BPI is a global producer of polythene films and supplies over 270,000 tonnes each year for a range of applications. They are also Europe’s largest recycler of polythene waste. Their products are used across a range of market sectors with a focus on agriculture/horticulture (31%), retail food chain (32%), industrial (12%), construction (14%), healthcare and waste services (7%) and non-food retail (4%).

In Agriculture and horticulture, the group provides silage products, greenhouse films, polytunnel covers, packaging for retail horticulture (compost bags), animal feed packaging and fertiliser packaging. In non-food retail, they provide mailing bags and garment film for on-line retailers, mailing film, transit packaging, and protective films for furniture and carpets. In the food retail chain, they provide bakery packaging, frozen food packaging, shrink film for cans and bottles, fresh produce packaging, refuse sacks and transit packaging. In Healthcare and Waste Services they produce refuse sacks, recycling bags, caddy liners and aprons. In construction they provide gas protection systems, structural waterproofing, protection films, ventilated cement sacks, overwrap films for insulation and packaging for aggregate and bricks. In Industrial, they provide container liners, heavy duty sacks and pallet protection for polymer producers, additives manufacturers, specialist chemical companies, salt producers and fuel producers.

Some major clients include Tarmac, Britvic, Bunzl, Coca-cola in UK and Europe, Saint Gobain, United Farmers, Greif, Unilever, Sainsbury, NHS, Next, Princes Foods, Tesco, Travis Perkins, Veolia, Warburtons, Morrison, Dow, Total, Ineos, McCain, and United Farmers of Alberta.

The European business comprises two manufacturing sites in Belgium, one in the Netherlands and a sales operation in France. The business specialises in the manufacture and sale of high quality printed film for the food industry, form fill and seal films and heavy duty sacks including valve bags for the chemical, construction, horticulture and fertiliser industries. The UK and Ireland business consists of 15 UK manufacturing sites and three sales offices. It also includes the manufacturing plant in China as most of its production is currently sold in the UK. The North American business is based in Edmonton, Canada and manufactures polythene film for the agricultural and horticultural markets and also includes a conversion facility in nearby Westlock which folds and packs bags used for the storage of silage and grain.

Films are plain film on reel products and recycled products are manufactured from recycled polythene scrap. Silotite is used by farmers to securely ensile their forage crops. BPI has now released its final results for the year ended 2014.

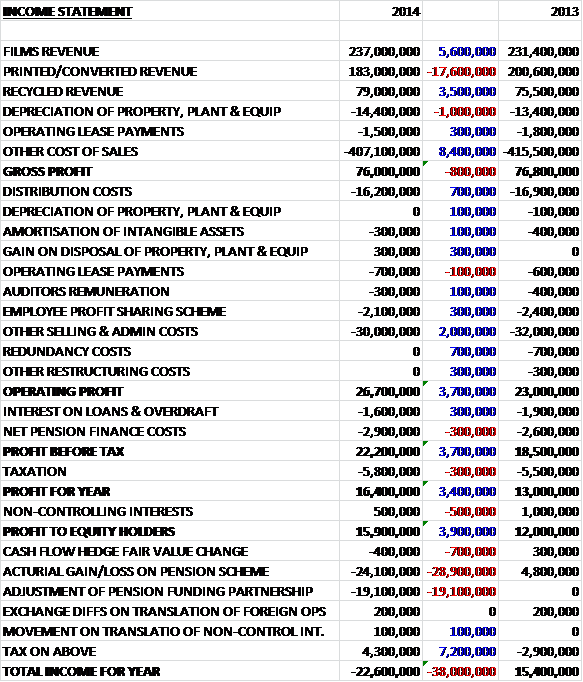

Overall revenues declined year on year as increases in films and recycled revenues were more than offset by a £17.6M fall in printed revenue. Cost of sales also fell, despite an increase in depreciation, to give a gross profit £800K below that of last year. Distribution costs fell by £700K and admin costs were £2.8M below that of 2013 and when £1M of restructuring costs that occurred last year did not repeat in 2014, the operating profit was some £3.7M ahead. After interest costs, pension costs and cash are taken into account, the profit for the year stood at £15.9M, an increase of £3.9M year on year.

