Arbuthnot has now released its interim results for the year ending 2015.

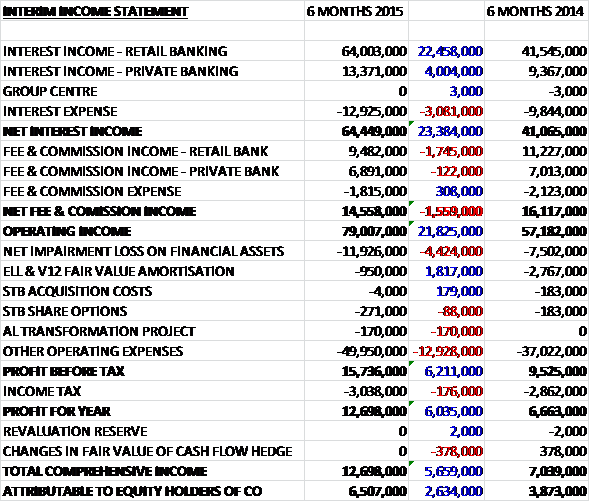

Net interest income increased by £23.4M year on year as a £22.5M increase in retail banking interest income and a £4M growth in private banking interest income was partially offset by a £3.1M increase in interest expense. Conversely net fee and commission income declined during the year due to a £1.7M fall at the retail bank and a £122K decline at the private bank to give an operating income some £21.8M ahead of the first half of last year. There was then a £4.4M increase in financial asset impairment losses and a £12.9M increase in underlying admin costs but the fair value amortisation charge fell by £1.8M to £950K and after a tax bill just a small amount higher than last year, the profit for the half year period stood at £12.7M, almost doubling year on year, up by £6M.

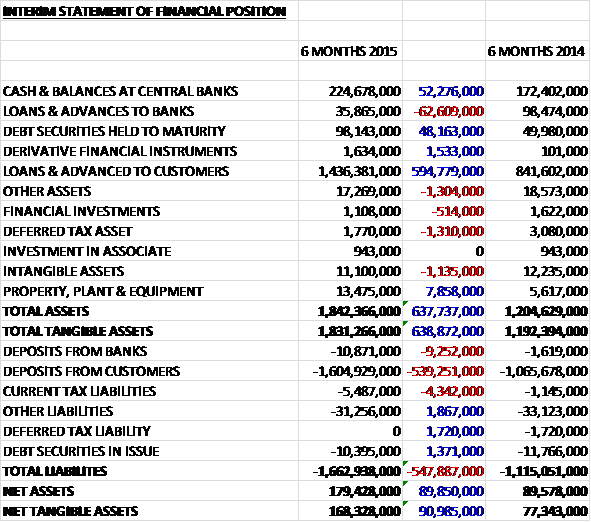

When compared to the half year point of last year, total assets increased by £637.7M driven by a £594.8M increase in loans to customers, a £52.3M growth in balances at central banks and a £48.2M increase in debt held to maturity, partially offset by a £63.2M fall in loans to other banks. Liabilities also increased during the year due to a £539.3M increase in deposits from customers to give a net tangible asset level of £168.3M, an increase of £91M year on year.

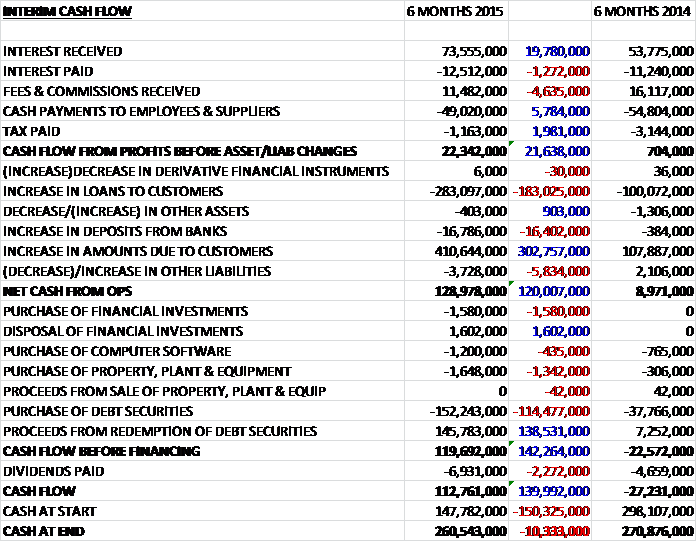

As we have already seen, the group increased the amount of interest received but saw the amount of fees and commission fall. Cash payments to employees and suppliers also fell by £5.8M and tax was nearly two million pounds lower to give a cash flow from profits of £22.3M, an impressive increase of £21.6M year on year. We then see a £283M increase in loans to customers and a £16.8M increase in deposits from banks more than offset by a £410.6M increase in amounts due to customers to give an operational cash flow of £129M, an increase of £120M when compared to the first half of last year. There was then a net £6.4M purchase debt securities and a £6.9M payment of dividends to give a cash inflow of £147.8M for the half year period and a cash level of £260.5M at the end of the half year.

The segment profit at the retail bank was £13M, an increase of £4.5M when compared to the first half of last year with continued positive trends in the customer lending balances which have grown by 90% year on year. Of the more established consumer finance businesses, motor finance and retail finance have performed well with the motor finance book increasing by 19% to £152M and the retail finance lending growing from £91M to £163M driven by good lending volumes generated from the sport and leisure, and cycle businesses. The SME lending growth has exceeded expectations, mainly due to the real estate and asset finance products. The real estate finance loan balances have increased from just £13M at the half year point of last year to £266M at present. The asset finance portfolio has risen to £30M and invoice finance now stands at £16M, both of which commenced business within the last year.

