Entu has now released its interim results for the year ending 2015.

Overall revenues fell year on year as a £682K increase in home improvement revenue and a £110K growth in repair and renewal service agreement revenue was more than offset by a £3.5M fall in energy generation and saving revenue and a £500K decline in insulation revenue. Depreciation increased slightly but other cost of sales fell by £1.8M. We then see a £281K increase in admin expenses as a result of the company’s admission to AIM, offset by a fall in tax and after the £404K loss from the discontinued operation is taken into account, the profit for the half year comes in at £2.7M, a fall of £1.6M when compared to the first half of last year.

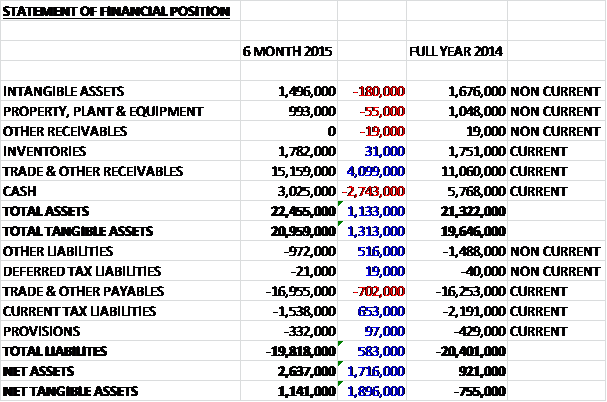

When compared to the end point of last year, total assets increased by £1.1M as a £2.7M fall in cash and a £180K impairment of intangible assets due to the discontinued operation, was more than offset by a £4.1M increase in receivables. Conversely liabilities fell during the period driven by a £653K fall in current tax liabilities and a £516K decline in “other liabilities” partially offset by a £702K increase in payables. The end result is a £1.9M increase in net tangible assets which are now positive at £1.1M.

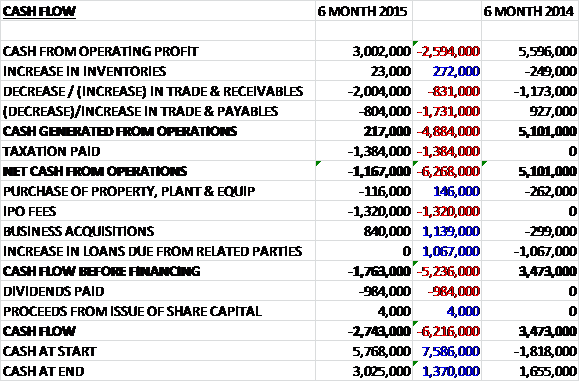

Before movements in working capital, cash profits collapsed by £2.6M to £3M. This was then eroded further by the £2M increase in receivables and a fall in payables and after a hefty tax payment of £1.4M there was a £1.2M cash outflow at the operating level compared to a £5.1M cash inflow at this point of last year. There was minimal capital expenditure and the group managed to gain a net £840K cash inflow from the acquisition but the IPO fees were paid during the period to give a cash outflow of £1.8M before financing and after the £984K dividend payment, the cash outflow for the period as a whole was £2.7M to leave a cash level of £3M at the year-end so clearly this situation cannot continued for much longer.

Overall performance was in line with management expectations against an unusually high prior year comparator. I find this quite a curious statement. If this is correct, then why wasn’t the fact that last year’s result was a one-off good performance mentioned at the time? It was also stated that operating profit was below that of last year reflecting normal seasonality of the business. Again, I find this quite strange as the comparison is the same time of year! While I am on a bit of a whinge, the current asset figure in the audited annual result for 2014 doesn’t add up – I suspect a typo under the trade and other receivables column, probably as a result of having to rush the results out following the collapse in the share price prior to them being published.

Underlying operating profit at the home improvements business was £2.4M, an increase of £700K when compared to the first half of last year which also represented an improvement in operating margins reflecting the benefit of the group’s efficient integrated Job Worth Doing platform which undertakes the product installations. A corporate contract with a national DIY retailer has now been agreed and anticipated revenues from this venture are expected to build to about £10M with the opportunity to cross sell other services.

The underlying operating loss at the energy generation and saving business was £252K, a negative swing of £1.3M when compared to the first half of 2014. The division clearly had a challenging six months due to lower solar panel product sales as the potential customer base becomes accustomed to lower tariff levels from the sale of surplus energy generation back into the grid, along with significant departures and disruption in the sales and marketing teams over the period. The group have now strengthened these teams and they expect activity to improve in the second half of the year. They also have a healthy pipeline of commercial solar business following the agreement of a solar PV contract with a European procurement organisation for an initial 1000 homes with revenues of approximately £4.5M and the opportunity to cross sell other services.

The underlying operating profit at the repair and renewal service business was £914K, a decline of £27K year on year despite a 10% increase in revenues as a result of increased sales commissions driving growth – it is expected that operating profits will rise in subsequent periods. The underlying operating profit at the insulation business was £794K, a decline of £1.1M when compared to the first half of last year which reflects a reduction in Energy Company Obligation funding (the revenue the group receives from utility companies in respect of carbon offset tonnage arising from the supply and installation of insulation products) across the sector which has fallen from £80 to £22.50 per carbon tonne. The group are installing a greater volume of products this year and the forward order book has risen from £2M to an astonishing £14M.