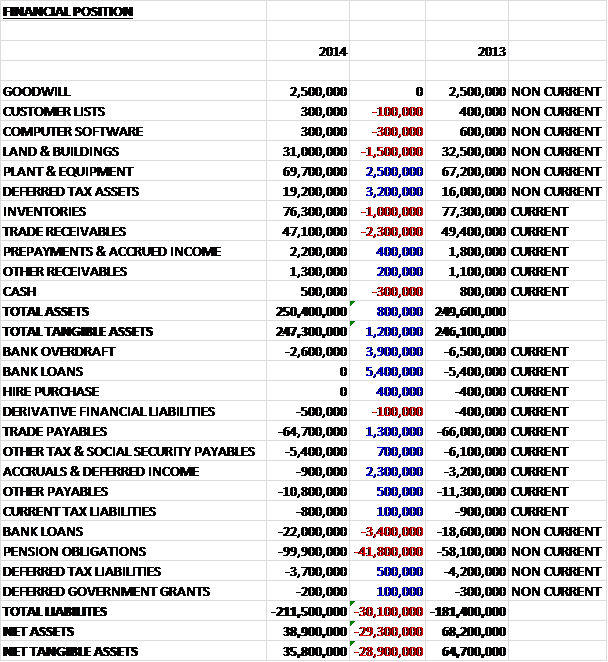

When compared to the end point of last year, total assets increased by just £800K as a £3.2M growth in deferred tax assets and a £2.5M increase in the value of plant and equipment was offset by a £2.3M fall in trade receivables, a £1.5M decline in land and buildings and a £1M fall in the value of inventories. Liabilities increased considerably driven by a £41.8M growth in the pension obligations, partially offset by a £5.9M fall in borrowings, a £2.3M decline in accruals and deferred income, and a £1.3M decrease in trade payables. The end result is a net tangible asset level of £35.8M, a fall of £28.9M year on year.

Before movements in working capital, cash profits increased by £4.2M to £42.7M. This was eroded somewhat by a fall in payables and payments to the pension scheme and after lower interest and tax was paid, the net cash from operations increased by £5.8M to £29M. The group then spent a net £15.8M on property, plant and equipment along with £300K on acquisitions so that the free cash flow stood at £12.9M, which looks rather good. After dividends were paid and shares were repurchased along with a modest repayment of borrowings the group had a cash inflow of £3.2M for the year.

The European polythene film extrusion market was estimated at around 7.5M tonnes in 2014 and no individual business has more than 5% of the market. Total market volumes have shown growth during the year with the recovery focused on packaging for food although market volume has been impacted by the continuing trend towards stronger and thinner films. Carrier bag production in Europe has declined due to increasing volumes of imported bags and environmental pressures to reduce their usage. There are still a large number of paper sacks in use and market sectors such as animal feed, pet food and cement are under pressure to move to polythene sacks. The refuse sack market continued to be resilient despite movements to wheelie bins and communal containers.

The growth in flexible films for food packaging has been driven by changing consumer demands with the requirement for extended shelf life for fresh food and less spoilage. Away from the packaging markets, greenhouse film has been growing due to increasing demand to extend the growing season of many varieties of fruit and veg. Construction film volumes declined due to previous falls in construction markets, although some recovery has been seen more recently. Polythene film has been substituting other materials within the packaging industry such as paper and aluminium. The industry has now reached a degree of maturity and recent years have been challenging with growth rates now averaging less than 2% per annum, caused by slower economic growth, continuing thinning of films and increased import penetration of converted bags from Asia.

The underlying operating profit at the UK and Irish division was £11.2M, an increase of £2.5M year on year with contributions from the STC and Flexfilm acquisitions, operational improvements at Ardeer and a strong recovery in construction. Sales volumes increased to 193KT despite the loss of the bread contract. Sales of collation shrinkwrap, which are mainly to the food and drink industries, were in line with last year despite difficult trading conditions in the UK soft drinks industry as the business secured some new customers. The converter market remained flat with demand patchy but they did see some growth at some customers and were successful in winning some new clients.

The sites continued to operate efficiently with a focus on reducing scrap and operating costs. At Bromborough they commenced a programme to replace older equipment over a period of several years. Three new coextrustion lines are now installed to increase capacity, produce thinner films and offer customers improved performance. All three lines are now performing well with good outputs. External volume sales of silage stretchwrap were flat year on year despite a high level of carry-over stocks in the UK and Scandinavian markets. In the UK, the business continues to position itself as a supplier to the leading co-operatives and agricultural merchants who wish to sell their products. The Irish market remains the lowest priced in Europe and the focus there is on a restricted range of customers. The new complementary products helped to increase sales in overseas markets, however, particularly in Scandinavia and New Zealand.

