Portmeirion is listed on AIM and is a market leader in high quality tableware, cookware, giftware and table top accessories based in Stoke. There is also a showroom and office in New York along with warehouses in Connecticut and Guangdong in China. Products are sold directly to customers in the group’s own shops in the UK, via the internet, through a network of distributors throughout the world and directly to retailers. They also gain some royalty income from the IP imbedded in their brands, patterns and designs. The factory in Stoke does not produce bone china or porcelain which are different clay mixes and require different firing temperatures so they manufacture just under half of their products themselves, sourcing the rest externally.

There are four main brands within the group. Portmeirion has designs that apparently sit comfortably with everyday life with its best-selling brand being the Botanic Garden Range. Spode is renowned for its rich heritage and includes British designs such as Blue Italian, Blue Room and Christmas Tree. Royal Worcester has a rich and diverse design heritage, offering a wide spectrum of products from fine bone china mugs and sophisticated tableware sets to the opulent Painted Fruit Collection. Pimpernel is a brand covering placements, coasters, trays and accessories.

The associates are Furlong Mills, a supplier of clay and glaze, of whom the group owns 28% and Portmeirion Canada who markets and distributes the group’s products in Canada, with a 50% ownership.

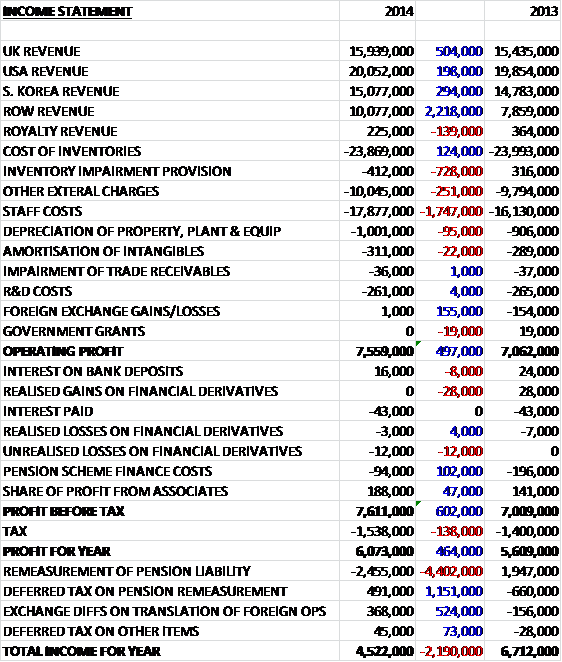

Overall revenues increased year on year as slightly lower royalty revenues were offset by increases in all the other segments, with a particularly large increase in ROW sales driven by growth in sales to India. We then see staff costs increase by £1.7M and a £700K negative swing relating to the inventory impairment provision which was partially offset by a £155K positive swing in foreign exchange to give an operating profit nearly £500K more than last year. There was also the lack of £28K in realised gains on financial derivatives that occurred last year but the pension scheme finance costs fell by £102K year on year and there was a £47K increase in the profit from associates to give a profit for the year of £6.1M, an increase of £464K year on year.

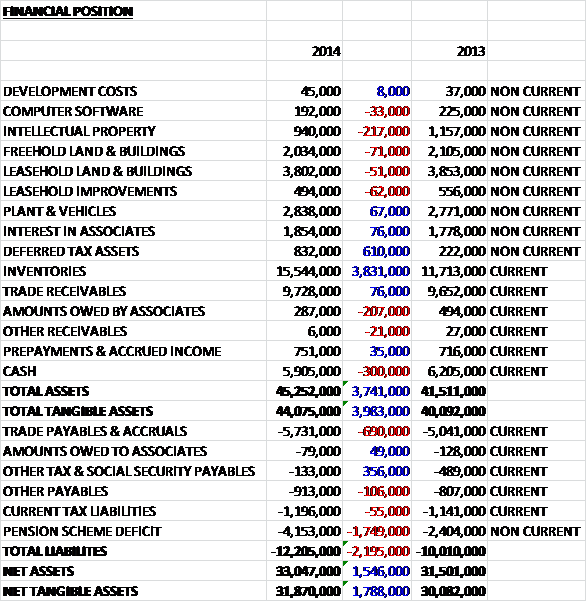

When compared to the end point of last year, total assets increased by £3.7M, driven by a £3.8M increase in inventories and a £610K growth in deferred tax assets, partially offset by a £300K fall in cash. Liabilities also increased during the year as a £1.7M increase in the pension deficit and a £690K growth in trade payables was partially offset by a £356K fall in other tax and social security payables. There is also £4M-worth of operating leases outstanding off the balance sheet, but that isn’t particularly material.

