Amino Technologies has now released their interim results for the year ending 2015.

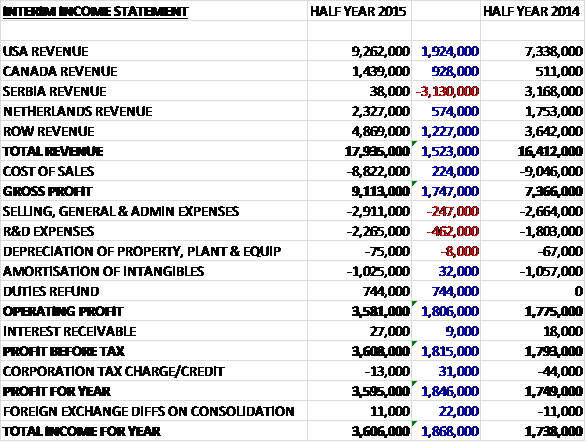

Overall revenue increased by £1.5M year on year as a £1.9M increase in US revenue, a £928K growth in Canadian revenue and a £574K increase in Dutch revenues was partially offset by an almost complete collapse in Serbian revenue. Cost of sales fell during the period which meant that gross profit increased by £1.7M to £9.1M. We then see a £247K increase in selling & admin costs, partly relating to legal costs associated with the acquisition, and £462K growth in R&D expenses relating to development of x5x and live products but there was a £744K refund of past duties paid which represents the final rebate, and after tax the profit for the half year was £3.6M, more than double the £1.8M profit recorded in the first half of last year.

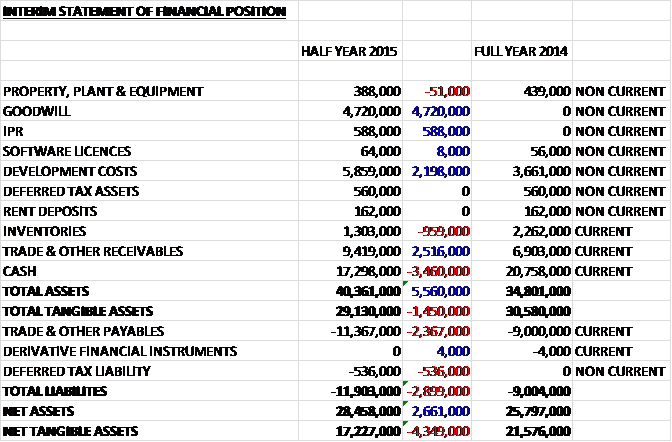

When compared to the end of last year, total assets increased by £5.6M driven by a £4.7M increase in goodwill, a £2.5M growth in receivables and a £2.2M increase in development costs (relating to both internally generated costs and those that came with the acquisition) partially offset by a £3.5M fall in cash and a £959K decline in inventories. Liabilities also increased during the period due to a £2.4M growth in payables and a £536K increase in deferred tax liabilities. The end result is a £4.3M fall in net tangible assets to £17.2M.

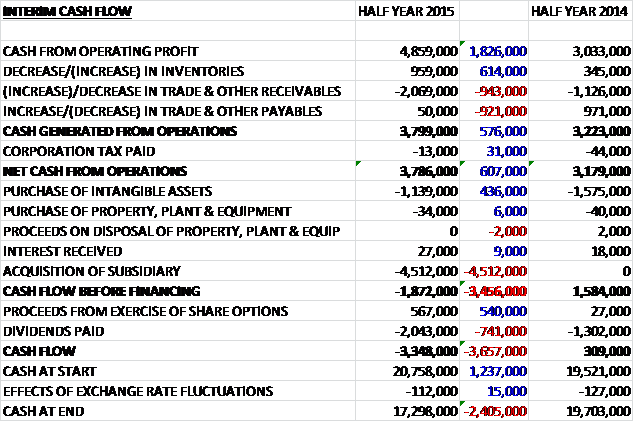

Before movements in working capital, cash profits increased by £1.8M to £4.9M. A large increase in receivables, however, eroded this somewhat and net cash from operations for the first six months of the year was £3.8M, an increase of £607K year on year. The group then spent £1.1M on intangible assets – probably development costs, to give a free cash flow of £2.7M which was not enough to cover the £4.5M spent on acquisitions let alone the £2M of dividends to give a cash outflow of £3.3M for the half year and a cash level of £17.3M at the period end – a great cushion but it seems the group has now found something to spend it on, more on that later.

