Braemar have released their interim results for the year ending 2013. As normal I will start with the income statement.

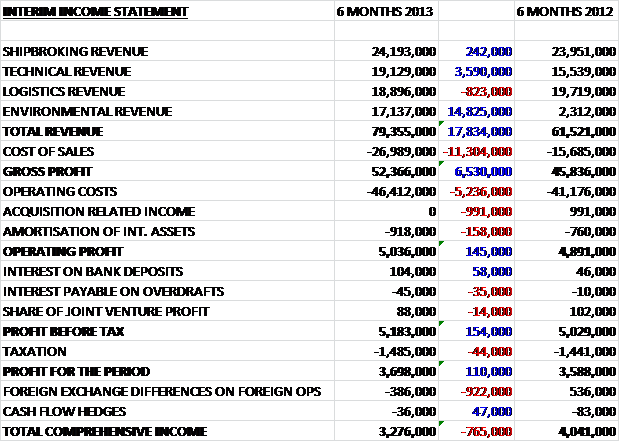

Revenue has increased substantially on the same period of last year. Shipbroking revenue is quite flat, while logistics revenue fell by £800K. Technical revenue is increasing steadily, and has been a growth focus for Braemar as late as they try to diversify away from shipbroking, up by £3.6M. The big increase, however, is from the environmental segment, up a massive £14.8M to £17.1M as the group ramp up the recovery related to the MSC Rena. Cost of sales are also up, but overall gross profit is up £6.5M. We can also see operating costs up, and the lack of income related to the acquisition which means that operating profit is only £145K up, at just over £5M.

After a bit of finance income is counteracted by an increase in tax the profit for the period was broadly similar to the first half of 2012, up £100K to £3.7M. Unfavourable foreign exchange rates mean that the actual income received was £765K less at £3.3M.

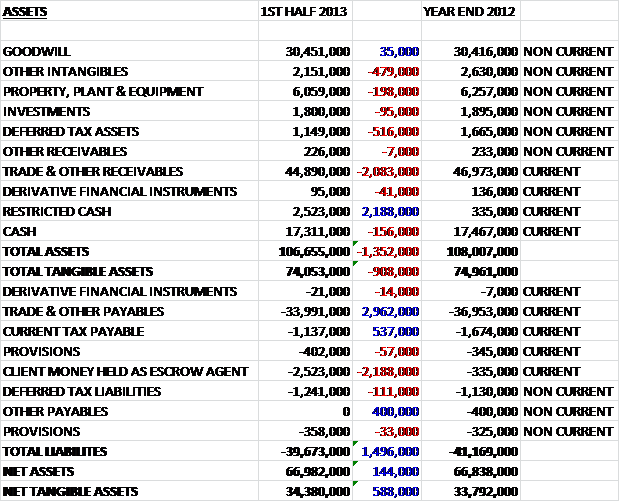

Looking at the assets initially, we can see these are almost uniformly down on the position at the end of the year. Ignoring the restricted cash, which has a liability against it, the rest of the assets are down slightly. The tax asset is probably the biggest faller, down half a million to just over £1M. Total tangible assets are down by £900K to £74.1M.

Liabilities are also lower, with trade and payables down nearly £3M to £34M. This means that net tangible assets increased by £600K to £34.4M.

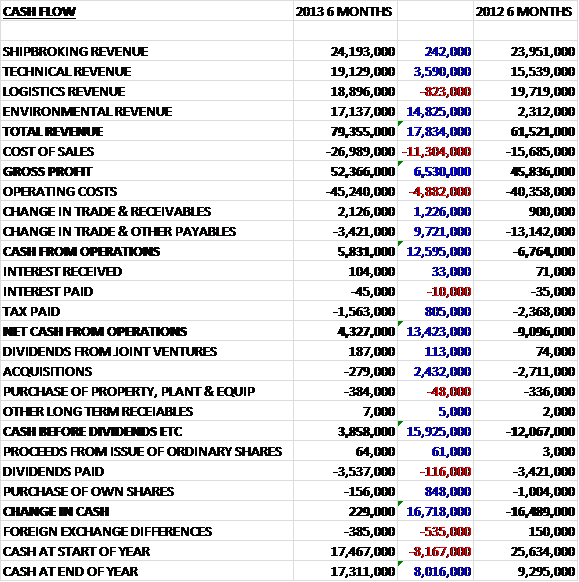

Overall, cash from operations from the first half of the year was £5.8M. This compares to an outflow of £6.8M for the same period of last year. This positive swing is due to better control over payables. After tax and interest was paid, the group still had an inflow of £4.3M. There does not seem to be much in the way of capital expenditure here and there was a small amount of cash paid for acquisitions which means that before dividends, there was an inflow of £3.9M. Most of this was then paid out to shareholders to leave a cash flow of £229K. Unfortunately due to the unfavourable swing in exchange rates, the cash position was very slightly worse than the same period of 2012, however, the position was much better than last year.