During the period the group started negotiations for the disposal of its kitchen retail operation as it represents a line of business that doesn’t fit into the overall strategy of the group. The business suffered an operating loss of £248K during the half year period and also had its net assets written down by £156K to zero.

During the period the group acquired Astley Facades that gave the group complementary commercial cladding operations across the UK. Despite initially paying £200K for the acquisition, the group has managed to have this consideration repaid after the event due to the need to add provisions for potential bad debts. The acquisition comes with no net assets and nothing was paid for the group which is a bit of a strange state of affairs. Also despite contributing £420K to revenues there was a zero contribution to operating profits/losses. This seems like a good fit for the company and they appear to have got it for free so I guess it is a good piece of business but given the figures supplied it is quite difficult to make a judgement. The group have suggested that they are looking for further acquisitions to enhance their geographic reach and product offering.

There have been a number of recent board changes. Phil Anderson joined as marketing director with responsibility for brand management and marketing initiatives across the group. After the year-end Geoff Stevens was appointed as CFO with Darren Cornwall remaining on the board as group corporate development director, focussing on furthering the group’s acquisition strategy and integration of acquired businesses.

Going forward the group is targeting the North West region in particular and are set to launch a new TV advertising campaign in the second half of the year and increase their online presence and the value of web sales. Additionally having already negotiated a supply and installation agreement with a well known corporate brand the group are looking for more such deals. Finally they are continuing to develop their proposition in home automation which sounds rather exciting in a market that is expected to triple in size over the next three years.

The total future order book has now grown to £30M from around £10M at the same point of last year which looks promising. The board has seen increased activity in the second half and they remain on track to meet market expectations (whatever they are!) with the second half of the year apparently being seasonably stronger. The European Court of Justice recently ruled that the UK’s 5% rate of VAT on energy efficient products is in breach of EU law, raising the prospect of an increase of the VAT rate to 20%. The group already applies a full 20% rate of VAT to the large majority of its home improvement products and the impact of the rate change is not expected to be material.

After the “special” final dividend of 1.5p was declared at the end of last year, an interim dividend of 2.67p has been declared at the interim stage which gives a rolling annual yield of 3.7% which doesn’t seem too bad. They also still intend to declare a final dividend of 5.33p per share which would give an astonishing annual yield of 7.1%. The group had a net cash position of £3M at the period end, an 83% increase year on year.

So, this is a really interesting update. Actually it has been a poor first half for Entu, profits were down, mainly due to people being less likely to buy solar panels after the cost of energy fell, the loss of a proportion of the sales and marketing team and the reduction in the eco funding for the insulation products. A knock on effect is that the operational cash flow collapsed and was negative during the period, not helped by a big increase in receivables. Astonishingly the group then claim that this performance was in line with management expectations! So management were expecting to lose much of their sales force? In addition, there was a blatant leak of these poor results as the share price crashed days before their released which obliged to the group to rush these results out early.

On the surface there were actually some decent points, the underlying double glazing business is actually performing well, the contract with the DIY retailer is certainly material on a revenue level (although no mention is made of profitability), the order book trebled to £30M and there is a stonking potential dividend on offer. Unfortunately I have completely lost confidence in the board to be truthful about any of this though so I see the seeming value on offer here to be a bit of a value trap. It could be that management are just naïve rather than being wilfully untruthful but I can’t really see this as a serious investment (although there could be a short term trading opportunity as people come in for the divi.)

We can clearly see the dubious price action before the release of the results – although the volume wasn’t that massive, the price came down considerably.

On the 1st September the group released a trading update. The anticipated improvements in the solar division during the summer months had not materialised and the board expects the market environment for solar to become increasingly difficult as a result of speculation about a possible increase in VAT from 5% to 20% and uncertainties concerning the future levels of feed-in tariffs , in particular a recent government proposal for a substantial reduction in these tariffs from the start of 2016. The company now expects that it will lose more than £2M during the current year from its solar activities against a budgeted contribution of £1.6M. It is not expected that the solar business is likely to make an acceptable return on investment in the medium term and therefore it will be discontinued.

Following the developments in the solar business, the group now anticipates that full year results will be below market expectations and it expects to make an operating profit from continuing activities of about £8M. The board apparently remain confident of the future prospects of the other activities which trade in line with expectations. In light of this update, the company is reconsidering the final dividend and instead of the mooted 5.33p pay out, it is now expecting to pay out 2.67p which shows the folly of suggesting such an ambitious unsustainable pay out in the first place in my view.

This is clearly very disappointing for shareholders and the board here are really not covering themselves with glory and seem very naïve as this profit warning cannot come as a total shock. Perhaps all of the bad news is now out, who knows, but the dividend pay-out is clearly not set in stone.

It was also announced previously that non-executive director David Grundy stepped down from the board with immediate effect.

On the 27th November it was announced that Chairman David Forbes purchased 50,000 shares at a cost of £30.4K. This is his first share purchase and while welcome is not really a huge amount.

On the 14th January the group announced that Geoff Stevens stepped down as CFO and assumed the role of non-executive director and he will be replaced by Neill Skinner. The board had previously intended the CFO role to be part time but has changed its mind! Neill has previously been CFO at Clean Air Power. Current MD of Entu Energy Services, Andrew Corless, has also joined the board as COO having been with the company since September 2014. The group have also indicated that they expect their results for the year-ending 2015 should be in line with expectations.