Sales of Securap, a new product for bailing waste, increased by 8% but this new market suffered from credit related issues. Sales of the prestretched WrapsmartUltra continued to grow and were 20% ahead of last year including some volume from the STC acquisition. The Bridgewater site is fully focused as a low cost manufacturer of industrial cast stretchwrap. Sales of the product were lower than last year as it is increasingly imported from Asia. Sales of cast hand reels and cast Wrapsmart both increased and improved margins, however.

Widnes continued to produce a range of blown machine and hand reels for the packaging industry and despite strong competition in the conversion sector and a continuing move to prestretch products, volumes were broadly the same as last year. At Leominster the programme of investment to upgrade older extrusion equipment and improve output and quality continued as output improved with a good reduction in scrap. All conversion for Wrapsmart, including the STC machines, was moved to a new hall at the end of the year and should result in further increased efficiency and lower scrap next year.

The group is the leading recycler of waste polythene films in the UK. They recycle scrap from their own operations, used products taken back from customers and scrap purchased in the open market. Availability of scrap continued to be a key issue and they are now bringing in packaging scrap from Europe as scrap prices increased, putting pressure on margins. The intake of farm plastics increased and they now have availability from some national schemes in Europe. The recycled material is used in the manufacture of construction films, including damp proof course, refuse sacks, rigid products and a range of other products.

Construction activities continued under the Visqueen brand with the supply of construction films including protective sheeting, damp proof membrane, damp proof course and a number of other products to major builders’ merchants in the UK. Construction films continued to recover and volumes were 6% ahead of last year against an overall market recovery of 5%. The specialist gas and water proofing business achieved a significant increase in market share as it increased sales by 25%. They achieved this growth by establishing stocking centres at their customers last year which enabled them to service clients more efficiently. Some 29 centres were established by the end of the year and there are commitments for a further eleven centres. Following this success they have launched damp protection centres which will stock general purpose DPM and DPC.

Total tonnage of refuse sack sales increased by 3% with the main growth coming from the retail sector. Pressure on margin in all sectors remained intense, particularly as scrap prices increased and continuous development is needed to remain competitive. In the healthcare sector the business has supplied a range of waste sacks to the NHS and secured additional apron business in the second half of the year. At the start of 2015, they secured a contract to provide refuse and clinical waste sacks to the Scottish Health Service, replacing an overseas supplier. Sales of healthcare products to other customers also increased during the year.

Volumes to the local authority sector continued to reduce as councils move to wheelie bins or stop providing sacks. The loss has been replaced by continued growth in the retail sector along with the food services and facility management markets where new customers have been secured. The public sector remains an area of risk as they look for savings to meet their reduced expenditure targets. The group supplies both the NHS and local authority markets and continue to offer lower cost products.

While the group achieved growth in the retail sector, margin pressure remained intense and they lost a major contract at the end of Q3 but continue to supply a number of the larger national food retailers. Sales of the green sack range continue to grow and are used by both retailers and distributers.

Volumes at Heanor increased during the year and management changes have been made to improve production and efficiencies. A first coextrusion line was installed in December and results apparently look promising and should enable to the business to offer an improved range of products.

The industrial activities, which manufacture heavy gauge polythene packaging products, saw volumes increase by 5% with continued recovery in the construction sector and improved demand in peat, furniture and general industrial packaging. The group continues to see growth in volumes of the more complex printed cement sacks and expects to see further growth in 2015 due to additional customer wins including some export business. Sales volumes of peat and compost sacks for retail horticulture showed a small increase while volumes to the animal feed sector were down due to the extended mild weather. Packaging for furniture and carpets continued to recover and industrial packaging volumes improved as additional business from current customers was secured. Sales of garment film for online retailers were ahead of last year due to strong demand. Pallet stretch hooding volumes increased significantly as new customers were secured following the upgrade of lines in 2013.

The major site at Ardeer continued to improve its operational performance with a significant reduction in scrap, particularly in the new films hall which was opened following the transfer of business from Stockton. The new extrusion investment for heavy duty sacks continued to deliver higher outputs, improved film quality, lower scrap and energy costs and a further line was installed during Q4. Two further extrusion lines for other products have been ordered for installation in the summer of 2015 and a replacement eight colour printing press will be delivered in Q2. Greenock continued to perform well with higher volumes, lower scrap rates and reduced costs. Good growth was achieved in tissue overwrap film, liners, carrot covers and garment films.

Total volumes of agricultural film products sales increased by 40% with considerable growth in silage sheet as product was supplied to the North American business as its new line was being installed. Horticulture sales improved with growth in the UK and France as a new winder was installed at Adeer which improved the quality and appearance of the finished product.

