Sanderson has now released its interim results for the year ending 2015.

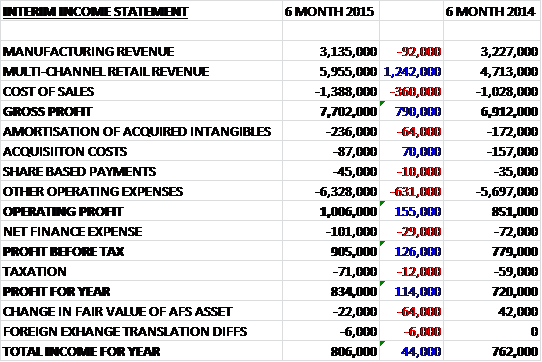

Multi-channel retail revenue is becoming a more important part of the business with a £1.2M increase year on year compared to a £92K decline in manufacturing revenue. Cost of sales also increased to give a gross profit some £790K higher than in the first half of 2014. We then see an increase in amortisation of acquired intangibles offset by a fall in acquisition costs but other operating expenses increased by £631K year on year. When combined with a £29K increase in finance expense and a £12K increase in taxation, the profit for the half year stood at £834K, an increase of £114K when compared to the first half of last year.

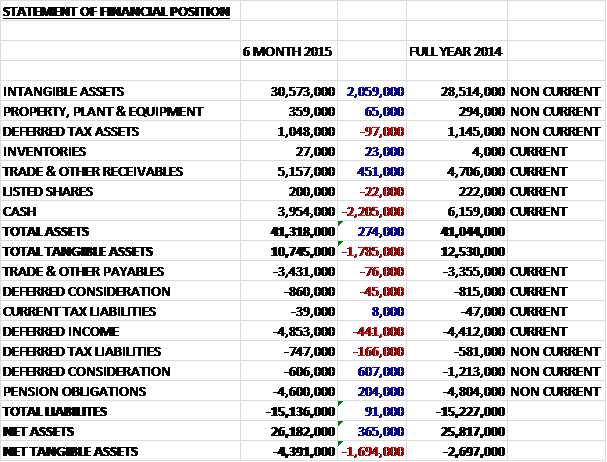

When compared to the end point of last year, total assets increase by £274K to £41.3M driven by a £2.1M increase in intangible assets and a £451K growth in receivables, partially offset by a £2.2M fall in cash. Total liabilities fell during the year as a £441K increase in deferred income and a £166K growth in deferred tax liabilities were more than offset by a £562K decline in deferred consideration and a £204K fall in pension obligations. The end result is a further £1.7M deterioration in net tangible assets to a negative £4.4M.

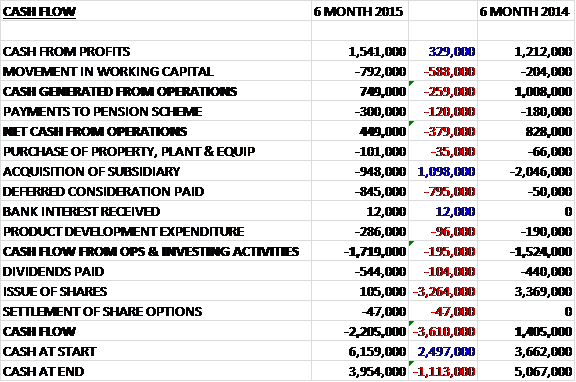

Before movements in working capital, cash profits increased by £329K to £1.5M but this was reversed by a £792K working capital outflow as a number of sales ledger balances slipped beyond the period end with a total of £435K being receivable in the first week of April, and a £300K payment to the pension scheme so that net cash from operations was just £449K, a decline of £379K year on year. Although this just about covered the development costs and purchase of fixed assets, the group also spent £948K on another acquisition and a further £845K on deferred consideration to give a cash outflow of £1.7M before financing. The small issue of shares did little to stem the cash outflows as the group spent £544K on dividends to give a cash outflow for the half year of £2.2M and a cash level of just under four million pounds at the period end.

The order book at the period end was £2.8M compared to £2.5m at this point of last year and 13 new customers were gained, up from 12 last year.

Operating profit at the Manufacturing business was £334K, which was broadly flat year on year with a decline of just £5K. The general manufacturing business improved its trading performance compared with the first half of last year which is expected to continue into the second half of the year. This performance was offset by the food and drink business which experienced some delays in the receipt of expected sales orders. Eight new customers were gained during the period including Simtom Food Products, Summit Chairs, Wine Bottling Solutions and NutriFresh which compared well with the five new customers gained during the first half of last year. There were also some large projects with existing customers including Magnadata, Cook Trading, Food Partners and Freddy Hirsch.

The group has had some success with its entry level Unity ERP product which is aimed at smaller and emerging businesses and over the coming months they are expecting to further develop the software and to launch new products, including further cloud based solutions. Recurring revenue represents over 61% of total divisional sales and the order book stands at £1M, a decline of £240K year on year but a strong sales prospect list should ensure that the division achieves an improved trading result for the full year.

