GVC has now released its interim results for the year ending 2015.

When compared to the first half of last year, sports NGR increased by €2.8M and gaming NGR grew by €13M and after variable costs, the gross profit came in some €8.7M higher than last time. We then see various other costs increasing year on year with a €1.4M growth in technology costs, a €443K increase in professional fees and a €792K increase in other personnel costs. The incentive scheme costs increased by €2M to a frankly incredible €8.1M and we also see an €846K increase in foreign exchange losses. We also see some non-underlying expenses as the €1.6M cost relating to the Betit put option last year was more than offset by a €3.8M charge relating to costs that have arisen so far on the proposed takeover of Bwin and a £915K charge for Romanian back tax and license fees. All this gives an operating profit of €18.4M, a decline of €493K. As far as finance costs are concerned, a €373K unwinding of the discount on the deferred consideration was more than counteracted by an €804K detrimental movement in foreign exchange revaluation relating to the conversion of the William Hill loan from GBP into Euros along with the retranslations of finance lease payments and share option cash-out liabilities, so that after tax, the profit for the half year stood at €16.7M, a fall of €827K year on year.

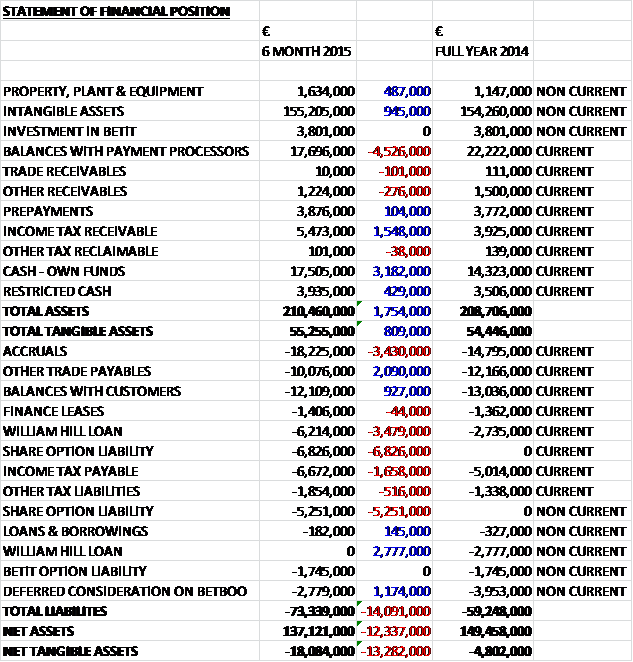

When compared to the end point of last year, total assets increased by €1.8M driven by a €3.2M growth in cash, a €1.5M increase in income tax receivable and a €945K increase in intangible assets, partially offset by a €4.5M fall in balances with payment processors. Total liabilities also increased as an incredible €12.1M share option liability, a €3.4M increase in accruals and a €1.7M growth in income tax payable was partially offset by a €2.1M fall in trade payables, a €1.2M decline in Betboo deferred consideration and a €927K decrease in balances with customers. The end result is a €13.3M fall in net tangible assets to a negative €18.1M.

The group made €26M of cash from operations, which is an increase of €4.5M when compared to the first half of last year. They then spent €1.2M on earn-out payments from the Betboo acquisition, €2.6M on internally generated software and €407K on property, plant and equipment to give a free cash flow of €21.7M, an increase of €7.3M year on year. The bulk of this was spent on dividends and there was also €948K spent on finance lease payments to give a cash flow of €3.6M for the half year period and a cash level of €21.4M at the end of the period.

In the first half of the year, the value of sports wagers came in at €823.7M compared to €769.2M in the first half of last year. The sport margin has declined from 9.7% to 8.8%, however with Q2 even lower at 8.7% so that the sports NGR was just €2.8M ahead at €54.8M. This increase was driven by Q1 NGR and the NGR in Q2 was actually below that of Q2 last year and was the lowest quarterly total for over a year, which is a bit of a concerning development. The Gaming NGR seemed to be much more healthy, however, and in contrast to sports NGR, the figure for Q2 was the highest in over a year and some €7.1M above that of Q2 last year and €3.6M higher than Q1 this year. Of the sports gross gaming revenue, in-play now amounts to 73% compared to 63% at this point of last year, and mobile represents about 38% compared to 22% during the first half of last year.

