Sylvania Platinum has now released its final results for the year ended 2015.

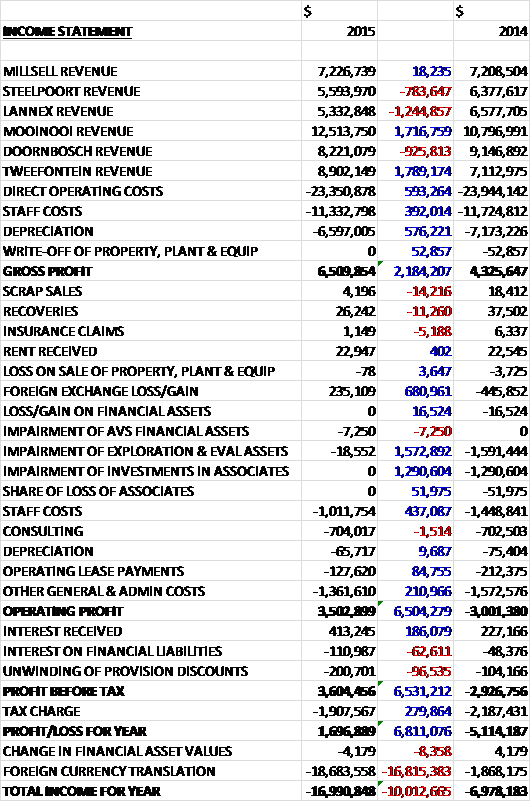

When compared to 2014, total revenues increased as declines in sales at Lannex, Doornbosch and Steelpoort were more than offset by growth at Mooinooi and Tweefontein. Staff costs and depreciation both fell to give a gross profit $2.2M higher than last year. We then see a positive swing in foreign exchange as far as costs are concerned, further lower staff costs and a decline in other admin costs, along with the lack of $2.9M-worth of impairments that occurred last year. After tax and finance costs, the profit for the year came in at $1.7M, compared to a loss of $5.1M in 2014. It is also worth noting that there was a huge $18.7M loss on foreign exchange translation.

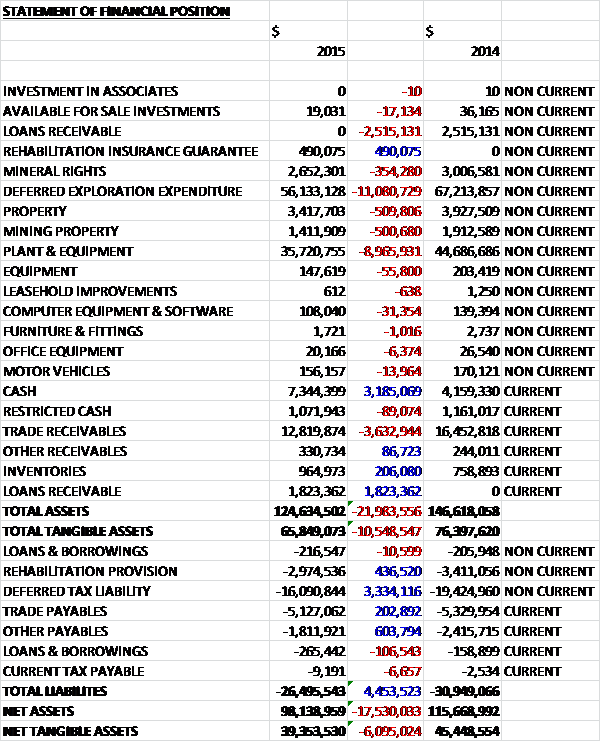

When compared to the end point of last year, total assets collapsed by $22M driven by an $11.1M fall in deferred exploration expenditure due to foreign exchange losses, a $9M decline in plant & equipment (due in part to exchange differences and partly due to the depreciation being higher than capex), and a $3.6M fall in trade receivables partially offset by a $3.2M increase in cash. Liabilities also fell during the year, mainly due to a $3.3M decline in deferred tax liabilities to give a net tangible asset level of $39.4M, a fall of $6.1M year on year.