Operating profit at the Multi-Channel Retail business was £672K, an increase of £160K when compared to the first half of last year. Mobile enablement and deployment continues to be a key driver in this sector with increasing levels of business activity. The wholesale distribution and cash and carry market has been slower during the period, however, but prospects for the second half of the year are good, driven by the release of the latest enhanced version of software. The acquired Proteus has made a steady start to the year and helped further expand the group’s presence in the areas of warehousing, logistics and supply chain.

Five new customers were gained during the period including Anzac Wines and Spirits, Lavitta, Quba & Co and Matthew Algie which compared unfavourably with the seven customers acquired in the first half of last year. The division also managed to gain a number of large orders from existing customers including JD Sports, Kingstown Associates and Superdry. The period end order book was strong at £1.8M (£1.2M) and with good sales prospects, the division is well placed to achieve its increased trading targets for the full year.

In December the group acquired Proteus Software Ltd for a maximum consideration of £1.9M, generating goodwill of £1.1M. The group has paid £1.4M in cash with up to £500K payable depending on the profitability of the business over the next year. The acquired company provides warehouse management solutions to businesses operating in third party logistics, warehouse management and supply chain distribution markets. Since acquisition, the business contributed £47K to operating profits before amortisation of acquired intangibles and acquisition related costs. I think it is getting to the point where I would like to see Sanderson concentrate on organic growth but this looks to be another decent value acquisition.

I am pleased to see that the group finally has a CEO, Ian Newcombe has been appointed having already made a contribution to the group’s strategy and driven the development of the multi-channel business. The group have also appointed David Gutteridge as a non-executive director who was Chairman of Tinglobal until he led a successful trade sale to Singapore listed Declout. It seems he has been employed previously at Sanderson.

I notice that the Chairman has stated in the interim results that the company has a strong balance sheet. I have found that this type of statement is a bit of a red flag and so it seems to be the case here too. It doesn’t look that strong to me, stuffed with goodwill and a negative net tangible asset level. The pension deficit is an unhelpful liability too and there are some £3.8M worth of operating leases off the balance sheet.

Going forward, particular emphasis will be placed on further developing the range of solutions for mobile and ecommerce businesses, for the food and drinks processing sector and for entry level systems in the manufacturing division. The general economic environment continued to show signs of improvement but sales cycles remain protracted. The board is apparently cautious but the decent order book along with a long list of sales prospects provides them with a good level of confidence that the group will continue to make further progress and deliver results in line with market expectations for the full year.

Net cash at the period end stood at just under £4M (£3.95M) compared to £5.1M at the same point of last year. The interim dividend has increased by 12.5% to give a rolling dividend yield of 2.8%.

Overall then, this seems to have been a fairly good start to the year with profits increasing and the order book in a better state than at the same period last year. The group is still consuming more cash than it generates though, due to its continued expansion through acquisitions. Also, the balance sheet deteriorated somewhat during the period and net tangible assets remain negative. The retail business looks good with increased profits and order book despite the slowdown in wholesale orders but the manufacturing business is a bit more mixed with flat profits and a fall in the order book due to a slowdown in the food manufacturing market. This is a tricky one, on the one hand I do like the company and its products but I have nagging doubts about the cash burn and the negative tangible asset base. I may look to buy on any improved trading announcements.

Well this is a bit of a mess! The share price seems to jump around all over the place but it has definitely been range bound over the past year.

It has been announced that on the 15th July, non-executive director David Gutteridge acquired 45,000 shares at a value of £29.7K. Following the transaction he owns 545,000 shares in the company representing about 1% of the total. This is a nice sign of confidence.

On the 27th October the group released a trading update covering the year as a whole with trading in line with market expectations. Group revenue grew from £16.4M to over £19M and adjusted operating profit increased from £2.8M to £3.3M.

The group continued to invest in its product and service offerings which are designed to provide customers with tangible business benefits often visible within a short time. A particular focus is in the multi-channel retail business to further enable the adoption and application of digital and mobile technologies into the retail market. The group’s mobile commerce business focused on delivering cloud based solutions accessed via mobile, tablet and in-store devices achieved revenue growth of over 75%. It is expected that it will continue to achieve significant growth as retailers seek to adapt technology in order to transform the shopping experience for their connected customers.

Within the manufacturing division, the part of the business focused on supplying customers operating in the food and drink processing market experienced slower trading conditions with some project and order delays but a large new customer order has been received since the year-end and trading prospects in the new year are much improved.

The group acquired Proteus Software, a provider of specialist warehouse management solutions in December and the business has made a positive contribution in its first year as part of Sanderson. Notwithstanding the ongoing investment in product development and acquisitions which have been funded through the cash generated, there is a cash balance in excess of £4.4M at the year-end compared to £4.2M at the half year point.

The overall economic environment appears mixed and sales cycles continue to be protracted. The deployment and use of mobile technologies is continuing to develop with market demand accelerating. In the coming year, management expects to focus further efforts on delivering growth across the group’s businesses but especially from the newly emerging digital retail market and further acquisitions will be considered.

At this early stage of the new year, the board are condiment they will make further progress and deliver trading results at least in line with market expectations for 2016.

This all sounds rather good to me – “at least” could be considered a guidance slightly upwards from current expectations.