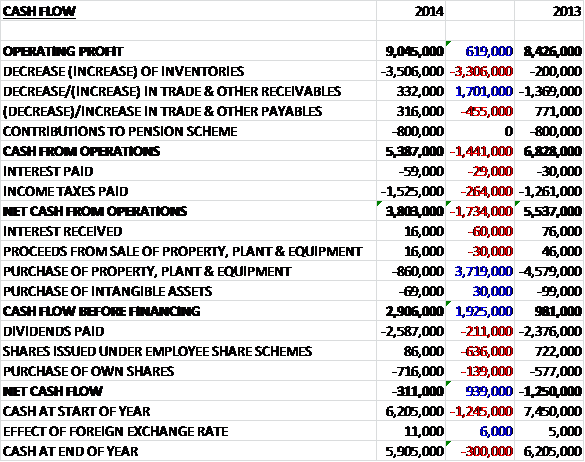

Before movements in working capital, cash profits increased by £619K to £9M. After a large increase in inventories (which is now a focus for management to reduce), however, and a smaller increase in tax paid, the net cash from operations stood at £3.8M, a decline of £1.7M year on year. The group then paid £860K for property, plant and equipment along with £69K on intangible assets to give a decent cash flow before financing, the bulk of which was spent on dividends with a further £716K going on share purchases for the employee share schemes. The end result is a net cash outflow of £311K for the year to give a cash level of £5.9M at the year-end.

Operating profit in the UK division was £6.6M, a reduction of £100K when compared to last year with sales to South Korea increasing by 2% and sales to the rest of the world up 25% with India growing by 84% to become the group’s fourth largest market. The operating profit in the US division was £994K, an increase of £678K year on year as better rates of employment and lower fuel costs continued to improve prospects in the company’s biggest market.

Sales of the best-selling Botanic Garden collection were over £28M and it remains at the heart of the group’s future prosperity. Spode Christmas Tree is the second best seller, its main market is the US where is sells in excess of $10M per annum. The initial responses to the Ted Baker tableware patterns are encouraging and management has high hopes for it during the coming year.

Online sales, principally to UK and US customers, hit £2M which represents a 73% increase year on year. US online sales increased by 178% after commencing in the second half of 2013 while UK online sales increased by 36% with no sign of slow-down in this route to market. During the year the online capabilities were expanded into Austria, Belgium, France, Germany, Ireland, Luxembourg, the Netherlands, Spain and Portugal.

As well as nudging against manufacturing inefficiencies due to being close to capacity (the group makes just under half of its own products), they also suffered from the imposition of anti-dumping duty in Europe which has cost the business about £800K. Another area of potential concern is carbon tax measures and energy costs. Energy costs are a major item of expenditure for the group but recent energy pricing has moved favourably which meant that despite a 16% increase in sales of own manufactured products, energy costs only increased by 2.6% year on year. Finally, another risk to the group is clearly economic conditions, particularly in the UK, the US and South Korea, although increasingly other markets are also becoming important such as India.

In the Portmeirion brand, next year is to host two new collections in collaboration with Ted Baker. The Rosie Lee collection is a comprehensive tableware range featuring pretty florals and is hand gilded with 22 carat gold. Ted Baker’s signature prints are also threaded into the Casual Collection. The Sophie Conran range has been refreshed with a new collection, Sophie Blue which is inspired by traditional English spongeware techniques and features surface patterns in a deep blue colourway set on the rippled silhouette. A new colour, “pebble”, also joins the range alongside white and glass line extensions.

