Goodwin has now released its prelim results for the year ended 2015.

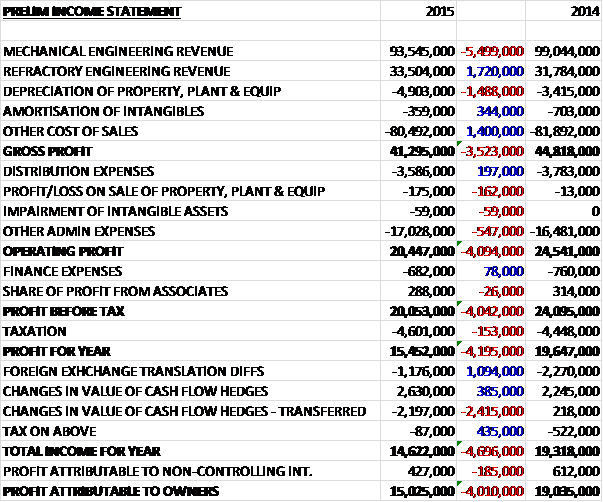

Overall revenues fell year on year as a £1.7M growth in refractory engineering revenue was more than offset by a £5.5M decline in mechanical engineering revenue, driven by falls in the US and the UK. We then see a big increase in depreciation, counteracted by falls in other cost of sales to give a gross profit £3.5M below that of last year. Distribution costs fell modestly but admin expenses increased which was not helped by a £175K loss on the disposal of fixed assets to give an operating profit £4.1M down from 2014. After an increase in tax and a fall in finance expenses, the total profit attributable to the owners fell by £4M to £15M.

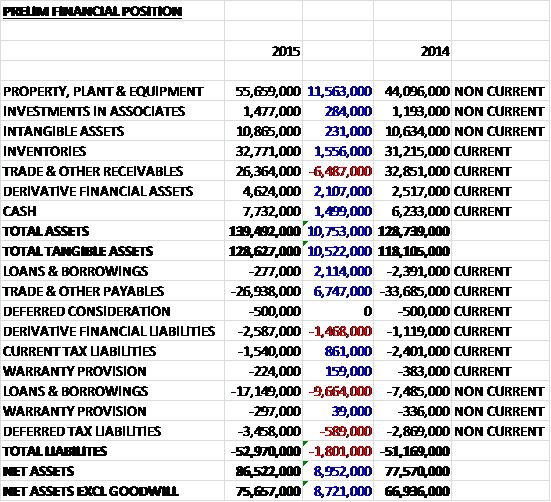

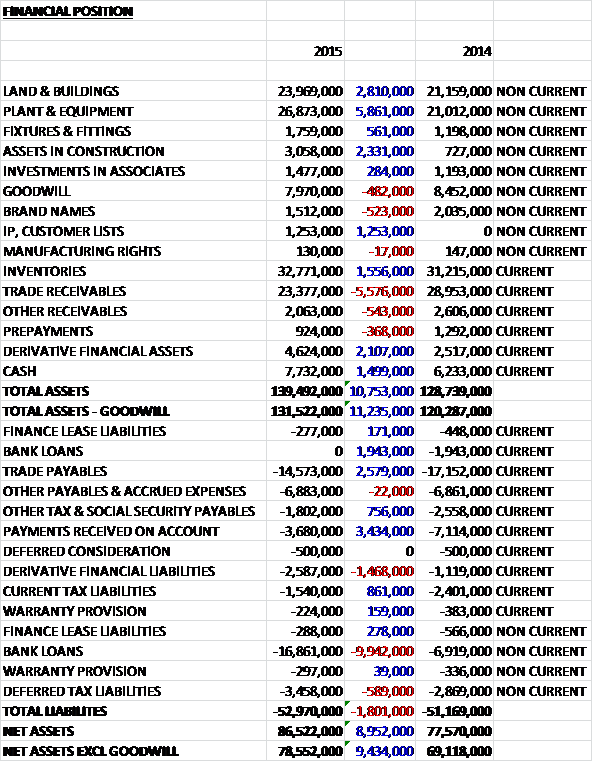

When compared to the end point of last year, total assets increased by £10.8M driven by an £11.6M increase in property, plant and equipment, a £2.1M growth in derivative financial assets, a £1.6M increase in inventories and a £1.5M growth in cash levels, partially offset by a £6.5M fall in receivables. Liabilities also increased during the year as a £7.6M increase in borrowings and a £1.5M growth in derivative financial liabilities was partially offset by a £6.7M fall in payables. The end result is an £8.7M growth in net tangible assets to £75.7M.

