Compass House, Guildford Street, Chertsey, Surrey, KT16 9BQ

Compass is a large FTSE 100 company who provide culinary and maintenance outsourcing services to companies and institutions in various sectors. Less than half of the food service market is currently outsourced and Compass sees this as an opportunity to target. Most of the new business Compass achieves come from companies who have outsourced these services for the first time as opposed to Compass’ direct competitors. The bulk of the work is in food outsourcing, but the group also offer cleaning, reception and light building maintenance. It is active in the following sectors:

Business & Industry – this is the most important source of revenue for Compass, accounting for 42% of revenues in 2012. They provide food and other services to offices and factories.

Education – Accounting for 16% of sales, Compass provides meals for schools and colleges.

Healthcare & Seniors – Accounting for 19% of revenue, Compass provides food and other services to hospitals and offer care services to residential homes and home meal delivery services.

Sports & Leisure – This sector is the smallest, only accounting for 10% of revenue. Compass provides services to stadiums, exhibition centres, visitor attractions and major events.

Defence, Offshore and Remote – This is 13% of group revenues and involves providing food and support services to the oil & gas, mining and construction industries. Services are also supplied to the defence sector under this segment.

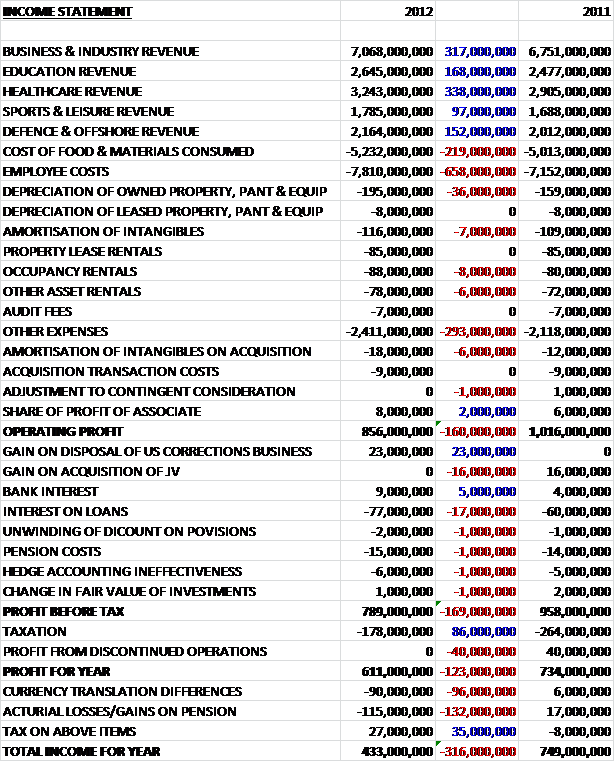

Here is the income statement.

Revenue is up across the board with healthcare revenue showing the largest percentage increase, up £338M to £3.2B. We also see that costs have increased at a greater level, however. Cost of raw materials is up substantially but the biggest increases come in Employee costs, up £658M to £7.8B and “Other Expenses” which are up a hefty £293M to £2.4B. This is a big increase, so I would like to know what is included. Due to these increased expenses, operating profit was £160M less at £856M. The increase in finance costs relates to the pension deficit, costs relating to the share buyback and the raising of the new debt in the US private placements. A similar amount expected in 2013 with another pension deficit charge and another share buyback.

We see that there is a one-off gain of £23M (net £13M after tax) on the disposal of the US corrections business but most of this is non-cash as it is due to the release of provisions allocated against this business. Last year there was a similar level of one-off gains, however, as £16M was earned on acquisitions – this was a non cash gain due to the re-rating of the value of the current investment in the JV (Sofra Yemek Uretim). The major financing charge is the interest on loans, at £77M, which was £17M higher than last year. All this means that the profit for the year before tax and the profit on discontinues operations was £789M, down by £169M. A lower tax charge, however, was not entirely counteracted by the loss of the profit from those discontinued ops received in 2011 and profit for the year was £123M less at £611M.