The segment profit at the private banking division was £3.7M, an increase of £2M when compared to the first half of 2014 with the Dubai office contributing a loss of £66K compared to a loss of £520K last year. The increase in profit is a result of investment in hiring additional private bankers over the past two years which has led to a substantial increase in new clients opening accounts. In addition to recruitment in London, the bank has also developed in other markets. The South West office in Exeter has agreed a lease and will move into its new premises in the second half of the year, the Manchester office has completed further recruitment of both private bankers and a wealth planner and the Dubai office should break even in the second half of the year, just two years after opening.

Included in the customer loans is the residential mortgage portfolio that was purchased in December and the ownership of these mortgages is now in the bank’s own name as of June and they have entered into a servicing agreement with Exact Mortgages. The bank is now embarking on three significant investment initiatives to support its future growth. Firstly they have begun an upgrade of their operations which includes paperless workflow, standardised customer interaction and the implementation of a new banking platform which is expected to be completed by the end of 2016. Secondly the bank has agreed terms to secure 10,000 square feet of additional office space in the City on a short-term lease to be occupied in the second half of this year – the exact reason for this remains a mystery though. Finally, and most interestingly, the bank is embarking on its expansion into commercial banking. Initially the focus will be on providing business banking services to its entrepreneurial private banking clients but the scope should increase in future. They have started recruiting for this new venture but the proposition is not expected to launch until 2016.

Overall the economic environment remains favourable which should allow both banks to continue to grow. With a business friendly government in office over the next five years, the board expects the banks to maintain their momentum and continue their long term investment plans, although they will remain vigilant over the political and economic events in Europe. The board have increased the interim dividend by 1p to 12p which means the shares are yielding 1.7% on a rolling annual basis.

Overall this seems like it has been a good six months for Arbuthnot. Profit nearly doubled and is being driven by both the part owned retail bank and the fully owned private bank. Net assets also increased and the group had a healthy level of cash inflow during the period. The retail bank is benefiting from growth in retail finance, motor finance and real estate finance while the private bank is benefiting from a lot more people opening accounts. Going forward, the commercial banking services look rather exciting although we are unlikely to see a contribution from that until next year. We should also be able to see the Dubai office starting to contribute to profits too. The exuberance should be tempered by the new tax levies the government has implemented that adversely affect the smaller challenger banks and would hit One Savings Bank, but despite this I have decided to take a position here.

The shares have struggled to get above 1,600 over the past year and are still pretty much trending along although the most recent decline has definitely been reversed following the last results.

On the 15th October the group released a statement covering trading in Q3.

Secure Trust Bank traded strongly during the period. Demand for its consumer lending products remained healthy, especially in Retail and Motor Finance where lending volumes are materially higher than the previous year. The SME lending divisions continue to make progress and as a result the overall lending volumes of the bank have now exceeded £900M. The business continues to see favourable conditions in the retail deposit market and remains able to match its lending growth by attracting deposits to various fixed rate products.

The bank is in the process of developing a deposit platform that will enable it to offer cash ISA products and Ian Henderson has been appointed who will be responsible for strategy, personal lending and mortgages. He was recently the CEO of Kensington Mortgages.

Arbuthnot Latham has continued to see an increase in the number of new client introductions and is now taking on more than fifty new clients per month. They have seen an increase in market activity following the general election and as a result, a healthy pipeline of approved lending applications has been generated. The improvement in the property market has resulted in the repayment of a number of loans, however, as projects have been completed. This has resulted in an apparently temporary slowing of the growth in customer lending balances but given the pipeline, the board anticipate that this will recover and the year-end balance will be in line with market expectations.

Following the bank’s intention to develop its commercial banking capabilities, it has announced the arrival of Stephen Fletcher to lead the business. He was previously an MD at Coutts with over 25 years of experience.

Overall the group is confident that it can continue to make positive progress and take advantage of the opportunities that exist for both its banks. They therefore expect results to be in line with market expectations for the year as a whole. This is a fairly decent update and I am happy to remain a holder here but it does sound as though AL might miss its customer lending targets if the pipeline does not come good.

On the 26th November it was announced that Robert Wickham was retiring as deputy chairman of the group having been a part of the story here since way back in 1993. He will leave at the end of the year.

On the 14th January the group released a pre-close trading update for the full year where they stated that they continued to trade well in Q4 and expect to report a pre-tax profit in line with market expectations.

Secure Trust Bank saw strong overall growth in its lending portfolios, which resulted in the total loan book closing in excess of £1BN, a growth rate of over 70%. Its consumer lending was led by Retail Finance and Motor, with new volumes materially higher than in the prior year. The business has continued to make progress in the development of its SME lending activities during the year and the bank has seen strong demand for Asset Finance, Invoice Finance and Real Estate Finance with new lending volumes 65% higher than in 2014. Conditions in the savings market remain favourable as the bank continues to see good inflows of deposits across its product offerings and the bank remains strongly capitalised and well-funded.

At Arbuthnot Latham, customer lending balances have ended the year in line with market expectations. The other lines of business in the private bank have continued to make good progress while the commercial banking division remains on track with its developments. During Q4, the business was in negotiations to purchase a second portfolio of residential mortgages but when the Bank of International Settlements published its second consultative document on its proposed revision to the standardised approach for credit risk in December, management decided that the direction of travel indicated would result in the anticipated return on capital from the mortgage portfolio would fall below the desired target levels so they withdrew their offer which resulted in transaction costs of £450K.