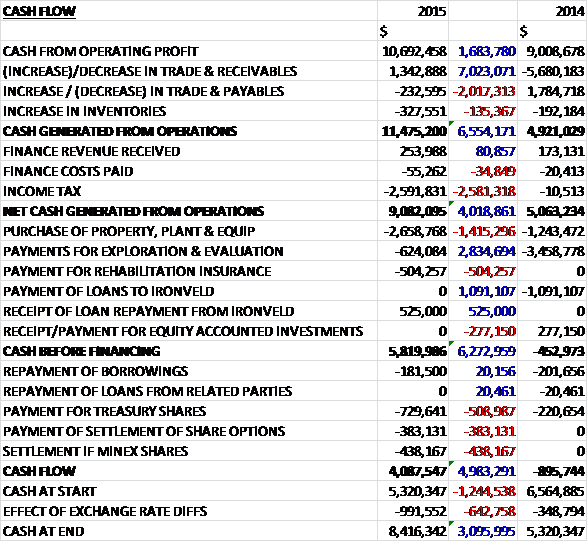

Before movements in working capital, cash profits increased by $1.7M to $10.7M. This was further improved by a fall in receivables, but there was a much bigger tax payment this year so that the net cash from operations stood at $9.1M, an increase of £4M year on year. The group spent $2.7M on property, plant & equipment relating to new tailings facilities at Lannex, Doornbosch and Tweefontein along with the changeover to a hydro-mining process; $624K on exploration and they used the receipt of loan repayments from Ironveld to pay for rehabilitation insurance to give a free cash flow of $5.8M. The group then spent $730K on treasury shares, $438K on the settlement of Minex shares, $383K on the settlement of share options and $182K on loan repayments. In all, there was a $4.1M cash inflow for the year to give a cash level of $8.4M at the year-end which looks like a very good performance to me.

Profits at the Millsell plant were $2.7M, an increase of $500K year on year; profits at the Steelport plant were $687K, a decline of $400K when compared to last year; losses at the Lannex plant were $1.7M, a deterioration of $1M when compared to 2014; losses at the Mooinooi plant were $176K, an improvement of $1.6M year on year; profits at the Doornbosch plant were $2.8M, a fall of $300K when compared to last year; and profits at the Tweefontein plant were $2.2M, an increase of $1.6M year on year. The average basket price during the year fell to just $1,072 per ounce and the cash costs per ounce fell by 9% to $603 per ounce.

The main issue for the group has been the continued decline in the platinum price. The metal started the year at $1,497 per ounce and finished the year at just $1,078 per ounce. The decline was partly mitigated by the South African Rand’s decline against the US dollar but in a market that has been oversupplied and in which production additions are still being made to increase mine capacity and where high-cost production is being cross-subsidised there appears little prospect of much of a recovery in the price. Labour conditions in the country have improved after a five month strike last year but the mining labour environment in the country remains a concern for the sector in general.

During the year the group set a company annual record for SDO production at 57,587 ounces, a 7% increase from the 53,808 ounces achieved last year. The SDO began the year with a sixth consecutive quarter of continuous growth in Q1. This tapered off in Q2 and Q3 largely as a result of the start-up and commissioning of hydro mining, the planned holiday shut down period and a structural failure on the Lannex plant’s thickener which resulted in some downtime at the plant. Community unrest as a result of poor municipal service delivery exacerbated operating conditions at the Eastern operations as employees were prevented from entering the plants. The change over from mechanical mining of the dumps to a hydro-mining process is expected to reduce mining costs by up to 20% going forward.

Feed material to the operations declined slightly from Q2 onwards due to the start of second-pass treatment at Millsell, Lannex and Doornbosch, as well as the final scrapings at the Steelpoort dump, but these stabilised at lower production rates to align with the annual guidance. As a result, plant feed tons for the year are down 15% to 2,129,352 tons but a 13% increase in the feed grades to 2.31g/ton combined with the subsequent upgrading of the PGM’s before flotation contributed to the annual production achieved.

The company received word that the mining rights for PGMs and iron ore, vanadium and heavy minerals was awarded to a subsidiary at Harriet’s Wish, Aurora and Cracouw. The official signing to execute the mining right has been delayed, however, pending a request to the DMR to reduce the amount of financial provision for rehabilitation. After the year-end, the DMR agreed to reduce the financial provision to R6M. A financial guarantee will be issued and arrangements made for execution of the right which will be followed by an application to transfer the right to mine iron ore, vanadium and heavy minerals to Ironveld in terms of the transaction concluded in 2013.

The group continues to await the outcome of the mining rights application from the DMR for the Volspruit project which appears to rest on the decision taken by the LEDET whether to grant an Environmental Authorisation to mine. The company remains confident that the decision will be favourable but LEDET requested clarification from the group on certain aspects of the Environmental Impact Assessment as well as an instruction to provide biodiversity and wetland offset strategies. The decision by LEDET is expected within the following six months. In addition, a submission of the application for the Water Use License will require preliminary civil designs of all dam facilities and as this will result in further costs, these activities have been postponed pending the decision on the MRA and environmental authorisation.

At the Grasvally Chrome operation, it has been discovered that the resource contains some of the best quality chromite in the country, comparable with Turkish-grade chromite. Exploration continued over the northern portions of the property in order to declare a SAMEC compliant resource which will be required in order to apply for a mining right over the resource. Exploration is expected to be completed by October and as the company has no intention of becoming a Chrome miner, the Grasvally project will most likely be available for sale during 2016. The intention is to become a platinum miner at Volspruit but in order to do so, the group would have to raise substantial capital or find a joint venture partner, both of which are uncertain given the availability of mining capital in the current market.

