![]()

Laura Ashley have released their half year results for 2013. As usual I will start with the income statement.

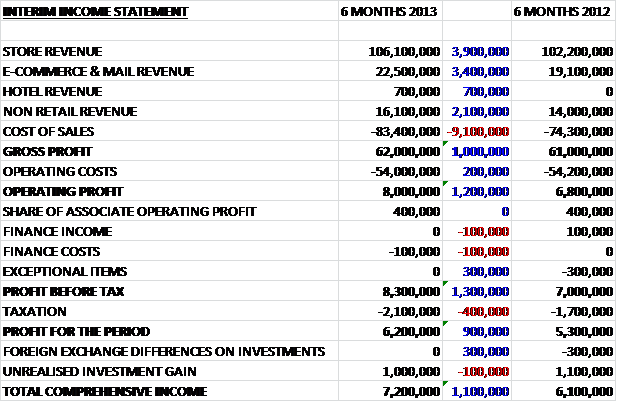

Income is up across all sectors, with e-commerce and non-retail doing particularly well. Geographically, revenues were up across all territories with the UK and non-Europe doing the best. Cost of sales were up slightly less to give a £1M increase in gross profit. There was not much change in Operating costs so operating profits for the half year were £1.2M higher at £8M. Tax increased slightly to leave the profit for the period £900K up at £6.2M.

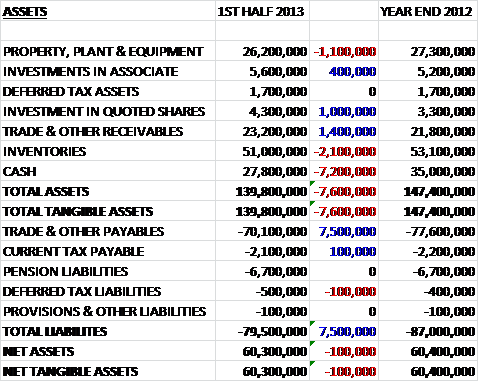

Since the end of last year, both assets and liabilities are down. The main assets to fall are inventories and cash, which was down £7.2M to £27.8M, which is a bit of a shame. The main change in liabilities was the decrease in Trade and Payables, down £7.5M to £70.1M so I guess we can see where that cash went. Overall this means that net tangible assets barely changed – down just £100K to £60.3M which is pretty good given the lack of debt.

On to the cash flow:

Although the group achieved £10.4M from profit, as we have already seen, £7.5M was spent on paying off some of those payables. This means the cash from operations was £3.6M. After Capital expenditure (less than last year) and tax (more than last year) was paid, there was a completely neutral cash flow. £7.3M was then paid out in dividends so the cash outflow for the half year was £7.2M. The cash flow of Laura Ashley has been a little disappointing of late. The situation seems to reverse somewhat in the second half of the year but even so, despite the substantial cash pile, this is not a sustainable situation.

Although by far the largest amount of revenue is obtained from the stores, non-retail now accounts for the biggest share of the profit – this includes the franchising and licencing sectors. The stores and the e-commerce accounted for the next highest share as margins fell in the retail side due to a high amount of discounting in the sales, and no profit has yet been made by the hotel.

During the year, UK store numbers stayed the same as the group concentrate on expanding sales from existing stores. E-commerce and mail order now account for nearly 18% of UK sales as rising e-commerce sales more than make up for lower mail order sales. During the first half of the year, an app was introduced to help the e-commerce side and a click and collect service will be introduced in the second half.

Within the UK sales, the sales of furniture decreased by 1.1%. This was rather disappointing but it did apparently outperform the market and achieved good online growth. Fashion sales were also down (1.2%) but again this outperformed the market and did well in knitwear, dresses and blouses. Sales of decorating products did much better, up 4.7% due to the fact that the group can respond quickly to differing trends due to the items being manufactures in the UK. Sales of home accessories did best of all, up 9% and showed significant growth in bed linen, lighting and gifts.

The refurbishment of the hotel the group purchased last year has commenced and it is due to be launched in the second half of the year – it will be interesting to see what the group intends to do with it. Franchising operations are increasing (as already mentioned non-retail accounted for the highest amount of profit during the first half of the year). Nearly 20 new franchised stores were opened, including two in Russia and some in Japan, Taiwan and Australia. The franchising operations make up the bulk of the non-retail revenue.

So what have we got here? Well revenues are certainly up across the board but the big growth areas are e-commerce and the overseas franchise operations and the increase in UK sales could be down to heavy promoting which seems to have hit margins slightly. Profit for the half year is up nearly £1M. The cash situation continues to be come cause for concern as £7.2M was lost in the half year. To some extent this is a cyclical trend but I am not sure the second half of the year will counteract it enough. Going forward, the group may concentrate on the franchising. There is no debt, which is clearly good and the dividend payout has been held and is still 7.4% which is a remarkable return in this market.

Overall, the cash flow is a bit of a concern but there is no debt and a stonking 7.4% dividend so I may try and buy some more.

On 14th December, Laura Ashley released a management statement. Total sales up to that point had increased 4.2% on the same period of last year. Within that, E-commerce continued to grow and was up over 22%, boosted by the new mobile site and increased overseas deliveries. The gross margin is likely to be lower than last year due to heavier discounting to maintain increased sales and the store portfolio has increased by 2. All in all, not a huge amount given away and this does not change my stance on the company.