At Worcester, sales volumes were significantly reduced following the loss of a large bread bag contract at the end of last year. The site was restructured at the end of 2013/start of 2014 with significant job losses and equipment moves. Surplus equipment including two printing presses and conversion equipment was transferred to Jordan Plastics. Volumes at Worcester remained under pressure throughout the year as a number of supermarkets reported lower sales and more produce was sold without packaging. Margin pressure remained intense as supermarkets and their suppliers attempted to continue to reduce costs. The strategy to broaden its customer and product base saw some initial results as they increased volumes in printed shrink and frozen food and secured business with additional supermarkets including the discounters, however.

The plant in China manufactures aprons on the roll, flat aprons and a range of bangs including refuse, swing and pedal, food and freezer. The group installed further extrusion equipment and an additional eight colour printing press to increase capacity for the production of packaging for bread and fresh produce. Total volumes were just behind 2013 as some refuse sack business was lost. At Jordan Plastics, capacity was increased by transferring two eight colour printing presses and four conversion machines buy unfortunately additional sales volume was not delivered and margins were impacted by the strength of sterling against the euro for the sales in Ireland.

The total capital expenditure in the UK business was nearly £12M as older equipment was replaced and new extrusion lines were installed at Bromborough, Adeer, Heanor and China along with a new recycling line at Heanor and a printing press in China. Planned expenditure for next year includes extrusion equipment for Ardeer and Bromborough and a replacement printing press for Ardeer.

The underlying operating profit at the Mainland Europe division was £16.3M, an increase of £1.9M when compared to last year despite an adverse currency movement of £900K as the business benefited from investment in new equipment and an improved product mix. Sales volumes were 5% ahead with growth in both silage and industrial products. Total sales of silage products increased by 11% due to good growing conditions, despite high levels of carry-over stock in some markets. Sales of the newer products SilotitePro and Baletite increased by 33% with market feedback continuing to be positive. Baletite is a replacement for traditional round bale netting and SilotitePro is a new generation of silage film with improved economic and environmental properties.

Aggressive competition due to the presence of carry-over stocks resulted in some margin reduction. In the first quarter the business completed the installation of a nine layer coextrusion line at Zele to meet the growing demand for these products, the full benefit of which will only be seen in 2015. The reduction in polymer prices may delay the start to the new season and result in a more difficult year with pressure on margins, but the good growing season this year has resulted in limited stocks in the supply chain.

Volume sales of printed film for the food industry were behind those of last year as some orders were delayed due to impending changes in food legislation. A new replacement printing press has been authorised to replace two older units and this will enable greater production efficiencies and a small increase in capacity. Demand in pallet protection film and general purpose film remained reasonable despite some competitive pricing but sales of the strategic product, stretch hoods, were up 28%. Sales of Bontite the high quality industrial stretch product showed an increase and new legislation on load stability should offer additional opportunities.

Following the transfer of a line from Zele, extrusion on Roeselare increased significantly as it now produces all the feedstock for printing at Zele. Total production at Roeselare was nearly 19,000 tonnes with growth in all strategic products. Sales volumes of the new thinner products for the insulation industry increased by nearly 22% year on year. Sales from the industrial film plant in Hardenberg in Holland increased by 3% with demand from the polymer industry steady despite difficult conditions. Sales of other FFS products grew by 8% but volumes of bags continued to reduce as customers moved to form fill and seal products. The plant also benefited from last year’s installation of a replacement eight colour printing press and a further eight colour printing press for FFS that was installed at the end of 2014. Production fixed costs and labour costs per tonne remained broadly flat year on year.

The group continued its investment in the business with the installation of a nine layer extrusion line at Zele for silage and a replacement eight colour printing press at Hardenberg for non-petrochemical form fill and seal products. Going forward, Zele in Belgium will continue to focus on stretch products, particularly silage and printed film for the food industry. Roeselare in Belgium will focus on a reduced number of products, including stretch hoods, feed stock for printing and a range of pre-stretched thinner products for the insulation industry. Hardenberg in Holland is focused on industrial products and is a leading supplier of FFS to the petrochemical and other industries. With further investments in capacity and the development of new and improved products, the business should deliver similar or better returns in future years.