As can be seen, there were two exceptional items during the period. There were professional fees of €3.8M that have been incurred since May after the group announced the proposed acquisition of Bwin party. As this is still ongoing, there will presumably be more of these professional fees in the second half of the year. These costs relate to due diligence, synergy reviews, tax planning and extensive legal workstreams. It is anticipated that an acquisition of Bwin would be accompanied by a move from AIM to the main market at the time of completion.

The other item was a €915K charge for Romanian back tax and license fees. The group is making an application to be licensed in the country and under the licencing regime enacted, companies that have in the past operated there are obligated to make a “tax amnesty” settlement should they wish to be considered for a new license. The group has therefore made a provision for these back tax costs. The underlying tax impact of being licensed in Romania is likely to be about €500K. There was also the imposition of the UK point of consumption tax of 15% in the UK on sports GGR and 15% of Gaming NGR along with German VAT of 19% on certain aspects of gaming revenues.

As can be seen, there is now a huge new liability relating to share based payments. These relate to cash payments paid to each director over a period of two years and the director’s dividend bonuses derived from the share options that will decrease in a straight-line over the two year period of the retention plan. The total liability is a very considerable €12.1M. The group is still paying off the William Hill loan and the second instalment of £2.3M is repayable in December with the final instalment of £2.3M being repayable in June next year.

The group has made a restatement of €1.6M to the income statement last year and added it as a cost of valuing the Betit put option. This represents the recognition of the fair value of the put and call options to acquire the balance of the outstanding shares associated with Betit. At the time of the 2014 interim statement, the fair value exercise had not been completed which makes me wonder if perhaps it would have been more suitable to just recognised the cost when it was calculated rather than restate previous statements.

After the end of the period, the group received notice that 37 Entertainment Inc, a company incorporated in Canada, had files legal proceedings against GVC which the group intends to “robustly contest”.

After experiencing softening in the Greek market following the economic problems in the country, the group is now experiencing signs of greater customer activity. They remain confident on the future prospects of the Greek market which will continue to be important. Current trading for the group as a whole remains strong, even with the absence of the World Cup this year. Management are highly confident for the rest of the year. At the current share price the shares a yielding 9.6% on a rolling annual basis.

So, this seems to have been another period of decent performance. Profit did fall year on year but this was entirely due to the costs relating to the proposed Bwin takeover and operational cash flow improved during the period to give rise to plenty of free cash. The balance sheet is not looking so good, however, with net tangible assets down by €13.3M due to the share option liabilities. Indeed, these figures really lay bare exactly how much management is rewarding themselves with these options which are very excessive in my view. Operationally, the falling sports book margin is a little concerning but this is being made up for by increasing profits from the gaming side of the business. The dividend yield remains a major incentive but the real issue at the moment is the potential Bwin acquisition – there seems to be a bit of a bidding war going on so the concern has to be whether GVC end up overpaying for Bwin or miss out on the acquisition entirely.

GVC has now announced that they have reached an agreement on the terms of a recommended offer where GVC acquires Bwin.party. As part of the deal, GVC shares will transfer from AIM to the main market and if the offer becomes effective it will result in the issue of about 195,288,073 new GVC shares to Bwin shareholders which would result in former Bwin shareholders holding about 66.6% of the enlarged group.

The group intends to integrate its own and Bwin’s operations with restructuring steps including the migration of the GVC sportsbook onto the bwin.party platform and in the 18 months after completion, GVC will take the following actions to improve the profitability in the sportsbook, casino and poker businesses:

After the integration onto the bwin platform, GVC’s existing sportsbook platform will cease operations, generating substantial cost savings in the form of lower technology costs, reduced staff costs and other associated efficiencies. The directors also believe that there opportunities to substantially improve the financial performance of the bwin.party sportsbook by a greater use of CRM systems to realise value from the large historical investment in the bwin and Sportingbet brands by cross-selling; building a best in class trading and risk team from the combined teams; investment in technology, systems and product development, the addition of more third party casino content, focused investment in those projects and marketing programmes which have measurable return on investment and termination of all sponsorship programmes, and more efficient operation of the customer services, IT and marketing functions.