Over the period the board has seen a considerable evolution within the Pay TV industry where the shift towards “TV everywhere” viewing across multiple TV, smartphone and tablet screens is accelerating. At the same time, the timeframe within which new 4K Ultra-HD services are expected to be deployed by service providers has also shortened which has brought forward the group’s plans to introduce services to support this new medium.

The strong demand seen in the key North American market at the end of last year continued into 2015 and demand from existing customers grew strongly along with a number of new contract wins. New products launched into the market were well received and the group received further orders for the Live Advanced Media Platform from an existing customer and good initial take-up of the A150 IP device which was introduced into the market during the period. The group has added certified YouTube capability alongside Vudu video on demand and the Amino TV appstore which has been well received by operators but progress on the availability of Home Reach has been slower than expected with commercial trials now underway with a regional operator in North America.

In Latin America, the demand for lower spec products remains strong with substantial orders received from an existing customer in Chile. There was also progress in the Argentinian market where Catel, the association representing some locally-focussed IPTV operators, launched a second phase of their IPTV deployment using the higher spec A150 device. Europe remains challenging, however, despite the good progress made with key customers in the Netherlands where the A150 continues to be the product of choice for new deployments. Some progress has been made in the Middle East where focused sales and marketing activities are beginning to generate orders. This will continue into the second half of the year with a focus on developing partnerships with key regional systems integrators to address new hospitality, residential compound and digital signage opportunities. A new H150 IP device was launched during the period to address these markets.

As mentioned above, TV viewing has continued to grow outside the home on smartphones and tablets. This means that operators are looking to deliver these services with a consistent look and feel that retains their brand. In line with the increase in consumer demand for 4K TV sets the company showcased their new 4K platform which is based on the widely deployed Aminet software to customers at the major TV connect industry event in April and availability is likely in early 2016 in line with operator deployment plans.

During the period the group acquired Booxmedia, a Software as Service cloud TV platform provider based in Finland. The company was acquired in order to enhance the group’s offering by adding a cloud based platform which can enable the delivery of “TV everywhere” entertainment to a full range of IP connected devices. The total consideration was £7.5M, generating goodwill of £4.7M and consisted of cash of £5M, shares worth £483K and contingent and deferred consideration of £2.1M. If the acquisition had been made at the start of the year, the business would have contributed £114K to group profits. I think the total cost of this acquisition had a view on the future rather than the profits generated at the current time.

At the end of the period the group had a net cash position of £17.3M compared to £19.7M at the end of the first half of last year with the decline attributable to the £4.5M of cash spent on the acquisition of Booxmedia. After a 10% increase in the interim dividend, the shares now yield 3.2% on an annualised basis which increased to 3.5% on the consensus forecast for the whole year. Going forward, the board remains confident of meeting market expectations for the full year.

On the date of their interim results, the group also announced the acquisition of Entone for a total consideration of £46.7M comprising of initial cash consideration of £41.6M, £3.2M on the first anniversary of completion and a further £1.9M on the second anniversary. The acquisition will be funded by the placing of shares to raise £21M, existing cash reserves equal to £17.3M and a revolving credit facility with some £5.1M expected to be drawn down.

Entone is a provider of hybrid TV and connected home solutions and the acquisition is expected to enhance Amnio’s global footprint and is expected to be significantly earnings enhancing in the first financial year of ownership (2016). In the 11 months to May, Entone had EBITDA of $4.1M from revenues of $46.7M and had net assets of $15.9M including net cash of $12M. The acquisition provides an opportunity to consolidate one of the group’s direct competitors and will assist with evolution of HEVC and 4K UHD along with offering a direct sales route into the US. Key synergies of about £1M in the first full year of ownership have been identified.

The group was particularly interested in two Entone products, FusionHome, a home monitoring solution, and Engage, a hosted field service software suite including a secure environment for remote management of device firmware and provision data along with remote support and service information diagnostics. Other core product offerings include Hybrid TV devices and software that provides flexible home networking options with models ranging from media players to home servers; and FusionTV, applications that enable the delivery of TV services from the cloud. Entone has over 150 global customers and is a market leader in the US IPTV market. Core customers include Consolidated Communications, Canby Telecom, Cable & Wireless, Fair Point Communications, Vodafone, Three Rivers and Twin Lakes.