The North America division recorded a loss of £800K, a deterioration of £1.7M year on year as the installation of the replacement of the largest extrusion line was delayed by nearly three months due to a major item being delivered behind schedule by a normally reliable supplier. Initial teething problems, particularly with the new winder, further restricted production and led to inefficient production runs as the focus was on satisfying customer orders in the second half of the year. Sales volumes were in line with last year as the product was sourced from the plants in the UK. Sales of agricultural products were up 10% with strong growth in silage and grain bags as new customers were added. Sales of sheet were also ahead of last year due to higher exports and better crop conditions but volumes in bale wrap were lower due to competitive conditions.

Horticultural sales fell by 20% as the business lost its major supply position at one customer and had difficulty in supplying the market in the second half. They are withdrawing from the low margin overwintering film and will now focus on greenhouse films. Higher polymer prices in the region despite low feedstock costs have encourage imports and placed pressure on sales pricing and margins. Some reductions were seen in the price of polymer towards the end of the year and the reductions have continued into 2015.

Scrap levels increased due to commissioning issues on the new line and inefficient production in the second half as the business struggled to meet customer demand. The new extrusion line is currently running well and it is achieving the expected outputs with good film properties. They are now producing an improved product and the group are looking forward to a more normal 2015 and return to profit.

Total capital expenditure of £17M was above depreciation. During the year the group completed two major strategic projects comprising a multi-layer coextrusion line for stretchwrap at Zele and a replacement seven layer agricultural line in Canada. Other major investments included the installation of two coextrusion lines at Bromborough to produce thinner films for food packaging, the installation of a replacement eight colour printing press for FFS film at Hardenberg to improve quality and increase capacity, the installation of additional extrusion and printing equipment in China, the replacement of recycling equipment at Heanor to increase efficiency and reduce costs, and the installation of a coextrusion line at Heanor to reduce costs and develop improved products.

At the year-end the group had outstanding contracts for capital expenditure of £5.8M and planned expenditure already authorised includes the replacement of an eight colour printing press at Ardeer to reduce costs, improve quality and increase capacity; the addition of two coextrusion lines at Ardeer to improve film quality and reduce scrap and energy costs; the replacement of an eight colour printing press at Zele to replace two older presses and increase capacity; and increasing the rewinding capacity in Canada to support a new extrusion line.

The cost of raw materials is currently reducing due to a decline in the price of naphtha, the main feedstock for the petrochemical industry in Europe, which should reduce the working capital requirement of the business going forward. The lower polymer prices are reflected in selling prices, however, so reported sales turnover will reduce. Energy costs reduced marginally in both the UK and Europe reflecting lower wholesale prices. Going forward, it is anticipated that wholesale energy price in the UK will reduce further but the overall costs is likely to increase due to higher energy taxes. Costs per tonne in the UK remains higher than in the European and Canadian operations and energy policies in the country continue to place intensive energy users at a competitive disadvantage in global terms.

In July the group acquired the pre-stretch business of STC including three converting machines. This is a small purchase, with sales of just 1,000 tonnes but will bring new customers, additional capacity and new products in the form of coreless pre-stretched reels to the group.

It was announced that after serving for nine years, non-executive Lord Jamie Lindsay is retiring from the board. It has to be said that the pay is very generous here with the directors being rewarded handsomely for average performances with the CEO earning £1.6M this year with an astonishing £843K through long term incentives. At least this was lower than the incredible £2.1M he earned last year!

The pension scheme seems to be a cause for serious concern for the company. The defined benefit scheme was closed to new entrants in 2000 and ceased future accruals in 2010. Despite this the scheme currently has a deficit of £99.1M on assets of just £232.2M (taking off the related deferred tax asset, the total liability is £83.1M). Contributions next year will consist of an annual payment of £3.6M, which will continue for the foreseeable, and an additional payment of £500K reflecting the company having reached an agreed profit target, this is in addition to the £1.9M paid out of the pension funding partnership. After the year-end, the company agreed with the trustees to change the index used to revalue pensions in payment from RPI to CPI, which reflects the current government guidance. The effect of this change would be to reduce liabilities as they currently stand by £27M. As part of the agreement the company has agreed to make a one-off payment of £11M to the scheme in June 2015.

In 2011 some freehold properties were transferred to a limited partnership established with the main purpose of leasing the properties back to group businesses and to provide the pension scheme with a distribution of the profits which is about £1.8M per annum. Apparently as the group has changed to the pension partnership agreement, restricting the ability of the scheme to sell or transfer its income interest without the consent of the group, the income interest no longer meets the criteria for recognition as a plan asset so it has been removed from the balance sheet. The result of this change has been to increase the pension obligation by £19.1M this year, being the fair value of the income interest. The scheme funding and cash flow benefits of the pension funding partnership are unaffected by this accounting change. As well as this £19.1M effect, the scheme was also affected by £25.2M due to changes in assumptions underlying the present value of scheme liabilities.

