BPI has now released its interim results for the year ending 2015.

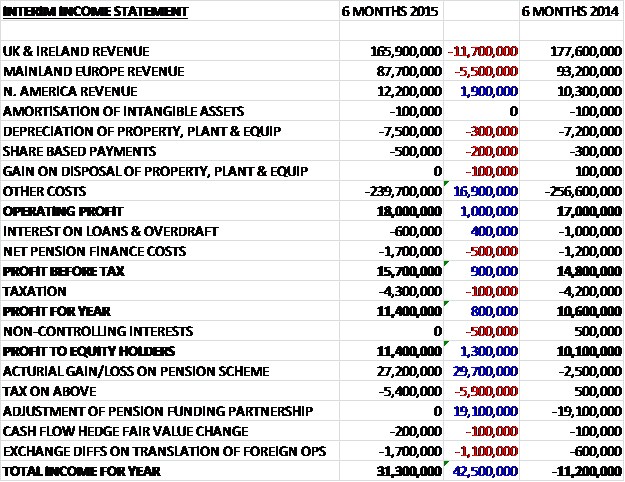

Overall revenues fell when compared to the first half of last year as a £1.9M increase in North American revenue was more than offset by an £11.7M fall in UK revenue and a £5.5M decline in European revenue. There was also a fall in costs, however, to give an operating profit some £1M above that of the first half of last year. After an increase in pension finance costs was nearly offset by a decline in the interest on the loan and tax was slightly higher, the profit for the year came in at £11.4M, an increase of £1.3M year on year.

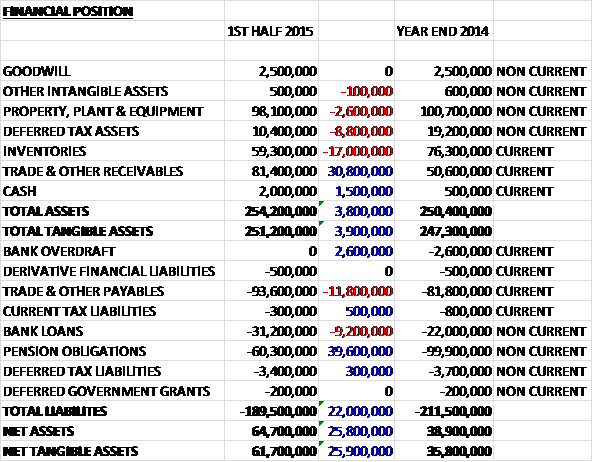

When compared to the end point of last year, total assets increased by £3.8M driven by a £30.8M growth in trade and other receivables and a £1.5M increase in cash, partially offset by a £17M fall in inventories, an £8.8M decline in deferred tax assets as the value of the pension deficit fell and a £2.6M decline in property, plant and equipment. Liabilities fell during the year as a £39.6M decline in pension liabilities and a £2.6M fall in the bank overdraft was partially offset by an £11.8M increase in payables and a £9.2M growth in bank loans. The end result is a net tangible asset level of £61.7M, an increase of £25.9M when compared to the end of 2014.

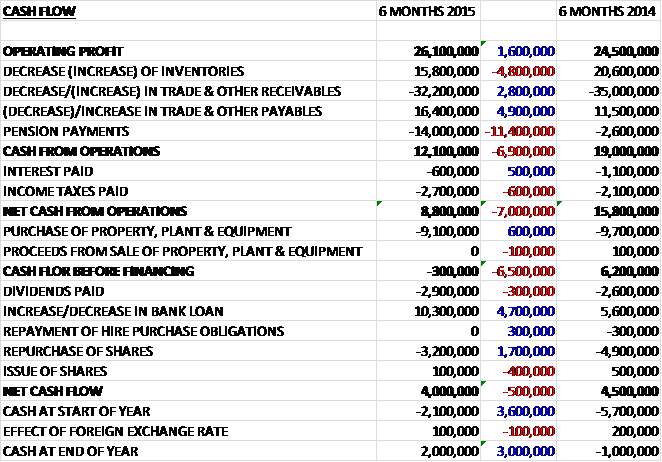

Before movements in working capital, cash profits were £26.1M, an increase of £1.6M year on year. An increase in payables and a fall in inventories were broadly offset by an increase in receivables but the £14M paid towards the pension plus a slightly higher tax payment meant that net cash from operations came in at £8.8M, a fall of £7M. The group then spent £9.1M on capital expenditure so there was no free cash during the period in which to pay the £2.9M of dividends or the £3.2M spent on acquiring shares for the incentive scheme so the group took out £10.3M of new loans to leave a cash inflow of £4M and a cash level of £2M at the end of the first half.

