assets that occurred last year being offset by the lack of the interest on pension obligations. After an increase in tax, total profit for the year came in some £93K below that of last year at £1.6M.

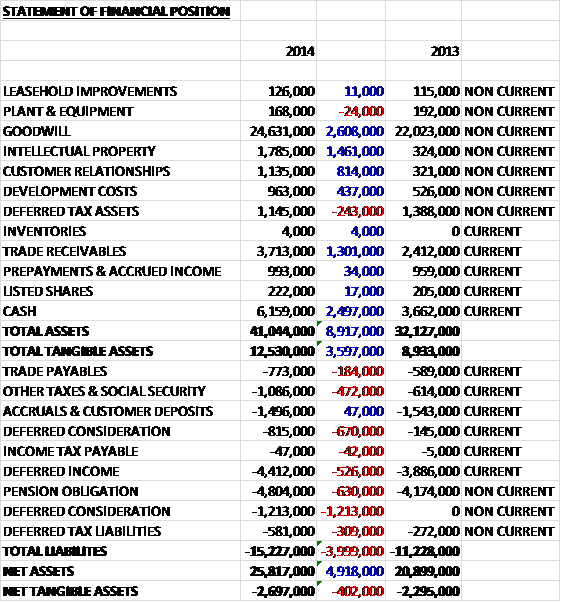

When compared to the end point of last year, total assets increased by £8.9M driven by a £2.6M increase in goodwill, a £2.5M growth in cash, a £1.5M increase in intellectual property and a £1.3M growth in trade receivables. Liabilities also increased during the year due to a £1.9M increase in deferred consideration and a £630K increase in the pension obligation. The end result is a £402K reduction in net tangible assets which stand at a negative £2.7M. There was also £3.8M worth of operating leases outstanding, £253K of which is due within the year.

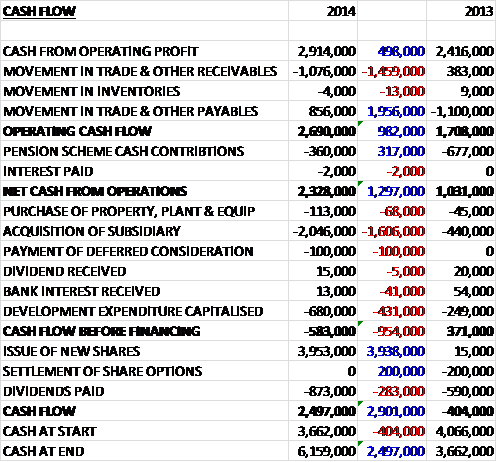

Before movements in working capital, cash profit increased by £498K to £2.9M. We then see an increase in payables more than offset by a growth in receivables before the contributions to the pension scheme nearly halved to give a net cash from operations of £2.3M, an increase of £1.3M year on year. This cash easily paid for the capital expenditure with £680K going on development costs and £113K on fixed assets but did not cover the £2.1M of acquisitions. In order to pay for these and cover the dividends, the group then issued new shares at a value of just under £4M to leave a cash flow for the year of £2.5M and a cash level of £6.2M at the year end.

Operating profit at the Manufacturing business was £877K, just £29K above that of last year. The market continued to experience slow trading but a recently launched product, Unity Express, aimed at smaller manufacturing businesses has a number of good and promising prospects in the sales pipeline. The growth in the division was driven by the food and drink processing sector which now accounts for half of all the division’s revenues and continues to provide opportunities due to the need for traceability through the supply chain combined with the drive to reduce operating costs. Seven new customers were gained during the year compared to nine last year and the order book at the year-end fell from £1.2M to £926K.

The operating profit at the Multi-channel retail business was £1.2M, a £46K increase year on year. A continued high level of activity has been experienced from the provision of ecommerce and mobile commerce solutions with an average growth rate over 10%. The growth in the ecommerce and wholesale distribution business was partially offset by a fall in the traditional mail order business, however. Priam, which was acquired last year, was restructured and fully integrated into the group and whilst its profit contribution was minimal in the year, it is expected to make an improved contribution next year. Ten new customers were gained in the year compared to five last year. It seems that the order book in the ecommerce business took the group by surprise and this apparently held back profitability during the year but now offers a good opportunity to boost profitability in the coming year.

The value of the order book at the year end stood at £2.4M, an increase from the £1.9M recorded at the end of last year. During the year 17 new customers were gained (14 last year) at an average initial contract value of £116K (£119K) with the total value of new orders growing to just under two million pounds.

