![]()

Photo-Me have now released their half year results for 2013, I will start with the income statement.

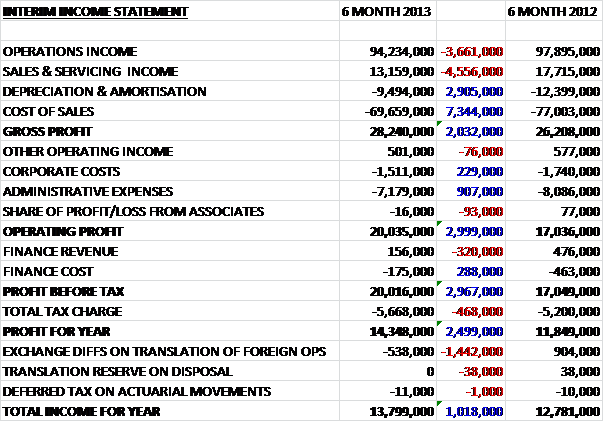

We can see that again, revenues have fallen. The operations revenue is down £3.7M to £94.2M, and the sales & servicing revenue has fallen even more drastically – down £4.6M to £13.2M. The cost of sales have fallen a similar amount, however, and this coupled with a lower depreciation bill ensured the gross profit was £2M higher. Admin expenses are also lower than last year so the operating profit is actually nearly £3M up, at £20M. The tax charge is slightly higher, as would be expected given the higher profit, which all means that the profit for the year was nearly £2.5M up at £14.3M. Unfavourable exchange rates pegged this back slightly, however, to leave the total income £1M up, at £13.8M. This is quite a respectable performance in my view.

Next, the statement of financial position.

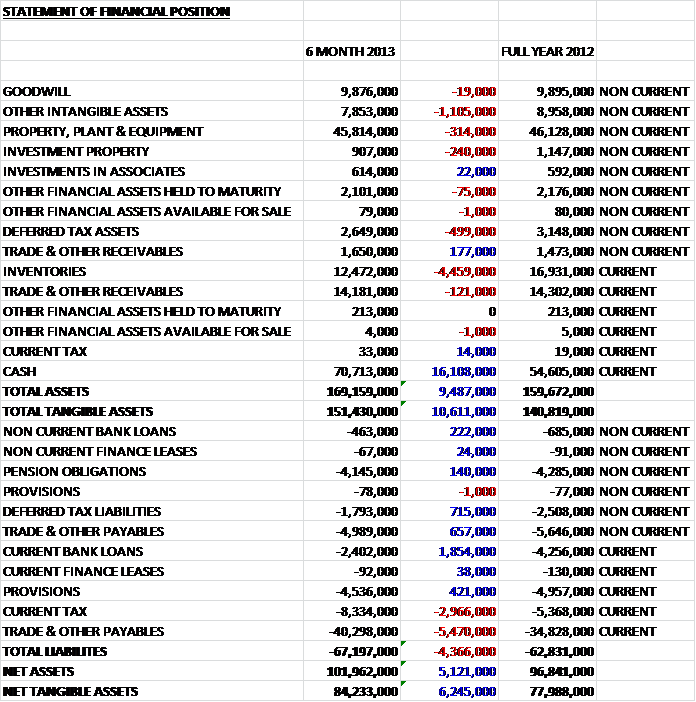

Overall we see that total assets are up by £9.5M to £169M. Pleasingly this rise is down to an increase in cash – up a whole £16.1M in just half a year! Most other assets are down on the end position of last year, with inventories being hit the hardest, down by £4.5M to £12.5M. The only other significant movement seems to be in intangible assets.

Total liabilities increased by £4.4M to £67.2M. This was due to a nearly £3M increase in the current tax liability (as the group makes more of a profit) and a £5.5M increase in payables which suggests the group may be ramping up trade somewhat (I am not sure exactly what payable have increased so this is a guess). Otherwise we see the group continuing to pay back debt, and there is now less than £3M in bank loan liabilities on the books.

All the above means that net tangible assets are up a respectable £6.3M in half a year to £84.2M.

Moving on to the cash flow:

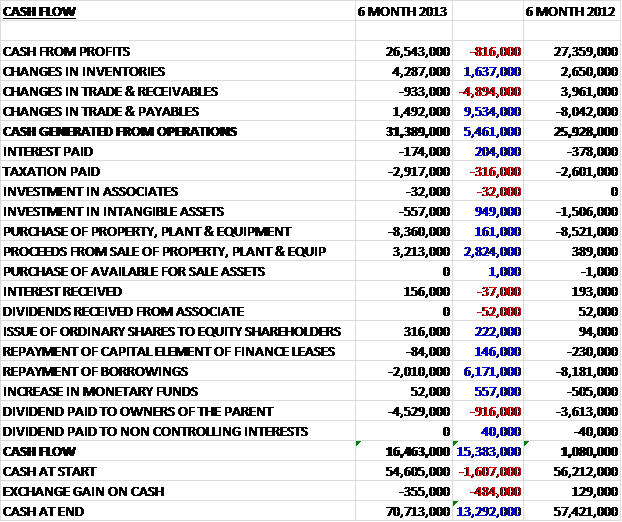

The bottom line here is the £16.5M cash flow for the half year, that is £15.4M more than last year and really an incredibly good performance. Cash generated from operations was £5.5M up, boosted by tying up less money in inventories and good control over payables (we have already seen payable liabilities are up). The group spent slightly more on capital expenditure than in the first six months of last year but benefited from the sale of a property, which netted £3.2M in cash. The property that was sold was the former home of the KIS division, which moved out of its premises in France as part of the restructuring of the division. The other main difference from last year is the fact that as the debt winds down, the group needs to pay less back and that is evident here as only £2M was spent on repaying bank loans (compared to £8M). Dividend payouts increased by just under £1M but still the group is able to achieve a very good cash inflow. No wonder the board are considering giving more back to shareholders and now there is a cash pile of over £70M which could hint at quite a substantial payout.

Photobooths make up the bulk of the profit for the Operations division and is a significant cash generator. The group is undergoing an expansion in Germany and is involved in a rollout of a newer design of Photobooths which are showing a 50% increase in turnover. The group are also targeting new markets for the Photobooths and has launched its first machine in Malaysia. They are also testing the market in Thailand and Ukraine and examining an entry into Turkey and Poland.

The big news in this update, however, is the announcement that the group is looking into stand-alone heavy duty laundry units after an extensive trial in France and Belgium showed that the units stood up durability wise and took enough money to make them viable. Utilising the same sites as the Photobooth units, there will be an aggressive rollout in France and Belgium, initially, before looking at other European markets. The average EBITDA of the units is apparently over 50% of turnover (but the exact figure is not stated) and costs should be reduced when the manufacture of the units moves from France to the Far East. The fact that the machines use the same current sites that the group has for the Photobooths and also uses the same service engineering network ensures that they can be offered at a competitive rate. The board predict that these machines should be a significant contributor to profits within three years.

Digital printing kiosks are focussed on France and Switzerland and they now include more value added items such as calendars, greeting cards and postcards, together with a scanner for photo replication. Trading for the printing kiosks was on a par with last year. The amusement and business service equipment struggled again, with small reductions in revenues recorded. It is planned that a single logistics and distribution platform for European operations will bring further cost savings.

The Sales and Servicing division has undergone substantial restructuring over the past couple of years and is now much smaller than it was. Over the past half year, revenues have reduced but profits are actually up when compared to the same period of last year. The market has remained difficult but the group has managed to deliver some Pocket book makers to Mitsubishi and Fuji. Sales of the new mini lab have been subdued by the ongoing weakness in the photographic printing marketplace.

The same risks remain from the full year report and the collapse of Jessops may have a detrimental effect on group revenues. The first half of the year is traditionally much stronger for profits so gives an indication as to the fortunes for the full year. This year, revenues have fallen but profits have increased. It does seem as though Photo-Me is now a much leaner, more profitable organisation than it was a few years ago. Debt has been pegged back substantially in the last two years and now that it is almost paid back, there is less need to spend cash on the repayments and this is the main driving factor for the hugely impressive cash inflow in the last six months. There was a one-off £3.2M cash gain from the sale of the old KIS building but even without this, the group would have made £13.3M in cash during the 6 months.

Looking forward, the move into laundry machines is an interesting one. Initially it doesn’t seem to entirely fit with the other offerings but there are overlaps and it is something that I will be watching closely in the near future. As long as the Photobooths continue to generate cash, it is an experiment that the group can afford to conduct without the need to take on new debt. Speaking of the Photobooths, the move into new markets is a good development and it is especially good to see the move into emerging markets such as Malaysia. There was absolutely no mention of any progress in China, however, which was a little disappointing.

On the current share price, the increase in dividend means that it is trading on a yield of 4.1%, which is actually pretty good, especially with the promise of further shareholder returns. Overall then, this has been a very positive update and if I didn’t already have quite a number of these shares I would look to buy more. In fact, I may do so anyway on any dips.

On 4th February, the group announced plans for the special dividend. A total of £11M will be distributed to shareholders, which works out at 3p per share. On today’s share price, that is a return of 4.5% so a very decent incentive in my view. The ex dividend date is 13th Feb.

On 8th March 2013, Photo Me released a statement covering the first three quarters of the year. In Q3, profitability was substantially better than in the same period of last year. In the first nine months of the year, revenues in the Operations division was very similar to that of last year but due to cost savings from lower manufacturing costs, profits are up on last year. Performance in Japan and Germany was particularly good. Going forward, further cost savings due to the central logistics platform in Europe should show benefits next year and onwards. The new Starck photobooths are delivering improved returns and the new laundry machines have started to be delivered.

Sales and Servicing suffered reduced revenues in the period but due to the restructuring, it is no longer loss making. Cash generation of the group is still good and shareholders have now benefited from the special dividend announced in the last update. So far, this is a very good update but the only cloud attached to this large silver lining is the adverse affect of currency movements. This will apparently have the effect of reducing pre-tax profits by 8% so it is testament to the good progress being made that management still expect to hit market expectations for the year. Overall, this is still a very good stock to own and the share price has come on very well since the last update and now looks about right to me – a strong hold.