The directors will consider expanding into certain markets in parts of Asia and Africa where the bwin brand is well known due to its association with a number of internationally recognised football brands.

The group believes that there are also opportunities to improve the financial performance of the casino and poker operations. They believe that there are opportunities to significantly reduce costs at bwin’s casino operation by applying the same principles as with the acquired sportsbook. The majority of bwin’s bingo activities operate on a third-party platform and so require little or no investment in terms of product development, although the group intends to ensure that its bingo product continues to evolve and remain competitive. Poker is bwin’s leas profitable gaming business and has declined in terms of NGR in recent years. The group intends to continue the steps already taken by bwin to stabilise and improve its poker performance and integrate the GVC poker operations into bwin’s poker platform.

The group has identified gross cost savings from integrating and restructuring the sportsbooks and integration of other operations of at least €125M per annum before any negative synergies such as an increase in customer attrition from the restructuring. Some cost synergies include staff, outsourcing and other people-related costs with efficiencies to be derived from removing duplication and by operating a more streamlined sportsbook; sponsorship and marketing cost efficiencies by eliminating marketing which as a low return on investment; IT and development efficiencies by migrating the sportsbook, reducing the number of development programmes, focusing on platform stability and reducing the amount of time that the technology systems were not available to customers; and back office and facility related savings by integrating systems and teams, re-organising finance functions and implementing changes to board incentives.

The delivery of these cost savings is likely to give rise to approximately €60M in one-off costs which would be incurred in the first 18 months after the acquisition. By applying its cash management capabilities to the integrated sportsbook activities, the group believes that by the start of 2017, the restructuring would drive substantial improvement in cash flows from operations and free cash flow enabling the prompt repayment of the Cerberus loan and the resumption of payment of dividends at a level which is comparable to the group’s quoted peer group of online gaming companies.

Bwin is licensed and regulated in Gibraltar and also has licenses in Alderney, Austria, Belgium, France, Italy, Denmark, Germany, Malta, Spain, the UK and the necessary approvals to operate in New Jersey in the US. It generated EBITDA of €101.2M last year and has a leading position in each of its four key products: online sports betting, casino and games, poker and bingo with brands including bwin, party poker, party casino and Foxy Bingo.

In all, GVC have offered 25p in cash plus 0.231 new GVC shares for each bwin.party share, implying a headline value of about 129.64p per bwin share. It is proposed that current bwin CEO Norbert Teufelberger will join the board as a non-executive director.

The group is also proposing to raise about €206M by way of a placing of 27,978,812 shares to certain new and existing institutional investors are a placing price of 422p per share and the subscription of 7,566,212 new shares by certain investors at a price of 422p per share. Certain GVC directors will also participate in the fundraising. The net proceeds of the placings will be used to fun reorganisation costs within the enlarged group and for general working capital purposes, they will not be used for the cash consideration relating to the offer.

In addition, the existing contractual bonus arrangements for the GVC board are cancelled from 2016 onwards and the existing awards held under the 2010 LTIP will be cash cancelled on completion. The existing bonus retention plan, announced in March, will be accelerated and paid on completion and transaction bonuses will be paid to the board on completion. The directors will reinvest these proceeds (estimated to be about £10.9M) in subscribing for new shares as part of the fundraising with will have a year-long lock-up arrangement. I have to say that despite the fact the proceeds will be invested back into the company, the acceleration of that disgraceful bonus plan leaves a rather sour taste in my mouth and seems rather greedy to me. At least the new employee share scheme will be market value options.

The cash consideration of the offer will be funded by €400M of senior secured debt provided by Cerberus which is a two year secured facility that bears interest at EURIBOR + margin 11.5%, which seems pretty expensive to me.

In all, this is clearly a transformational deal for the group and if GVC can pull it off quickly there should be great rewards. This is not without risk, however, and with the added uncertainty plus the lack of dividends for the foreseeable (despite earlier assurances that any acquisitions would not affect shareholder returns), I have decided to sell out here. These shares have made me a lot of money so I may look to re-enter at a later point.