Operating profit at the UK and Irish division was £7.6M, an increase of £100K year on year. Volumes sold reduced as the group shipped less product to the site in Canada and exited some very low margin retail refuse sack business which was offset by some growth in plain films and silage stretchwrap. Volumes in the plain films sector increased but margins suffered from the polymer price increases. The policy of upgrading the extrusion lines at the Bromborough site has continued with three new lines fully operational. An additional five layer coextrusion line has been ordered for delivery in early 2016.

Silage stretch volumes increased despite a slow start to the season due to the cold weather in Northern Europe. As with other products, though, margins were lower due to the polymer price increases and the impact of exchange rates on export volumes. Operational improvements continued at Leominster and a seven layer line has been ordered for delivery in 2016. Sales volumes of industrial stretchwrap increased due to continued growth in the prestretch wrapsmart product and good demand for blown hand reels due to customer wins. Sales volumes from the Wide Lines at Ardeer increased despite reduced supplies of silage sheet to the North American business as they experienced greater demand for silage sheets in the UK and secured new volume in Continental Europe.

Sales volumes in refuse sacks reduced by over 10% following the loss of some retail business at very low margins but operational efficiencies have improved and the group is starting to see benefits from the co-extrusion investment. Construction films experienced a slow start to the year with continued patchy demand in Q2 resulting in lower volumes but sales of the specialist gas and water proofing business continued to grow, up 9% as new products were introduced. In recycling, scrap availability continued to be the major concern, particularly in farm plastics where new start-ups in Ireland and Central Europe contributed to higher demand for farm waste. The new recycling line at Heanor is performing well and allowing access to more contaminated waste.

Volumes in the Visqueen packaging business were lower due to reduced demand from the construction sector and a poor season in the animal feed sector due to the mild winter. Sales to the peat/compost and furniture/bedding sectors saw some improvement. At Ardeer, a replacement printing press was installed towards the end of the first half and two replacement extrusion lines will be installed in the second half of the year. The UK consumer operation which supplies printed packaging for food to the supermarkets and major brands, continued to experience challenging conditions with lower volumes and intense margin pressure. The plant in China increased volumes in aprons and stretchwrap but has yet to secure any additional printed film food business.

The operating profit at the Mainland Europe division was £9.6M, a fall of £500K when compared to the first half of last year. This decline was entirely due to the weakness of the Euro and profits in the local currency actually increased by 6.5% with sales volumes up 7% to 49,500 tonnes as all three sites reported increases. Margins were squeezed by the exceptional raw material prices in Q2, however. Sales volumes of the silage products increased by over 10% with sales of advanced products SilotitePro and Baletite increasing by 31%. This increase arose against a background of cold weather in Northern Europe and consistent hot and dry weather in Central Europe. The significant polymer price increases in Q2 resulted in very difficult pricing and margins suffered, being below those of last year.

At Zele, volumes of Bontite, the premium industrial stretchwrap product, continued to grow aided by new legislation for load stability. Sales of printed film for the food industry increased by over 13% with growth mainly from the frozen fries sector but margins suffered from the polymer price increases. A replacement printing press with additional capacity will be installed in the second half of the year. In Roeselare, volumes improved as sales of stretch hoods, feedstock for printing and Formiflor, the thinner product for the insulation market. Sales volumes from the plant in Holland increased by over 4% with increased sales of FFS and printed film. Margins were squeezed here too by the increasing polymer prices. A replacement printing press for FFS was installed and the replacement of a number of extrusion lines was authorised.

The operating profit at the North America division was £800K, an improvement of £1.2M year on year. The division returned to normal production levels following the installation problems on a replacement large extrusion line that occurred last year. Agricultural sales were up by 15%, particularly in the agricultural bag market with customers reporting strong approval of products from the new extrusion line which is performing well with the products showing improved physical characteristics. Production output was much improved over 2014 but some power outages reduced levels to below expectations. Scrap levels have reduced and new and improved products are being developed for the market. Performance in the second half of the year will depend on market demand and weather and while there are dry conditions in California, the group is experiencing good grain bag bookings in Western Canada. The business will recover from the disappointing 2014, however, and further benefits should be seen from the new extrusion line.

As can be seen, the main issue during the period was raw material costs. During the first few months of the year there were clear signs of raw material costs falling but these costs accelerated to an all-time high during Q2 in Western Europe. Several factors accounted for this rapid rebound in costs. Firstly, import tariffs for polyethylene polymers from certain Middle Eastern countries increased from January. Secondly the euro depreciated in value against the US dollar, the currency used world-wide except in Europe to trade in the raw material. Both of these factors meant that it was less attractive to import polymer from the Middle East. Thirdly, the Western European producers suffered from an unprecedented number of force majeure incidents with more plant outages than ever seen before.

The raw material market has become less frenetic in the last few weeks and attention is again focusing on medium term reductions in feedstock costs on the back of imported shale gas from North America. Some minor reductions in price have been seen for certain grades of raw material and further reductions are anticipated over the coming months. Passing through the price increases was apparently very difficult so margins have been squeezed. Wholesale electricity costs are reflecting the lower oil and gas prices but there has been no relief in the UK due to increasing energy taxes and environmental levies.

