32Red is involved in the provision of interactive betting and gaming operations over the internet. It is domiciled in Gibraltar and is listed on the AIM exchange. The board own a considerable amount of the company with the chairman, CEO and non-exec John Hodgson owning 45.2% between them. It has now released its final results for the year ending 2014.

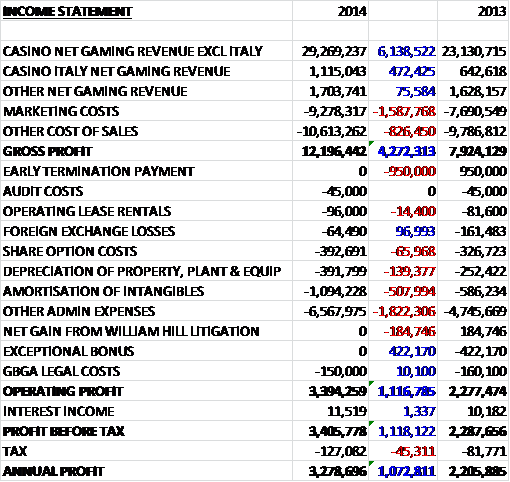

Overall revenues increased when compared to last year with Italian casino revenues up £472K, other casino revenues up £6.1m and other net gaming revenue increasing by £76K. Cost of sales also increased, driven by a growth in marketing costs, to give a gross profit some £4.3M ahead of last year. We then see a lack of the early termination payment from Swansea City (£950K) and the gain from the William Hill litigation (£185K) that occurred last year, offset by the non-recurring exceptional bonus of £422K in 2013. We also see amortisation increasing by £508K and other underlying admin expenses up £1.8M to give an operating profit some £1.1M higher than in 2013. The GBGA legal costs seem to be ongoing and are incurred in respect of industry lobbying and legal advice connected to the UK government’s proposed point of consumption tax regulation. After a slightly higher tax bill, the profit for the year stood at £3.3M, an increase of £1.1M year on year.

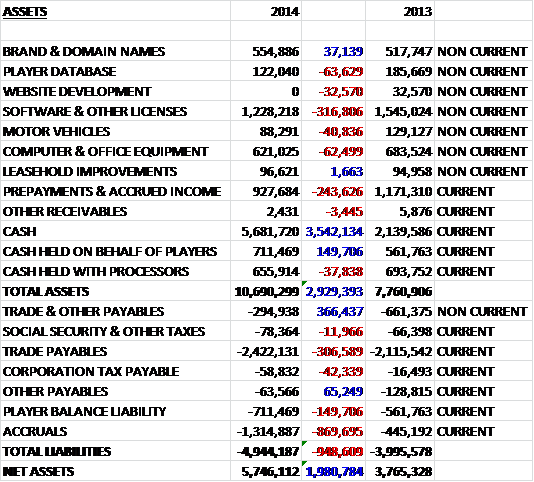

When compared to the end point of last year, total assets increased by £2.9M driven by a £3.5M increase in cash, partially offset by a £317K fall in the value of software licenses and a £244K decline in prepayments and accrued income. Total liabilities also increased during the year as an £870K growth in accruals and a £307K increase in current trade payables was partially offset by a £366K fall in non-current payables. The end result is a £2M increase in net assets to £5.7M. There is also some £480K worth of operating leases off the balance sheet but this is not really a material amount.

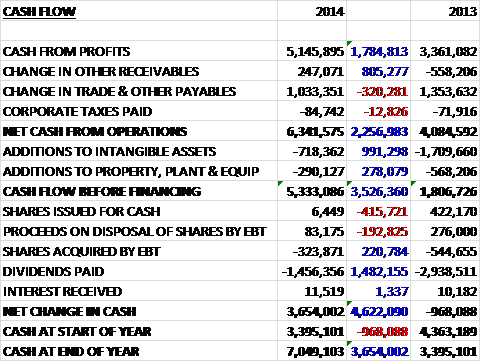

Before movements in working capital, cash profits increased by £1.8M to £5.1M which was further improved by an increase in payables to give a net cash from operations of £6.3M, an increase of £2.3M year on year. The group spent £718K on intangible assets and £290K on property, plant and equipment and the free cash flow was £5.3M. This was more than enough to pay for the £1.5M in dividends to give a cash inflow for the year of £3.4M and a cash level at the year-end of £7M.

Gross profit before marketing costs in the Italian casino business was £795K, an increase of £348K year on year and a total of 5,011 new players were recruited to bring the number of active players up to 8,628. This performance is despite the company’s decision to limit its marketing investment in Italy during the year, ahead of expected positive changes in the regulated market from the end of 2014. The group is embarking on a new series of TV ads in the country from January 2015

Gross profit before marketing costs in the other casino businesses was £19.7M, an increase of £5.6M when compared to last year. During the year new players increased from 38,033 to 44,385 which is a direct reflection of the increased marketing investment with a total of 31,241 TV adverts being viewed by 5.4M UK males. While TV advertising continues to be largest marketing expense, awareness of the brand is also increased by the continued sponsorship of UK horseracing as one of the four main financial supporters of the All Weather Horseracing Championships. In addition, the group has also signed a three year sponsorship deal with Rangers football club and is half way through its three year license to operate “I’m a Celebrity Get me out of here” slot machine games. Over half of all new customers are recruited via mobile devices with mobile casino revenues up 89% now accounting for 32% of total casino revenues.

