Shoe Zone is a footwear retailer in the UK and Ireland, it was listed on the AIM exchange in May 2014 but is still majority controlled by the Smith family as brothers Anthony and Charles Smith between them own over 50% of the total share capital, they are also CEO and COO respectively. It has now released its final results for the year ending 2014.

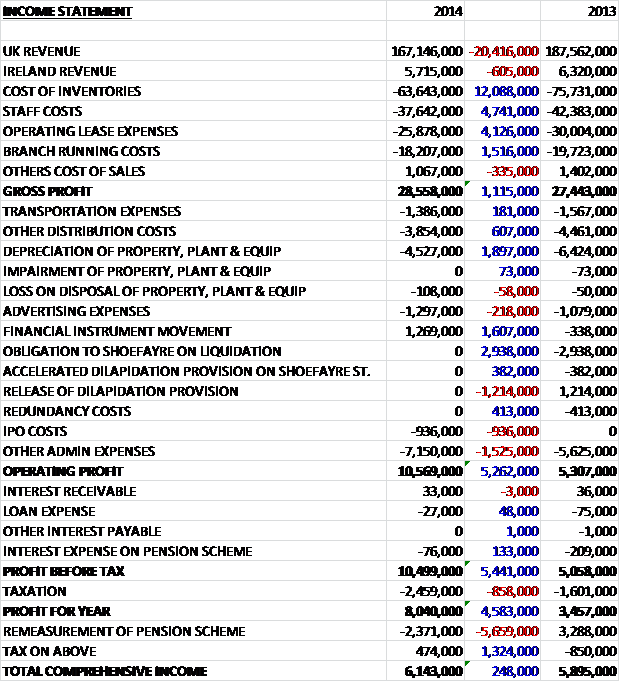

When compared to last year, UK revenues fell by £20.4M and Irish revenues declined by £605K as the group closed several more unprofitable stores, but we also see a decline in cost of sales with cost of inventories down £12.1M, operating lease expenses falling by £4.2M and branch running costs down by £1.5M. I realise that not all staff costs are cost of sales but frankly I didn’t think it was worth trying to estimate where to put them, in any case they are down £4.7M to give a gross profit some £1.1M ahead of that of 2013. We also see distribution costs fall and depreciation costs declining, partially offset by an increase in advertising expenses.

We also see the effect of some non-underlying items as the lack of last year’s £1.2M provision release was more than offset by a positive £1.6M swing in the financial instrument value, a lack of £2.9M obligation to shoefayre on liquidation that occurred last year and the lack of £413K-worth of redundancy costs that happened last year to give an operating profit some £5.3M above that of last year. We then see a small improvement in finance expenses, driven by a £133K decline in pension scheme interest, partially offset by a fall in tax to give a profit for the year of £8M, an increase of £4.6M year on year.

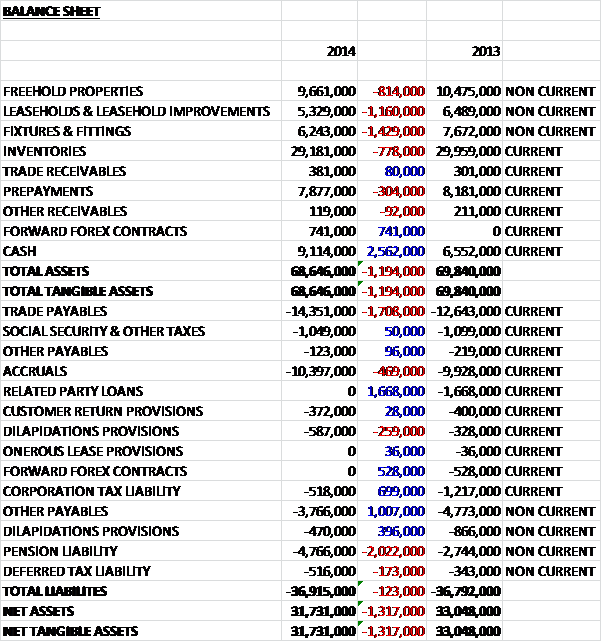

When compared to the end point of last year, total assets fell by £1.2M, driven by a £1.4M decline in fixtures and fittings and a £1.2M fall in leasehold improvements, partially offset by a £2.6M increase in cash. Liabilities increased during the year as a £1.7M decline in related party loans and a £1M fall in other payables was more than offset by a £2M increase in pension liabilities and a £1.7M growth in trade payables. The end result is a £1.3M decline in net assets to £31.7M but it is worth bearing in mind that there are some £103.6M of operating leases off the balance sheet which is substantial but not exceptional in a retail business.