The group has used forecast commodity prices for between 2016 to 2018 of between $1,400 to $1,600 per ounce for platinum and $850 to $875 for palladium in their models. As the current platinum price stands at $1,023 per ounce, there is the potential for some impairments going forward. A further 10% fall in platinum group metal prices would reduce profits by $704K with the opposite movement having the opposite effect (although I doubt that is very likely).The vast bulk of revenues were made to two customers and in the notes it states that the contract for one of them was terminated in May. There is no other mention of this in the report so I am not sure what kind of impact this is going to have.

Going forward, the first half of next year will be difficult and platinum prices are not expected to move in the group’s favour. Operationally, the board remain positive despite the difficult conditions and they will continue to pursue the benefits of optimising their operations. They are working to resolve the technical problems at Mooinooi and all other operations are approaching or are at steady state so it is expected that they will produce 55,000 ounces at a cash cost of under $700 per ounce and a capital expenditure of $3M.

I have to mention an extract from the chairman’s letter at this point – it certainly raised a chuckle from me and I quote: “Let me dwell further on a recent near miss…. The five or so tons of platinum South Africa produces each year is overwhelming the market and platinum miners, being the go-getters that they are, cannot be persuaded to moderate their output to balance the market. We were however, recently spared a possible glut when an asteroid with a 90M ton core of pure platinum passed within a whisker of our planet. If our mining companies had been quicker off the mark, they might have extracted enough metal from the flying rock to cover the entire Bushveld complex with platinum to a depth of a foot. Mind you, had the asteroid landed on top of the Bushveld complex, our present problems might have seemed as trifling as this interlude”. I love that!

During the year Grant Button has left after spending 11 years on board and he was replaced by Eileen Carr who has previously been finance director at Cluff Resources and is currently non-executive director of Nobel Holdings, a Russian Oil and Gas company.

At the current share price the shares trade hands on a PE ratio of 27.3 which apparently falls to 8.9 on WH Ireland’s forecast for 2016, which I personally find very hard to believe. The group still has some $2.9M of undrawn borrowing facilities available and plenty of cash so it doesn’t look as though they are in any immediate danger from the declining platinum price.

Overall then, this has actually been a good year for Sylvania. The profit is up, as is operating cash flow and the group has a decent amount of cash as a safety net. The net asset level did fall, however, mainly as a result of the depreciation in the South African Rand but the balance sheet remains strong. Operationally, most plants are doing well but technical problems beset the Mooinooi and Lennex plants and the Steelpoort plant seemed to struggle a little bit. The group produced some 57,587 ounces this year and plan to produce about 55,000 this year. The Grasvally chrome project sounds interesting and I do find myself wondering what kind of ball park figure will be realised from the potential sale of the project next year.

The main issue clouding the company, however, is the price of platinum. It has fallen from $1,497 at the end of last year to $1,078 at the end of this one and the group does not quite realise this full price from their sales. Their costs are only $603 per ounce, aided by the deterioration in the South African Rand but as long as the oversupply in the market continues and the price remains subdued, things will remain difficult for all producers of the metal.

This chart seems to have broken down somewhat, whether the 200day moving average will act as some support remains to be seen.

On the 24th August the group announced that a fire at an electrical substation had affected the Mooinooi dump and ROM plants. The cause of the fire is yet to be confirmed but it is believed to be related to a current in-rush as a result of a power failure. Production losses are currently being incurred but it is expected that a temporary substation and electrical equipment will be installed before the end of the week.

In addition, Lannex and Steelpoort have been affected by recent violent community protest regarding demands for improved infrastructure and jobs. The communities have now withdrawn the protests, however, and operations in the area have returned to normal. It is anticipated that these events could result in production during Q1 being up to 1,000 PGM ounces lower than expected but the group should still be able to achieve the 55,000 ounces forecast for 2016.

On the 28th October the group released an update covering Q1 2016. The dump operations produced 13,729 ounces during the period, a 2% improvement quarter on quarter. This increase is attributable to a slight improvement in recoveries, despite lower PGM plant feed grades and lower tonnes treated. The cash costs fell by 17% to $532/Oz whilst in Rand terms, costs were down 11%. This reduction is as a result of improved maintenance planning and cost controls at the operations combined with the improved recoveries.