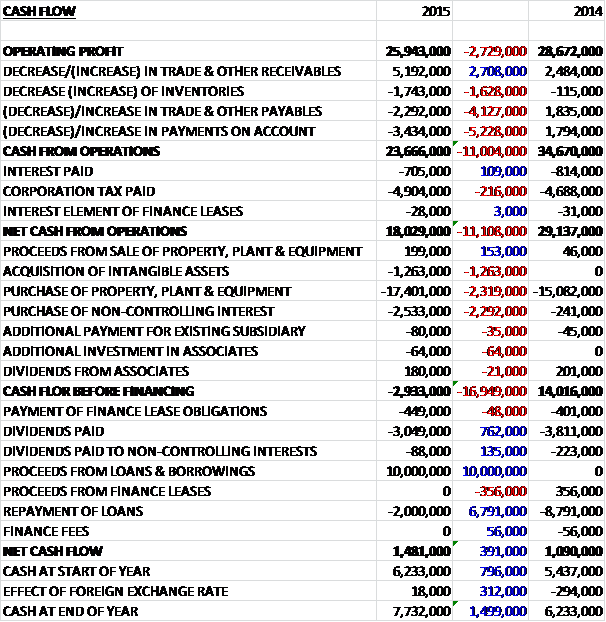

Before movements in working capital, cash profits fell by £2.7M to £25.9M but detrimental movements in all working capital items except receivables, plus an increased tax bill partly offset by a fall in interest paid meant that net cash from operations was £18M, a decline of £11M year on year. This cash just about covered capital expenditure in fixed assets of £17.4M but doesn’t quite cover the £1.3M of intangible assets acquired or the £2.5M spent on the purchase of non-controlling interests relating to the 20% minority interest in Gold Star Powders India and Goodwin Pumps India, along with the 49% minority interest in Gold Star Brazil, to give a cash outflow before financing of £2.9M. The group then paid finance leases of £449K and dividends of £3M which it couldn’t really afford so took out a net £8M of new loans to give a cash flow for the year of £1.5M and a cash level of £7.7M at the year-end.

The profit at the mechanical engineering business was £16.4M, a decline of £2.9M year on year and the profit at the refractory engineering business was £5.1M, an increase of £1.3M when compared to last year. The deterioration in profits stems from the oil and gas engineering market sector with order placing activity having substantially contracted in Q1 with order input in that quarter being 32% down on the same period of last year (the group derives some 45% of sales from the oil and gas sector). This situation did improve throughout the year to the extent that order input for the full twelve months was only 19% down on 2014. The lower level of available orders also resulted in higher competition which has and will impact on margins and profits. At the end of the year, group workload stood at £79M, a reduction of 22% year on year.

The group have been investing quite a bit in R&D in recent times and in the last two years have applied for five patents in 16 countries. It is hoped that within the next three years orders for these products will start to be received and that they will command decent gross margins. The patents relating to the refractory division are AVD (Aqueous Vermiculite Dispersions) used in fire extinguishers and Micashield, a fire resistant paint for wood structures and other substrates. The patents in the engineering division are for a new type of axial piston valve and a new type of nozzle check valve. In addition, the castings business has been granted a patent for its new super nickel alloy, G130, developed for use in high temperature turbine applications.

Just before the end of the year, the refractory services business signed an agreement to purchase the technology, customer list and other assets from a French casting powder company but the cost has not been disclosed. This purchase has enhanced the moulding material technology for the casting of tyre moulds and glass within the group and the tyre mould technology has brought with it associated patent rights with exclusive worldwide rights for use in reclaimable patterns and the lost wax casting industry.