In the Spode brand, Winter Scene joined the portfolio during the year. It is an interpretation of classic Spode artwork prints with a red border of holly leaves and acorns adorning each item in the tableware collection with key pieces featuring a winter’s day scene. Christmas Tree continues to be a best-selling festive pattern with new product introductions ensuring its popularity. Delamere Rural is showing strength and a number of new items being made at the Stoke factory are being added to the range.

In the Royal Worcester brand, the Wrendale Design’s licensed collection has proved very successful since its launch in 2013 and building on this popularity, new characters designed by Hannah Dale joined the fine bone china mug collection in 2015 including a dog, cat, pig and rabbit. A new giftware collection featuring a variety of the animal illustrations has also been introduced including a tea-for-one set and egg cups. The winning design from the group’s competition will make its debut in 2015. Inspired by the Stoke on Trent skyline (!), the design includes pinks, blues and oranges and features hot air balloons floating over an industrial landscape.

In the Pimpernel brand, the placemat and coaster portfolio has been extended to include three new designs in 2015. The seaside inspired Coastal Signs placements and coasters feature rugged seashores and maritime resorts whilst the Puppy Club and Kitty Club coaster sets feature sepia images of cats and dogs. New additions to the Wrendale Designs collection include round placemats, coasters and worktop savers that complement this licensed range.

Following a strategic review of the UK manufacturing site in Stoke, in response to the increased demand for UK made product, the board has approved a £1.5M investment in a new glost kiln and other equipment that will increase the capacity of the UK factory by over 50%. To meet demand from a number of export markets, including the US, South Korea, India and the Far East, production output was increased by 17% in 2014 to 150,000 pieces per week. Forecasts show sufficient growth in demand over the coming years warrant expansion with some 250,000 pieces per week being targeted.

The group does have one large customer in South Korea which accounts for about 23% of sales – presumably a distributor. If something were to happen to them, there could be an issue finding a replacement. The UK defined benefit pension scheme was closed to new entrants and future accruals back in 1999 but it is still causing a few problems. The scheme currently has a deficit of £4.2M on assets of £28.3M which is a shame given how long it has been closed but not particularly alarming. The group is expected to pay £937K into the scheme in the coming year which is a bit of a drag on cash flows. The group uses forward contracts to mitigate foreign currency movements, with the US dollar being the most important but a 10% change in any currency against sterling does not look as though it would have a material effect.

At the year-end the group had entered into contractual commitments of £699K. The group seems to have plenty of debt headroom. There is a £2M overdraft facility available at an interest rate of 2.25% and a £2M revolving credit facility with an interest rate of 2.3%. At the year end, neither of these were being used but it is worth noting the working capital movements throughout the year, with a build as the group enters the Christmas period.

Trading in the first two months of the new year is ahead of the same period of 2014 but sales have become increasingly second half weighted so the more important trading comes later in the year. In any event, management are confident for the short and long term.

At the current share price the shares trade on a PE ratio of 15.8, falling to 14.7 on next year’s forecast which seems sensible. After a 10% increase in the total dividend being paid, the shares are yielding 2.9%, growing to 3.1% on next year’s forecast which again seems fine. The group considers that a two times cover is appropriate for the dividend.

Overall then this was a good update for the group. Profits increased, as did net assets and although the operating cash flow fell, this was due to a build in inventories which management are looking to address and the underlying cash profits increased year on year. This was driven by a great performance in the US as the economy there improved. Profits in the UK actually fell and frustratingly the reason for this is not actually explained anywhere. Perhaps they encountered some inefficiencies as the Stoke plant performed close to capacity. The £1.5M being spent on a new kiln looks necessary given the capacity constraints and being able to make 250,000 pieces a week would be very good – the investment looks modest given the benefits.

Online sales continue to romp ahead and new websites have been opened in some European countries, although the EU anti-dumping fines of £800K look perplexing – some more background to this would have been helpful. There are plenty new designs coming in, with Ted Baker looking very interesting – a quick look on the website shows the Rosie Lee collection in particular to look interesting and modern. The group also seem to have the license for Peppa Pig which one would have thought enjoys some decent sales. In all, the PE ration probably looks about right but I may look to enter on weakness.