I always like a good case study and Sanderson has provided a few of those. Freddy Hirsch is an ingredients manufacturing organisation that has grown to become the largest food ingredients manufacturer in Africa. The company has been a Sanderson customer for 14 years and is a major user of all available modules in their food ERP system including factory automation for scheduling and control of recipe weighing and multiple dispensing systems. The group’s manufacturing system allows Freddy Hirsch to operate a common IT platform across its business with products and prices managed by head office and downloaded to the relevant country.

Preston Beer is a £5M, ten employee business. It supplies an extensive range of beers, sprits, soft drinks and wines to restaurants, hotels and pubs in the North of England. It has transformed its operations with the Sanderson delivered wholesale solution with their investment paid back over three times in under a year. Robust pricing control, real-time stock visibility and management data are all provided with accurate stock control achieving a saving of £5K per month. The group also supplies Aspinal who sell fine quality leather goods. The company has benefited from rapid sales order processing, accurate stock information across all channels and greater warehouse efficiency.

There is an interesting array of KPIs and the group’s performance against them was mixed. Operating margin and order intake both improved but revenue per employee, debtors over 60 days (12.2%) and dividend cover (2.4) all deteriorated year on year. The increase in the debtor days was quite considerable and above the 10% target. This was being put down to delays encountered in projects involving the integration of third party products and activity levels in the approach to the year-end. The economic environment also increased the number of customers extending payment beyond agreed credit terms which has got to be a bit of a concerning development.

It can be seen that the group operates a pension scheme and although relatively modest, the liability is affecting the net asset level. It is closed to future accrual and had its last actuarial valuation in 2011 so another one is due soon so this is a potential risk going forward. The bulk of the group’s revenues are earned in the UK so there is no foreign exchange risk. The main risk though, is probably a downturn in the economic environment and the subsequent reduction in company’s IT spend that would result from that.

It should be noted that the largest shareholder is Christopher Winn who owns some 22% of the total share capital. Mr Winn led a management buy-out of the company before it floated on the AIM exchange. He is also Chairman of the company and by far the best paid director. In fact, his pay could be considered rather generous so on one hand, we have to be careful that he doesn’t get too greedy and keep awarding himself increasingly excessive pay awards but on the other hand it can be good to have someone with such a vested interest running the company. There appears to be no CEO at Sanderson.

During the year the group acquired One Iota ltd which is a business that provides cloud-based multi-channel solutions via new mobile, tablet and in-store devices. The maximum consideration could be up to £5.4M which generates goodwill of £2.6M. The acquisition was satisfied with a cash consideration of £2.4M paid on acquisition and a further £750K satisfied by the issue of new shares. Deferred consideration of £300K will be paid over the three years following the acquisition and an additional £2M in deferred consideration could become payable subject to various performance targets to the year ending 2016. Last year One Iota produced revenues of £665K with a profit before tax of £195K and during the period it contributed £160K to the group’s profits. In my view, on the surface, this looks like a good acquisition for the group being good value and offering an opportunity to expand into the mobile retail solutions market.

In order to pay for the acquisition the group raised some cash by placing over six million new shares at 55p each which is a decent way of raising more cash but could be a sign that lenders were not willing to lend money due to the weakness of the balance sheet. Going forward, business sentiment at small and medium sized businesses has continued to show some improvement but customers remain cautious in their outlook. The improved order book provides the board with a reasonable level of confidence that the group will make further progress in the next year.

At the current share price the shares trade on a PE ratio of 22.2 which doesn’t look to cheap but this does fall to a better looking 14.1 on next year’s consensus forecast. After a 20% increase in the total dividend year on year, the shares currently yield a useful 2.7%, increasing to 2.9% on next year’s forecast. The group has a net cash position of £6.2M at the year-end compared to £3.7M at the end of last year.

Overall then, this was a mixed performance this year. Profits fell year on year and although it could be argued that the cause of this was acquisition related costs, given the frequency of acquisitions, it looks to me that these are underlying costs. Net tangible assets fell and the balance sheet looks weak with a negative net tangible asset level, although IT companies don’t seem to have very good balance sheets as a rule. The cash flow does look decent though, and the increasing operating cash flow threw off some free cash, although not enough to cover the acquisition. Speaking of which, the One Iota business looks to be a good purchase to me and it is already contributing to profits which should improve after the acquisition related costs work their way through.

The manufacturing business seems to be struggling with a reduction in the number of new customers and a lower order book at the year-end but this is offset by an improvement at the multi-channel retail business, boosted by the acquisition. Indeed, were it not for the acquisitions then organic growth across both businesses would have been fairly modest. The products do seem to offer some tangible benefits to customers, though, and there seem to be a number of long term clients on the books so there is clearly a good business here but whether that can trickle down to the bottom line is a little less clear. I will keep watch at this company for the moment.