Going forward, the level of workload has improved in the first two months of the new year which, according to the chairman, leads to the possibility that the performance in Y/E 2016 will not be as bad as feared. Some markets will remain difficult over the next couple of years but the group also expect to see continued growth in the refractory engineering sector and the board believes that the recent investments will enable the group to continue with its track record of growth.

At the current share price the shares trade on a PE ratio of 12.1 and after the dividend was held at the same level, the yield stands at 1.7%. These figures are not too bad but don’t really point to an undervalued share in my opinion. Frustratingly there are no broker estimates that I could find.

Overall then this has clearly been a difficult year for the group. Profits are down, driven by a fall in income from the much larger mechanical engineering division which relies on the oil and gas industry. We also see operating cash flow falling and there was no free cash flow generated at all during the year. The group still paid out some £3M in dividends which, while I understand why they did it, I don’t really agree with – when the dividends are held steady it tends to suggest the company is probably paying out more than it is comfortable with in my experience. There are some fairly good signs, though, the net tangible asset level improved considerably during the year and the board still see growth as a probability this year. In conclusion, this is clearly a quality outfit but in my view the share price doesn’t completely factor in the difficulties facing the group’s largest market in the coming year so I will continue to watch with interest from the side lines.

There has been some slight consolidation following the downtrend that has been in evidence through the year but an uptrend has yet to have been established.

Goodwin has now released their annual report for the year ended 2015.

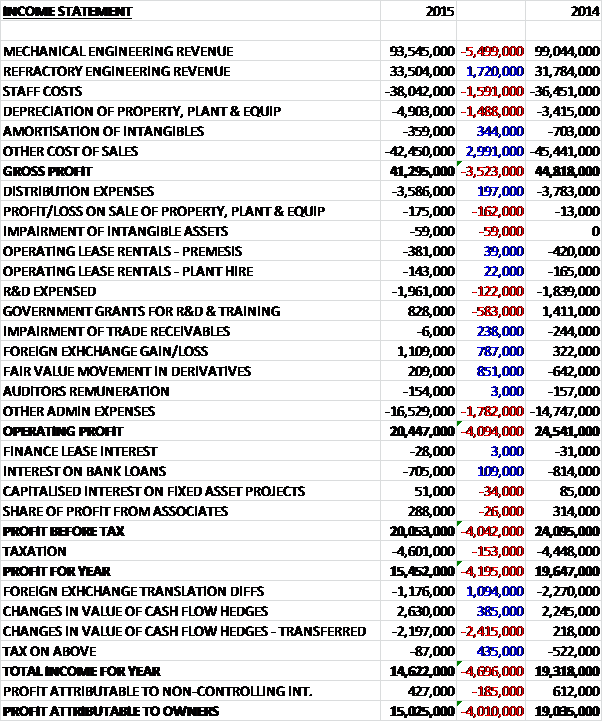

Within admin expenses we can see that the group benefited from a positive movement in foreign exchange and derivative financial assets, along with a lower impairment of trade receivables, although underlying admin expenses did increase. There was not really much else new to note when compared to the prelim results though.

We can see that within fixed assets, most items increased, in particular plant and equipment and within intangible assets, an increase in IP and customer lists was offset by a decline in goodwill and brand names. We can also see that all kinds of receivables fell when compared to last year. As far as liabilities are concerned, the fall in payables was driven by declines in trade payables and payments received on account.

The only other thing of interest really is the £672K increase in operating leases outstanding to £1.5M, although these remain modest relative to the size of the company.

On the 10th September the group announced its Q1 trading update. Revenues in the quarter were down by £6.3M to £33.5M and profit nearly halved to £3M. The Q1 sales order input was up 36% compared to the same quarter of last year when the downturn in the oil and gas industry activity started to hit but, whilst the order input is similar to 2013 and 2014, the profit margins on many of these new orders will be lower due to the increased level of fight needed to win the business in the quieter market. This is not a good update and whilst Goodwin often release RNSs at strange times, releasing this one just before the market closed does not strike me as best practice. Disappointing.