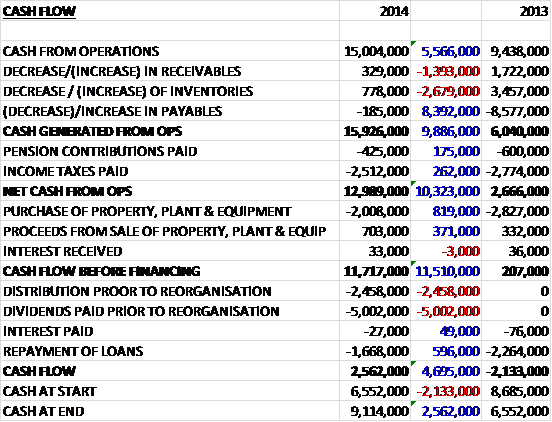

Before movements in working capital cash profits increased by £5.6M to £15M. A fall in inventories and receivables was partially offset by a small fall in payables and after lower pension obligations and tax paid the net cash from operations stood at £13M, an increase of £10.3M year on year. This easily covered the £2M capital expenditure with some £11.7M of free cash before dividends prior to reorganisation and the repayment of loans meant that the cash flow for the year stood at £2.6M to give a cash level of £9.1M at the year-end.

Over the past year the group placed a greater emphasis on their back to school and comfort shoe ranges with the 5-9 age group forecasted to grow by 12% between 2012 and 2017 and the continued growth in the ageing population suggesting improving markets in these areas. As a consequence of this emphasis, they enjoyed their best August in history as the back to school range sold well. In addition, they have increased their focus on men’s footwear and the men’s multi buy offer performed well so has been extended in recent months.

The handbag and shoe care ranges have progressed well after having been introduced in 2013. Handbag sales were up 73% to £2.5M and sales of shoe care products increased by 94% to £1.4M. The ranges have been enhanced for the new-year which is driving further growth in these areas. The group are also looking to introduce their handbag range into the smaller stores after a recent trial was carried out. Shoezone introduced 200 web exclusive products in spring/summer 2014 which far exceeded expectations, accounting for 5% of online sales. As a result of this success, greater volumes have now been purchased for the autumn/winter season. They are now in discussions with their supply partners about further extending their online offer further in 2015.

At the end of the year, the group had 545 stores compared to 570 at the same point of last year with 17 being opened during the year and 45 being refitted at a cost of £1.9M. The group are placing more orders direct with overseas factories with the proportion increasing from 38% last year to 53% this year and this approach apparently gives better margins. The traffic on the website increased by 25% year on year and a fully responsive site will be launched in 2015 following a recent trial that resulted in a 24% increase in mobile conversion rates.

As well as their own website, the group launched on Amazon in November 2013 which made up 8% of all online sales in 2014. Following this, they then launched on eBay in July 2014 which is expected to be at least as profitable as Amazon. In all, online sales grew by 47% but still only represent just over 3% of total sales. The email club grew by 52% during the year which allows the group to continue to develop their email marketing. They have also had some success with business to business transactions which will continue to be developed during the coming year.

The investigations into new stores in Spain and Poland are ongoing but are likely to remain a longer term goal rather than an immediate sales growth opportunity but online international sales have now been commenced with improved international delivery options from the website and the launch into other countries via Amazon.

A look at the KPIs show some that are fairly standard – cash balances increased, along with EPS growth and gross margin. We also see that online participation increased from 2.2% to 3.1% and finally rental percentage of turnover fell from 14.2% to 13.9% reflecting an increase in larger stores and rent negotiations.

There is some exchange rate risk on purchases from major suppliers based in the Far East which is mitigated through using forward foreign currency exchange contracts and it could be worth keeping an eye on the pension schemes – the group operates a number of them and the pension liability increased by £2M to £4.8M, mostly relating to the Shoefayre defined benefit scheme. Contributions of £300K are expected to be made in the coming year.

Going forward, despite the warm start to the winter season, the board believes 2015 will be a year of continued growth for the group. So far this year, six new stores have been opened and terms have been agreed on 10 new stores representing seven relocations and three new locations. The multi-channel offering continues to grow ahead of forecasts and the falling oil price is having a positive impact on the cost of logistics and raw materials. The board are therefore confident that the business will perform in line with market expectations.

At the current share price the shares have a dividend yield of 2.1%, increasing to an impressive looking 5.4% on next year’s consensus forecast. If we discount the IPO costs, the shares are trading on a very cheap looking PE ratio of 9.7 but next year, profits are not expected to be so good so on the consensus forecast, the shares trade on a forward PE of 11.1. At the year-end the group is in a net cash position of £9.1M compared to £6.6M at the end of last year.

Overall then, this seems like a decent set of maiden results for the group profit is up on last year, as is operational cash flow with plentiful free cash generated. Net assets did fall, however, but the balance sheet looks in decent shape, operating leases not withstanding. The sales of handbags, show care and online sales look set for further growth but they still represent fairly insignificant numbers compared to the sale of shoes from the stores. In conclusion, the shares do look cheap on most metrics but I feel it is prudent to wait for further updates given how little time the shares have been publically traded.