Shoe Zone has now released its interim results for the year ending 2015.

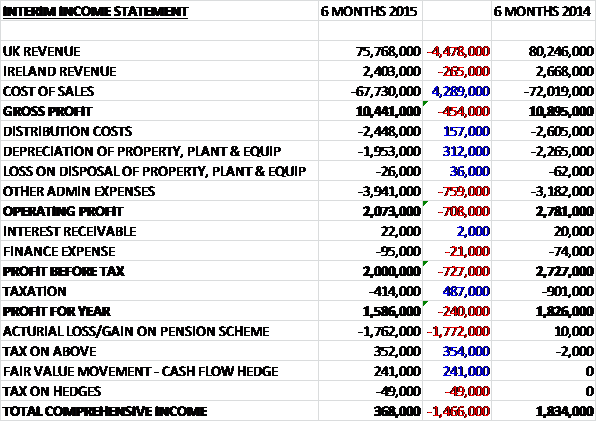

Overall revenues declined in the first half of the year as UK revenues fell by £4.5M and Irish revenues declined by £265K. Cost of sales also declined but the gross profit for the period was some £454K below that of the first half of last year. Distribution costs fell by £157K due to investments made in the Leicester distribution centre and lower fuel costs, and depreciation declined by £312K no doubt due to the reduced store estate but other admin expenses increased considerably to give an operating profit £708K lower. Finance expenses increased slightly but tax more than halved year on year to give a profit for the year of £1.6M, a fall of £240K year on year.

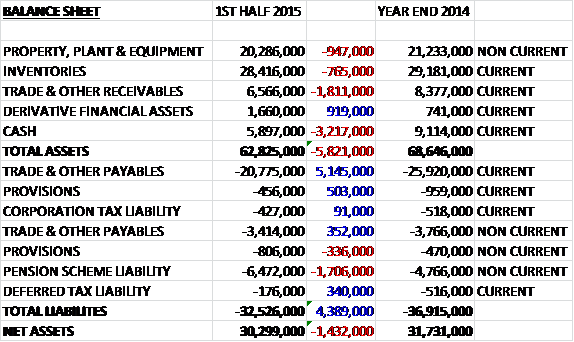

When compared to the end point of last year, total assets fell by £5.8M driven by a £3.2M decline in cash, a £1.8M fall in receivables, a £947K decrease in fixed assets and a £765K fall in inventories, partially offset by a £919K increase in derivative financial assets relating to the foreign exchange hedge. Liabilities also fell during the year as a £5.1M fall in current payables and a £503K decline in provisions was partially offset by an ominous £1.7M increase in the pension liability. Overall, net assets fell by £1.4M to £30.3M.

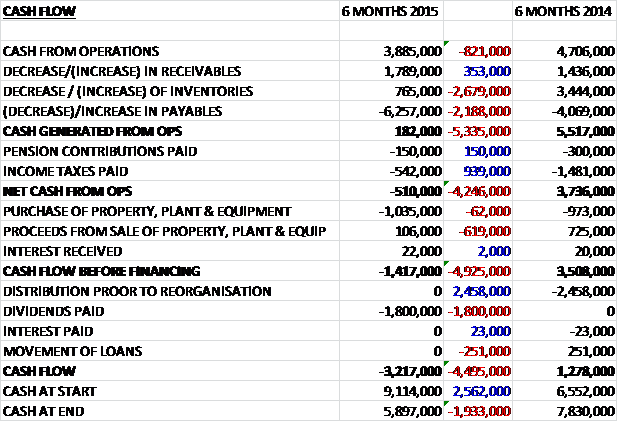

Before movements in working capital, cash profits fell by £821K year on year to £3.9M. We then see a massive fall in payables which meant that after lower pension contributions and tax payment, there was still a net operational cash outflow of £510K, a negative swing of £4.3M when compared to the first half of last year. The group then spent £1M on property, plant and equipment to give a £1.4M cash outflow before financing. After the payment of £1.8M worth of dividends, there was a cash outflow of £3.2M and a cash level of £5.9M at the period end.

The warm weather conditions had a material impact on autumn/winter trading which slowed revenues towards the end of the first half. While footwear volumes increased, the average price was down due to the different product mix sold with lower priced ladies ankle boots being favoured over long leg boots. In addition, the wider market continues to experience deflation in clothing and footwear.

The product range has continued to evolve with significant improvements to bags and sundries. The bag ranges for the winter and summer season have been relaunched with a strong focus on value with the range now being offered in store at the price points of £8, £10 and £13. The sundries and shoe care range has been expanded and are held in a defined space near the till. The group plans to build upon these growth areas in the second half.

Since the start of the year the group has opened five new stores, relocated four stores and refitted 18 more. They have closed nine loss making stores and will open, relocate and refit a further group of stores in the coming year. In all, there are now 541 stores compared to 545 at the end of last year with more large stores and less smaller stores. The profitability of stores is being improved by rent reductions with rents on renewal for the six months falling on average by 28%.

Online revenues were up 30% in the period and contributed at a higher rate than the average high street store. Following a successful trial on eBay, the group completed their full launch in October which is achieving good results, already accounting for 7% of online revenue. Amazon continues to grow and now represents 17% of online revenue and the email club has grown 14% over the first half of the year. The website now has a fully responsive checkout and the business continues to invest in online development.

Going forward, current trading has remained in line with expectations following the April trading update with the online performance remaining strong and ahead of market growth projections. The group has a net cash position of £5.9M at the period end compared to £7.8M at the end point of last year. The shares currently yield 3.9% which increases to 5.4% on next year’s consensus forecast which seems like a good rate of return.

Overall then this was a poor first half of trading for the group. Profits fell as a result of warm weather and deflationary pressures, net assets declined as the pension scheme deficit increased and there was a cash outflow at the operating level. Online revenue is improving, however, and the shares seem to yield a decent dividend. It seems rather poor that there was so little visibility over the effect the weather would have on sales but the shares seem to be fairly well valued at the moment. A tricky one this – perhaps I might be tempted if trading improves.

After the initial shock from the profit warning, the shares seem to have traded within a certain range but the underlying trend might be gently up.

On the 27th October the group released a trading statement covering the full year. They traded well in the second half of the year and expect to report revenues for 2015 in the region of £166.8M compared to £172.9M in the previous year with pre-tax profits expected to be in line with expectations. They ended the year with 535 stores having opened 18 and closed 28 during the period and ended the year with a net cash position of £14.2M compared to £9.1M at the end of last year.

On the 30th October the group announced that CEO Anthony Smith and COO Charles Smith sold 1,386,472 shares at a value of £2.6M and 1,108,528 shares at a value of £2.1M respectively. They still hold 28% and 22% of the company’s capital respectively so while it is always disappointing to see directors selling shares, they still have big interests. It was also announced that the wife of CFO Nick Davis purchased 15,700 shares at a value of £30K. This is Mr. Davis’ first interest in the shares and is small fry really compared to the huge sales.