Sales to the agricultural sector generally peak in the first half of the year due to seasonal weather conditions. At the period end the group had contracts in place for future capital expenditure of £10.3M. The most significant expenditure during the period was on the delivery and installation of replacement printing presses at Ardeer and Hardenberg. At Bromborough the group continued to replace and upgrade extrusion lines and at Leominster they ordered a seven layer extrusion line for silage stretch.

During the period, the pension scheme changed the index used to determine minimum pension increases from RPI to CPI which has resulted in the reduction of the present value of scheme liabilities of £27.6M. To increase the security for scheme members, the company also made a one off payment of £11.2M. These actions have resulted in a substantial fall in the deficit of the scheme from £99.1M at the end of last year to £59.6M at the end of the first half. This is still a considerable deficit but it is in a much better position than it was.

Demand remains at reasonable levels and with raw material prices having eased in August, the board are confident that they will meet expectations for the year as a whole. At the current share price the shares have a dividend yield of 2.4% which is expected to remain the same on the full year consensus forecast. At the period end the group had net debt of £29.2M compared to £24.1M at the year end and £29.8M at the same point of last year.

Overall then this has been quite a strong performance from the group. Profits were up, net assets were up due to the reduction in pension obligations and although operating cash flow fell, this was due to the one-off payment to the pension scheme and underlying cash profits increased. The lack of any free cash flow is a bit disappointing but this could be seasonal. Operationally the UK and Irish business was broadly flat, the European business saw profits fall but this was only due to the weak Euro as underlying profits increased, and North American profits improved following the issues surrounding the installation of the extrusion line last year. The one big issue during the period was the appreciation of polymer input costs at a time when oil prices have been showing unprecedented weakness. These prices were high into July at least with some respite in August so they will still affect the second half but the effect should be reduced as prices should ease following the re-start of Shell’s large Moerdijk plant.

The pension position is now much improved, although still a cause from concern and the continued weakness of the Euro is unhelpful. The shares yield 2.4% in dividends and the forward PE is about 10 which seems too cheap to me. With the easing of the polymer price and the continued benefit of a North American division that is working again I would have thought the second half looks potentially quite bright, full global economic meltdown notwithstanding. I am very tempted to buy some more here but it was recently reported that the MD of Europe, Michael Huyghe sold 25,000 shares at a value of £175K which leaves him with 83,292 shares left. This is a fairly decent chunk of shares that have been sold which leaves me a bit concerned and perhaps I should hold off buying shares at this time.

There looks to be a definite uptrend in play here.

There looks to be a definite uptrend in play here.

On the 11th November the group released a trading update. The group has seen some lower demand from certain sectors which has resulted in volumes to the end of October being below those of the same period last year, notwithstanding a 5% increase in sales of silage stretch-wrap. The shortfall in demand was offset by margin recovery during September and October and the group are now seeing order books firming again but polymer producers are seeking price increases for November. Overall the board remains confident that the business is on course to meet their expectations for the year.

Recent and imminent capital expenditure at Zele in Belgium and Leominster in the UK, the two largest facilities for production of blown stretch-films, has led to the decision to close a smaller facility at Widnes which will reduce costs. The group also plan to consult with employees to reduce numbers at the consumer facility in Worcester and in the films business at Sevenoaks on order to align staffing levels to current demand at these locations which is expected to result in about forty redundancies. In addition, in October they disposed of the loss making Promopack Digital Studio business for a consideration of £200K. In aggregate, the closure, restructuring, and disposal are designed to enhance future performance and will result in a one-off cost of £1M during 2015.

Overall then a rather mixed update but performance is still in line.

On the 21st December the group released a pre-close trading update. Trading remained consistent with the last update but raw materials have since increased with a forecast of further increases in early 2016. Overall, however, the board remains confident that the business is on course to meet their expectations for 2015, although the polymer price increases are cause for concern.

On the 27th January the group signed an agreement to sell its Chinese subsidiary to Amcor, an Australian-based packaging group. The consideration payable is estimated to be about £9.4M with an estimated £6.4M upon completion with the balance to be paid in cash in instalments following the agreement of working capital and satisfaction of certain post completion arrangements, all of which are expected to take place over the next year. The proceeds will be used to reduce borrowings.

The subsidiary was established to produce low cost carrier bags for the UK retail market but after the retail carrier bag business was sold in 2002, it diversified into other products for the UK market and latterly the group invested in high quality printing and conversion equipment to supply the Australian market. Progress was slower than expected, however and over the past year the business was in a break even position on sales of £9.6M. About 80% of the sales to BPI in the UK are expected to continue after completion. The disposal is expected to complete in 2016 and will result in a £4M gain on disposal.