On the 8th October the group released an update covering Q3 trading. After the latest quarterly dividend of 14c was announced, the yield for the first nine months of the year is 9.8% but as this is going to be the last dividend payment this year, we can take this as the yield for the year. NGR for the nine month period was 11% higher than last year averaging €670K per day with gaming NGR up 18% to €356K on customer deposits that grew by 14% to €1.7M per day.

Sports wagers in the period grew to an average of €4.5M per day compared to €3.9M per day last year but sports NGR only increased by 3% to €314K due to the sports margin falling from 10.1% to 9.2%. The board is apparently very confident of the outlook for the rest of the year.

On the 30th November the group announced the appointment of Shay Segev to the newly created role of COO. He is the former COO of Playtech and is an expert of technology and products for the online gaming industry. He is currently Chief Strategy Officer for Gala Coral, developing the company’s Onmi-channel growth strategy and it is expected that he will join GVC, initially on a non-board basis, in March 2016. This certainly seems like a quality appointment to me but not sure why he is not joining the board in March.

On the 4th December the group released a trading update for the first two months of Q4. Net gaming revenue was 11.7% higher than the same period in 2014, sports wagers grew by 12.7% to an average of €4.9M per day, a gross win margin of 9.3% was achieved in sports during the period compared to 8.7% last year, and customer deposits rose by 8.3%. The board remain highly confident of the outlook for the rest of the year. This is no doubt a great performance and the reason for the update becomes clear as the EGM is taking place on the 15th December to approve the proposed acquisition of Bwin so I am sure that will have more of an effect on the share price than these great numbers.

On the 11th January the group released a trading update covering Q4 and the full year. During the quarter, sports wagers were up by 13.6% to €4,959 per day and sports margin edged up to 9.1% which gave a sports NGR of €320K per day, a growth of 5.6%. Gaming NGR was up 13.9% to €392K per day to give a total NGR of €712K, up by 10%. The constant currency figures were even better as the group was affected by the depreciation of the Brazilian and Turkish currencies so that on a constant currency basis, total NGR was up 21.3%. This is clearly an excellent set of results for the group but proceedings are now dominated by the acquisition of Bwin Party.

On the 2nd February the group, following its admission to the official list, the group announced the appointment of two non-executive directors. Stephen Morana spent ten years as part of the management team at Betfair, having served as both CFO and interim CEO. He is currently the CFO of Zoopla which he joined before its IPO. Peter Isola is an expert in gaming law and regulation. He currently holds non-executive directorships at numerous Gibraltar companies and since 2007 he has been a Senior Partner at Isolas in Gibraltar.

On the 3rd February the group announced the grant of options under the LTIP. CEO Kenneth Alexander was granted an option over 8,798,075 shares with an exercise price of £4.22 per share; CFO Richard Cooper was granted an option over 4,399,037 with an exercise price of £4.22 per share; and Chairman Lee Feldman was granted an option over 4,399,037 shares with an exercise price of £4.67 per share. The higher exercise price for Lee’s shares are due to US law and just so he doesn’t miss out the company has agreed to pay him a cash bonus of nearly £2M (being the difference between £4.22 and £4.67 for that many shares), although he does have to invest half of these proceeds in new shares.

The options will vest subject to the satisfaction of a performance condition whereby total shareholder return is more than the median of the FTSE 250. Also, non-executive director Norbert Teufelberger was granted an option over 200,000 shares with an exercise price of £4.22 per share. These will not be subject to a performance condition so this is free money at the current share price.

I suppose this could have been worse – the performance conditions are helpful if not exactly taxing but this is a huge amount of shares that are being given away. In particular the chairman seems to be getting a lot, especially considering his cash bonus…

On the 9th February the group announced that non-executive director Norbert Teufelberger has sold 460,000 shares at a value of £2.3M. This is not exactly a vote of confidence but he retains 2,755,264 shares – I wonder if he will look to offload some more.

On the 22nd March the group announced the appointment of Liron Snir to the newly created role of Chief Product Officer who will be overseeing product management and the overall user experience. Liron is the former President of Product Strategy at Playtech and seems to be a good appointment to me.

On the 22nd March the group announced the appointment of Liron Snir to the newly created role of Chief Product Officer who will be overseeing product management and the overall user experience. Liron is the former President of Product Strategy at Playtech and seems to be a good appointment to me.