Most of the profit is still from shipbroking, but the Environmental sector achieved the second highest contribution, receiving more than twice that of the Logistics business, which is a little concerning given the volatile nature of environmental revenues. Technical profits were only £1.2M, which was lower than the same period of last year. Actually, all sectors had lower profits than the first half of 2011 apart from the Environmental segment.

In the half year the group purchased Orca Shipping for £820K. It came with £509K of cash so in total £311K was spent on this acquisition, £79K of which was deferred. I am not sure what Orca do exactly but it seems to have come fairly cheap and contributed £49K to the profits during the period.

The shipping industry in general has continued to struggle as most sectors still suffer from a surplus of tonnage and a weaker rate of growth in the Far East, which is the main driver for global shipping and fleet growth continued to outstrip supply. However, the rate of scrapping has quickened so the excess tonnage continues to work its way through the system (also good because Braemar are involved in the scrapping business too).

During the half year, the CEO left the company and was replaced by the CFO, James Kidwell and a new CFO was recruited, Martin Beer. I hope this won’t cause too much instability as I felt the outgoing head did a good job. Time will tell, I guess.

Going forward, the work on the MSC Rena should continue to the end of the year, but after this a substantial contributor to the profitability of the group will be lost. The other divisions are expected to continue as they are for the rest of the year.

In bulk shipping, fleet growth was 9% in 2012 as newbuild deliveries outstripped demolition, however scrapping rates have increased in recent months. Demand for bulk cargoes such as coal and grain continues to increase but the slow down in China has led to a reduction in iron ore demand. Having said that, performance of the group in this market has been good.

Transaction volumes for single tanker voyages have increased but the time charter business remains slow with owners reluctant to commit in the present climate but the levels of enquiries are beginning to increase. The growth in deep sea tanker fleets was 3.5% and the trade in crude oil continued to increase, driven by demand in the East and new refineries are being built in this region to accommodate this demand. The demand for crude in the US is falling, however, as greater fuel efficiency and lower demand takes effect. The specialised tanker team has performed consistently with a good level of contract business for European clients. The LNG tanker market is expanding.

The container market remains challenging due to the lack of consumer demand but the group are anticipating a cyclic recovery. Vessel values remained low and second the second hand market was slow. There is more of an opportunity in the demolition market, however, as the surplus tonnage and a reasonably strong steel price keep things ticking over. The offshore vessel market is strong, and there have been good revenues from this sector, particularly in the Far East and East Africa.

The technical division has grown revenues and the Offshore, Engineering and Surveying businesses were all busy in the Far East. The group are also involved in some long term offshore energy projects in the Asia Pacific region, providing warranty surveys and engineering consulting, and have opened an office in Thailand to capitalise on this as the group expect this to be a growth prospect. The salvage business performed within expectations and the adjusting business showed a steady performance with work in the tar sands region in Canada and offshore business in South America. Braemar Engineering is working on several LNG construction projects but offshore engineering work in the Gulf of Mexico has been more limited than expected.

Within the logistics sector, the UK and Singapore ship agency business performed well and has recently won some important new contracts, including managing the European hub for an oil company. The logistics performance was lower than last year due to the lack of one-off project forwarding business and the Olympics did not provide the boost for the cruise business that was expected.

As previously mentioned, the Environment arm that is working on the MSC Rena has been a major contributor in this half of the year. The sector does have some ongoing contracts and consultancy in this area but as the recovery of the Rena is winding down, income will be far lower next year.

So, for the half of the year revenues are up substantially but this has been driven by the one-off work on the MSC Rena. Other divisions were more steady but revenues were down in Logistics, which did not benefit from the one-off projects they had last year. Profit is fairly level at £3.7M, which is a bit of a worry given that a fair amount of that was contributed by the Environment sector. Cash flow was fairly decent, pretty much neutral once the dividend was paid out. There is now a new CEO in charge so it will be interesting to see how the group performs under him. The dividend is a whopping 7% and the group has not performed badly this half of the year, plus there is no debt here at all. However, I have concerns over where the revenues are going to come from once the work on the Rena has been completed. Overall I continue to hold.

On 16th January 2013, Braemar released an interim management statement. It was mentioned that Shipbroking was facing challenging conditions with excess capacity affecting rates and that an increasing proportion of business is on the spot market. The technical services segment performed as expected, as did the Logistics division as the hub agency contract mentioned in the last update started. However, revenues from the Environmental division was less than expected as the involvement in the MSC Rena project reduced quicker than expected.

Although, there is not much here that wasn’t known already, the fact they mention their two most profitable sectors are finding things tough is a real worry and I expect profit to be down for the full year. I still hold, however for the moment.