The group is raising £12M from the placing of 16,153,846 shares at a price of 130p per share which represents a 6.5% discount to the closing price the date before the announcement. Unfortunately the placing will be restricted to institutional investors and the directors of the company. Following the issue of the new shares, the enlarged share capital will be 74,407,743.

Overall then this seems like a good update from the group and profit in the first half of the year doubled, albeit aided by the duties refund. Net tangible assets did fall, as the group spent cash to acquire goodwill but operating cash flow increased year on year. Outside Europe, sales have been good and the group’s products seem to be in good demand. The results were overshadowed by the acquisition, though. It is clearly transformational and seems like a good use for that pile of cash the group has been sitting on over the past few years. I do hope they take some time to allow the acquisitions to bed in though and hope they don’t get hooked on acquisitions. One thing to watch out for is the deferred consideration – there is £2.1M outstanding from the Booxmedia acquisition and £5.1M from the Entone acquisition so together the £7.2M is a very material amount for a company of this size.

Overall though, I am more than happy to hold at the present time while we see how the acquisition beds in.

On the 27th October the group released a trading update. They expect to report a second half shortfall in revenue against expectations within the core Amino business. As a result, they expect pre-tax profit to be below expectations, in line with that achieved last year. The company also confirms that revenue and cost synergies arising from its recent acquisition are tracking ahead of plan and are integrating well. Net cash balances are still expected to be in line with expectations and the dividends are unaffected.

They have identified that their sales execution efforts in the second half of the year were not satisfactory. Whilst a small proportion of the trading shortfall is due to the consolidation of certain customers and delays to some orders where the customer is considering the transition to 4K UHD services, sales execution is the primary factor in the shortfall. As a result, the company has implemented a series of targeted actions across the business.

I have to say that this profit warning is very disappointing and I did not see it coming. It seems to me that the group have taken their eye off the ball with the core business and instead have been focusing on the acquisitions – they are not experienced acquirers after all. I would like to think, therefore, that this is temporary but the lack of any further detail on what exactly went on and how long it will take to fix means that I have sold out here. What a shame.

On the 3rd December the group released a trading update for the year ending 2015 where they state that they are trading in line with revised market expectations for both revenue and pre-tax profit. The net cash position at the end of the year was £2.1M and ahead of market expectations. Further to the earlier profit warning, the group has restructured its sales team to address the problems in execution experienced in the second half of the year. The new integrated sales organisation across the Amino and Entone businesses will be led by Steve McKay, the former CEO of the acquired Entone group. They now have a better sales focus in all key regions, with dedicated teams for Latin America and Europe and a new combined sales team for North America.

The group continues to make solid progress with regard to the Booxmedia and Entone acquisitions that were completed during the year. The Entone acquisition is expected to drive significant cost synergies and the integration of teams and product lines of each acquired company is on schedule. The acquisition of Entone has strengthened the combined group position in North America with the addition of direct Tier 2 operator customers – Cincinnati Bell and Consolidated Communications, complementing existing distribution partners serving Tier 3 operators. The enlarged group has also brought stability in Western Europe to a wider base of Tier 2 operator customers. Eastern Europe has been more challenging, with the potential consolidation of a major SE Eastern European customer, impacting further roll out of their IPTV solution.

Booxmedia sales and marketing plans have progressed well with two major customer wins secured in H2 2015. Dutch utilities and digital services company DELTA selected Booxmedia’s white label platform and products to provide, install and maintain a new end to end multiscreen cloud TV solution. Belgian broadcaster RTL selected Booxmedia to provide, install and maintain a full end to end cloud video on demand platform.

It was also announced that CFO Julia Hubbard has taken a short leave of absence from the business with Julian Sanders stepping in on an interim basis having previously taken on the role during Julia’s maternity leave in 2014. Her leave of absence has now been extended beyond the short period originally envisaged by the board.

Overall then it seems as though progress is being made but I would like see some evidence that their new sales team is improving the situation and the situation with the CFO sounds rather concerning.