Portmeirion has now released its interim results for the year ending 2015.

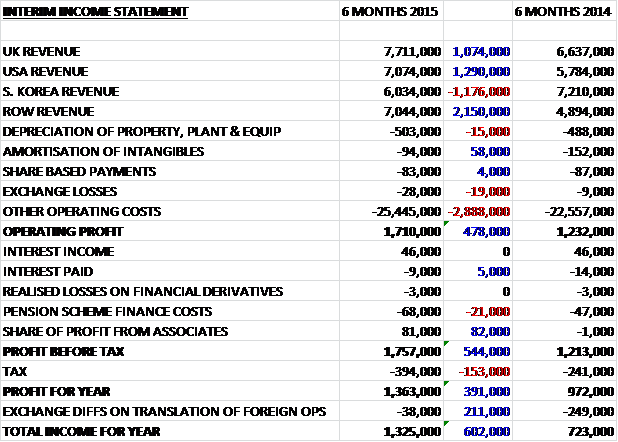

Overall revenues increased when compared to last year as a £1.2M fall in Korean sales was more than offset by a £1.1M increase in UK revenue, a £1.3M growth in US revenue and a stonking £2.2M increase in ROW revenue. Operating costs also increased during the period to give an operating profit some £478K ahead of the first half of last year. The group also made a small profit via the associate, presumably from Canada, but a larger tax bill offset this and meant the profit for the half year was £1.4M, an increase of nearly £400K year on year.

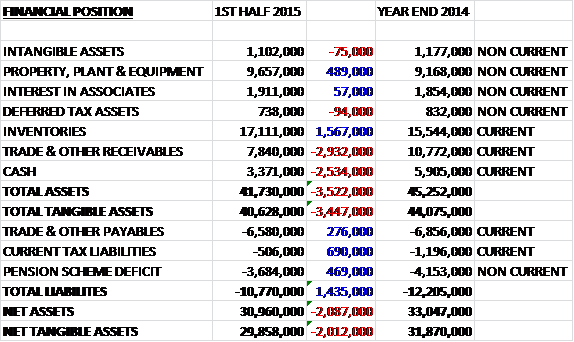

When compared to the end point of last year, total assets fell by £3.4M driven by a £2.9M decline in receivables, and a £2.5M fall in cash partially offset by a £1.6M increase in inventories and a £489K growth in the value of property, plant and equipment. Total liabilities also fell during the period due to a £690K decline in current tax liabilities, a £469K decrease in the pension deficit and a £276K fall in payables. The end result is a net tangible asset level of £30M, a fall of £2M over the past six months.

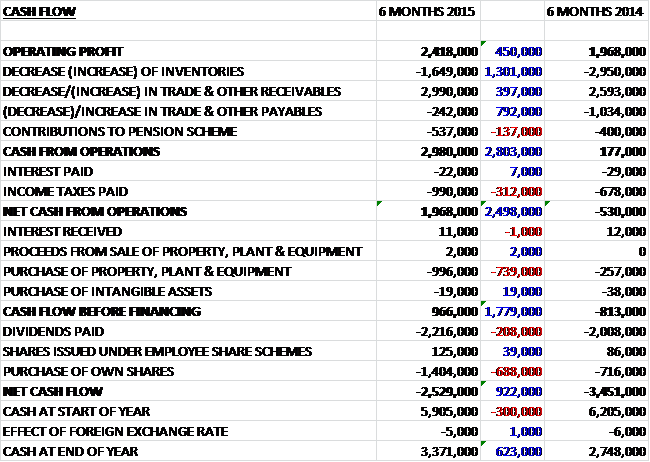

Before movements in working capital, cash profits increased by £450K to £2.4M and this was boosted further by a fall in receivables, partially offset by higher tax and higher contributions to the pension scheme so that net cash from operations came in at just under £2M, an improvement of £2.5M year on year. The group then spent nearly £1M on capex to give a free cash flow of £966K, which didn’t cover the £1.4M spent on share purchases or the £2.2M spent on dividends so that the cash outflow for the period stood at £2.5M with a cash level at the end of the half year of £3.4M. It must be pointed out, however, that the cash income is very much skewed to the second half of the year.

US sales increased by 12% in local currency and by 22% when translated into sterling as the recovery seen at the full year stage continued. In the UK, sales increased by 16% and direct online sales into the two countries increased by 43% year on year. After fifteen years of growth, the South Korean market contracted during the period, falling by 16%. This was caused by economic conditions in the country toughening but management are confident of long the long term prospects there. Elsewhere, India has once again performed strongly, with revenues increasing by 58%.

The major capital expenditure on production capacity expansion announced earlier in the year has already absorbed £1M and the total capital expenditure for the year will be about double this. The total cost of the expenditure at the Stoke plant will be £1.5M and includes a new continuous tunnel kiln. Work is well underway and running to schedule with an anticipated kiln commissioning date in Q4 2015. In the mean-time the group has continued to grow production incrementally, averaging weekly production of over 150,000 pieces, some 5% ahead of the same period of last year.

The group has continued to extend their existing patterns and to develop new patterns for all of their markets. Within Portmeirion they have Alfresco Pomona, in Spode they have variations on the Delamere patterns, including Bouquet, Lakeside and Rural. The new Ted Baker ranges have been well received around the world.

There is still no final resolution of the anti-dumping duty imposed on the group by the EU in 2012. They continue to pursue the matter through the legal processes but is so far cost the group a cumulative £1.7M

The results of the group are always significantly weighted to the second half due to Christmas sales but the board remain confident for the full year but the board remain confident for the future and the strategy remains unchanged. After an 11% increase in the interim dividend, at the current share price the shares yield 3%, increasing to 3.1% on the full year consensus which is fairly decent. The net cash position at the period end was £3.4M, compared to £2.7M at the same point of last year.

Overall then, this seems like another period of strong performance from the group. Profits increased, as did operating cash flow and the group produced a decent amount of free cash, although this did not cover the dividends. The results are always heavily weighted to the second half due to Christmas so this kind of cash flow is probably to be expected in the first half. Operationally, the US, the UK and India all did well but the performance in South Korea suffered somewhat, which is a potential cause for concern given the importance of that market. The anti-dumping issues continue, I suppose Portmeirion must be importing its china from overseas, probably China but this is guess work as there is no further detail provided in what is an update that is a bit thin to be honest.

Another potential banana skin is the commissioning of the new kiln and any potential delays, although that seems to be progressing on target at the moment. The yield of 3% is decent enough and I am sorely tempted to buy shares here.

Risks: New kiln teething issues, slowdown in Korea.

Opportunities: Greater capacity from 2016, Indian sales, resolution of the anti-dumping issues.

It does seem as though there has been some weakness recently – could be a good buying opportunity?

On the 18th January the group released a trading update for the year where they stated that they expect pre-tax profit to be slightly ahead of market expectations. Revenues are expected to be over £68M, an increase of at least 11% year on year although they have benefited from the strong US dollar and at a constant exchange rate the increase would have been 8%. The new kiln was installed and commissioned during the year within budget and in time without any disruption to existing production. It will be brought into live production from the start of February to meet expected demand for UK manufactured product in 2016. Sales in the UK were particularly robust through the year with strong growth in online sales with the US performing well in the run up to Christmas.

Overall, this is a good positive update.