Gross profit before marketing costs in the other products business was £963K, a decline of £150K when compared to 2013 although during the year the group signed an agreement with B2B sportsbook supplier Kambi Sports Solutions to deliver a fully managed sportsbook solution to 32Red. The new sportsbook is fully integrated with the existing microgaming platform enabling customers to transfer fund between casino and sports. This was launched in June 2014 and initial trading results have been encouraging. Poker and Bingo continues to make a steady contribution in highly competitive markets and it is expected that these products will benefit from increased activity levels following an increased investment in marketing.

There only seems to be two KPIs, the NGR increased from £25.4M to £32.1M during the year whilst the number of active casino players increased from 71,266 to 82,155. The board are incentivised to reach certain EPS growth targets and I notice that they are re-calculating 2013 EPS as if UK POCT had been in place throughout the year and to use this as the base EPS against which growth targets are set. Considering the board have stated elsewhere that they see the tax as an opportunity for the group as opposed to a headwind, this doesn’t seem to correlate with this action as far as I can see.

In my view, the group looks to be susceptible to the point of consumption tax which came into play in December, as it currently pays the 10% tax rate of Gibraltar and much of its revenue comes from the UK. The group is also somewhat exposed to foreign exchange risk, although the majority of their transactions are denominated in Sterling, a 15% strengthening of Sterling against the Euro would reduce profits by £115K and a 15% strengthening against the Aussie Dollar would reduce profits by £365K.

During the year the group acquired the UK customer database of Go Wild Casino. They were migrated to the group’s platform by mid-September with initial trading following migration being in line with expectations and the board expects the acquisition to be earnings enhancing in 2015.

Trading in the new year to date has been strong with net gaming revenue in the first two months of the year increasing by 35% year on year. The board believes that the new licensing regime in the UK will have the effect of reducing competition and provide opportunities for acquisitions. The group intends to increase its marketing investment in the new year and with relatively modest levels of market share in the UK, the board believes there are a number of opportunities for the group to expand its reach.

At the current share price the shares trade on a fully valued PE ratio of 18.1 but this falls to a more reasonable 13.3 on next year’s consensus forecast. At the year end the group has a net cash position of £7M compared to £3.4M at this point of last year. At the current share price the shares have a dividend yield of 3.2%, increasing to 3.3% on next year’s estimate which is decent if not exactly spectacular.

Overall then this seems like an excellent set of results, profits are up, net assets increased and operating cash flow was ahead of last year with copious amounts of free cash. The casino business seems to be doing well with the poker and bingo businesses doing less well. The new sportsbook agreement looks interesting and could generate some returns. The forward PE of 13.3 looks about right and the 3.2% dividend yield is nice to have but the big black cloud hanging over the group is the introduction of the UK POCT and being based in Gibraltar and having the UK as its main market makes 32Red susceptible. The group doesn’t appear overly concerned given their comments but the realigning of the board’s bonus targets to take the new tax into account paints a different story to me and I would rather they were just honest about the potential impact of the tax. For this reason, I am staying out until more clarity can be obtained.

On the 14th July the group announced the acquisition of Roxy Palace Casino for a total consideration of £8.4M consisting of £2M in cash, with £1M due on completion, £500K in six months and the remaining £500K by the end of 2016; and the issuance of 10,000,000 new shares. The business has been acquired from Hyperlink Media and Applied Logistics and is expected to be immediately earnings enhancing. Roxy Palace offers more than 500 online casino games including slots, blackjack, video poker and roulette and has a database containing 230,000 registered players. The business reported gross profit of £3.4M and EBITDA of £1.6M last year, although the POC tax will have to be factored in to that. It also uses the same Microgaming platform that 32Red uses so integration should be fairly smooth and the group have stated they will keep the Roxy Palace brand.

Overall this looks like a good acquisition. The price seems fair for a business earning more than £1.5M a year but clearly this will be lower once the UK POC tax is taken into account.

On the 22nd July the group gave an update covering trading in the first half of the year. Overall NGR was up 22% to £18.6M with UK casino up 21% to £17M, Italian casino up 67% to £900K and other NGR up 4% to £700K. At the UK casino, the number of new platers increased by 12% to 26,407 with the casino player yield falling from £400 to £380. In Italy, a total of 4,285 new players were recruited during the period and the company continues to grow market share in this recently regulated market and will look to add additional gaming products later in the year.

Trading momentum has continued since the period end with gross gaming revenue increasing by 35% so far in the second half and trading remains comfortably in line with the board’s full year expectations. All this sounds very good and operationally things are going well with Italy offering an exciting growth market but there is no mention of what profits are actually like and no mention at all of the POC tax so it is very hard to make an informed decision as to whether this is a good investment. In all, I feel it safer to wait until there is a clear view on to how profitability will be affected in the first half of the year and for that we will have to wait until September.

On the 23rd July it was announced that CFO Jonathan Hale sold 100,000 shares at a value of £71.3K. He is still interested in 1,329,458 shares representing 1.59% of the total so he still has a substantial interest.