There is not a great deal of susceptibility to changes in interest rates with a change of 100 basis points resulting in a £100K change to profit before tax. There is more susceptibility to exchange rate changes with a 10 euro cent change against the value of sterling changing profit/loss by £1.2M. As well as the pension issues, the main potential risks include general economic conditions, raw material prices (linked to the price of oil), energy costs, weather conditions (for the agricultural end users) and perceived environmental issues.

Going forward, the group has made a good start to 2015. The order book is similar to the same time last year and good demand is expected from the agricultural sector in the coming months. The board anticipate a much better year in North America, continued progress in the UK and another good performance in Europe so they look forward to the remainder of the year with confidence.

The shares are currently trading on a PE ratio of 11.7 which reduces to 9.6 on next year’s consensus forecast, which looks very cheap. After a 10% increase in the final dividend, the shares are currently yielding 2.4%, increasing to 2.5% on next year’s forecast. At the year-end the group had net debt of £24.1M compared to £30.1M at the end of last year, partly as a result of the delay to some of the capital expenditure spend this year. The group currently has overdraft headroom of £18.4M an undrawn bank loan of £48M. There was also £4.2M in operating lease payables off the balance sheet.

Overall then this was a fairly solid set of results. Profits improved as costs fell and operating cash flows were also up with a decent amount of free cash being generated which was partly due to the slippage of some capital expenditure into next year. Net assets did fall year on year due to a huge increase in pension liabilities, partly affected by an accounting change but the pension is still a considerable drag on results as next year the group will to pay an £11M one-off payment to the scheme. This is a huge amount and really shows the issues here as despite measures in the past to tackle the deficit it still remains considerable.

The market as a whole is very fragmented and has pretty much reached maturity for the time being. The reduction in carrier bag usage along with refuse sacks is a bit of a drag on performance but this is offset by more plastic packaging required to improve the shelf life of fruit and veg and also greenhouse plastic to increase the growing season. Another driver is the construction market which is improving as the economic outlook in Europe starts to look a bit better.

The UK put in a decent performance due to an improving construction market and the improvements made at the Ardeer plant, partially offset by the loss of a large bread packaging contract. The move to establish waterproofing stocking centres at customers seems to be a good one and the opening of more of these should drive further growth. The European performance was good despite a weak Euro due to increased sales to the silage and industrial markets. The North American division was the source of problems, however, as the inexcusable 3 month delay in the installation of an extrusion line caused the division to slip into a loss position.

Going forward, the fact that the extrusion line is up and running in Canada should mean the North American division returns to profit which should drive overall profits up. Also as the lower oil price reduces prices of the Naphtha feedstock, the input prices should reduce, although in the UK higher taxes are expected to mean that energy costs increase. The forward PE of 9.6 does seem to undervalue this company but that £11M payment to the pension scheme should be taken into account and the forward dividend yield of 2.5% is fairly modest but nice to have.

On the 12th May the group released a trading update covering the first four months of the year. Volumes were ahead in the period due to increased silage stretchwrap reflecting new capacity. This resulted in the performance for the first four months being ahead of the same period last year. Less positive is the fact that in March a reduction of polyethylene imports from the Middle East coincided with a number of declarations of force majeure (the exact natures of which were not disclosed) by Western polymer producers which has caused the price to rebound to high levels with shortages in many grades. This volatility will likely continue until the holiday season when the subsequent reduced demand should allow supplies to get back in balance.

The group will pass these price increases through to the end users but margins are likely to be impacted in the short term while these increases are in the process of being passed through. Despite this, the successes with new products in the UK and Europe along with the recovery in the performance of the North American business means that the board are confident in the outcome for the year as a whole.

On the 3rd July the group reported that improved volumes continued into May and they currently anticipate that the performance for the first half will be slightly ahead of that achieved in 2014 despite the continued pressure on margins as they continue to pass through increases in raw material costs. It now looks as though the raw material price increases are running out of steam having reached record levels well above those in the Far East but in addition returns from the European business are being affected by the continued weakness in the Euro.

It seems as though the underlying progress of the group is good but they are being hit by things which are outside of their control. I feel it is probably sensible to wait for the interim results to get some further clarification on these current issues.

There bull run seems to have run out of steam a bit.