The gross basket price dropped 15% to $879/Oz mirroring the platinum price which fell to a six year low at the end of September. Despite the higher ounces for the quarter, therefore, the low metal prices resulted in a 12% drop in revenue to $8.8M. The group cash balance at the end of the period was $6.8M, down from $8.4M at the end of the previous quarter with the reduction attributable to a cash outflow of operations of $90K due to the low basket price and reduction in pipeline finance; cash spent on sustaining capex and exploration assets rights applications of $400K; $400K spent on share purchases and $100K on rehabilitation guarantees. As much of the cash is held in Rand, the Rand/Dollar exchange rate movement resulted in a further reduction of $500K in dollar terms.

Despite the lower metal prices, electronic substation fire and subsequent one week downtime at Mooinoii, as well as two weeks of violent community protests at the Eastern operations, all of which impacted negatively on plant availability and tonnes treated during the quarter, the higher ounce production and lower unit costs resulted in group EBITDA improving significantly quarter on quarter to $1.25M. The basked price of platinum remains a concern for the foreseeable future but the group are confident that the SDO can continue to produce profitably provided prices do not drop significantly further and management continue to keep tight control on costs.

At Volspruit, following a review of all comments received and completion of the comments and responses report, the Addendum and report was delivered to LEDET and the DMR in mid-September. LEDET has 120 days in which to consider the addendum and if it accepted, another 30 days to grant the EIA.

The Grasvally mining right application for chrome was submitted in September and has been accepted by the DMR. The exploration programme has been completed over the northern portions of the site in order to declare a SAMREC compliant resource which will be required by the company in order to exercise a mining right over the resource. With all logging and data collection completed following the drilling programme, the work to compile the resource statement is in its final stages and expected to be completed by the end of October. It is expected that the resources will comprise a SAMREC compliant shallow indicated resource and a deeper inferred resource.

At Harriet’s Wish, the company received the decision from the DMR to reduce the amount of financial provision for rehabilitation in August. Arrangements have been made to issue the financial guarantees in order to provide for this reduced financial security for rehabilitation. It is anticipated that this will be received shortly, thereafter arrangements will be made with the DMR for the notarial execution of the mining rights. Application for ministerial consent to transfer the right to mine iron ore, vanadium and heavy minerals to a subsidiary of Ironveld has also been submitted. Hacra must now proceed with the water use license application but this will be delayed as the original land owners are all deceased and the company will have to facilitate the transfer of the title deeds to the lawful land occupants and descendants of the original land owners. This process will then allow the application to be submitted on agreement to the project by the current land occupants.

Overall then this update is not that bad considering the very poor platinum price but until sentiment picks up in the metal, this seems like quite a difficult investment.

On the 28th January the group released a Q2 update. The dump operations produced 15,791 ounces in the quarter, a 15% improvement on Q1. This increase was attributable to a combination of higher tonnes treated (15% improvement) and an improvement in both plant feed grades (3.5% improvement) and recovery efficiencies (8%) for the quarter. The cash costs decreased by 21% in dollar terms to $420 per ounce, aided by the weak rand but in rand terms, cash costs also fell by 13%.

The gross bucket price of $785 per ounce represents an 11% decrease compared to the $879 achieved in Q1, having fallen from $1,082 since the beginning of July. Despite this decline, however, revenue increased 10% to $9.7M due to the increase in volumes produced.

The group’s cash balance at the end of the period was $5.1M, a $1.7M fall on the previous quarter. Cash generated before working cap movements was $2.5M with net operating cash of just $500K after working capital is taken account for. They also spent $800K on tax, $400K on stay-in business capital for the plants and $400K spent on share purchases. The impact of exchange rate fluctuations on cash held was a decrease of $500K.

The communities in the East of the region have continued their violent protests demanding jobs and better infrastructure, which resulted in some production down-time, although this was less than in Q1 and accounted for about one week, and the precious metals market has also been strongly affected by the decline in platinum and palladium prices in recent times. In the early part of 2016, the price of platinum has shown little sign of recovery and the palladium price has dropped even further. Despite all of this, the group EBITDA increased by 83% to $2.3M.

At Volspruit, the company continues to await the decisions on the addendum and comments and responses report delivered last quarter. At Grasvally Chrome, the fulfilment of the most recent exploration phase, an upgraded mineral resource estimate has completed. The mining right application for chrome was submitted in September and has been accepted and the environmental impact assessment document was released to the interested and affected parties in January with public participation meetings to be held in February. As previously stated, the company intends to sell this chrome deposit for cash and an international agent has been appointed to handle the marketing to potential ferrochrome smelters. There were no further developments at the other platinum exploration licenses.

Overall then, this update is not all that bad. Sure, the low price of platinum and palladium are taking their toll but by increasing production, the group seems to have remained fairly profitable. The ramp up of volume has taken its predicable toll on cash generation but this is to be expected. Also I have to wonder how much the group expects to get for the Chrome deposit. The market for steel is not great, which is where I suppose most Chrome ends up but this could still be a welcome cash injection. I am sorely tempted to get back in here to be honest.