There was a bit actuarial loss on the pension scheme and this, combined with negative differences in currency translation mean that the total income for the year was a whopping £316M lower at £433M. On the surface this performance looks a little disappointing.

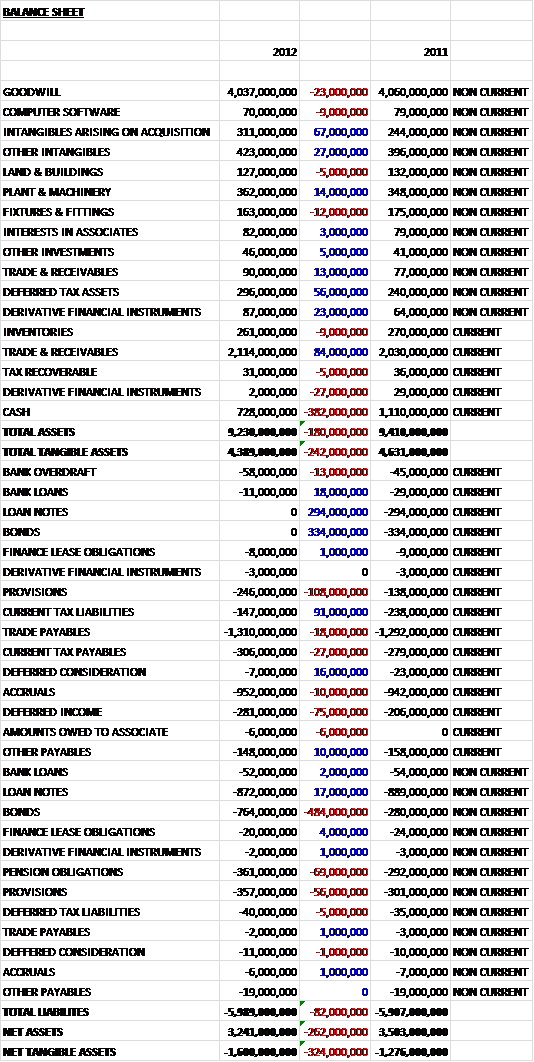

Starting with the assets, we can see that total assets are down by £180M to £9.2B. This fall is almost entirely due to the reduction in cash of £382M. The largest asset base is Goodwill, at over £4B. This is a sign that Compass has been making quite a lot of acquisitions in the past and it always makes me a little nervous when the largest asset is Goodwill, due to its intangible nature. Most other assets have shown modest increases on last year. Trade receivables are very diverse so is not a huge risk – receivable days are now 46 from 48. There are still £437M overdue though and this figure includes a £33M deduction relating to European exceptional non-payment of receivables. New controls have now been introduced to ensure the quality of new and existing business so going forward this should not happen again.

Liabilities have also decreased, but only by £82M. One good point here is that we see a complete elimination of £294M of current bank loans, partially replaced by non-current bonds. There seems to be a reduction in tax liabilities but there are a number of large increases of certain liabilities that I think should be flagged up. First we have a £164M increase in provisions, up to £603M. This seems like a lot to me and the increase was to do with the restructuring of the European business and relates to loss making contracts and the non-recovery of some debts. There are also provisions for insurance policies and environmental provisions, which are set aside to make sure the group makes its commitment to have a low environmental impact and relates to operating sites. Also we see a £75M increase in deferred income, up to £281M which also seems like a big increase. Finally there is a £69M increase in pension obligations which seems to be a bit of an issue for a number of companies at the moment.

All the above means that net tangible assets are £324M lower, at -£1.6B. The reduction in some of the debt is pleasing but the increase in some of the liabilities and the negative tangible asset base is something that I will keep an eye on. Compass does not seem to have much in the way of traditional bank loans but instead have private placements and Eurobonds. I am not sure of the advantage of these over more traditional fund raising methods, the interest rates seem to be between 3% and 7.5%.

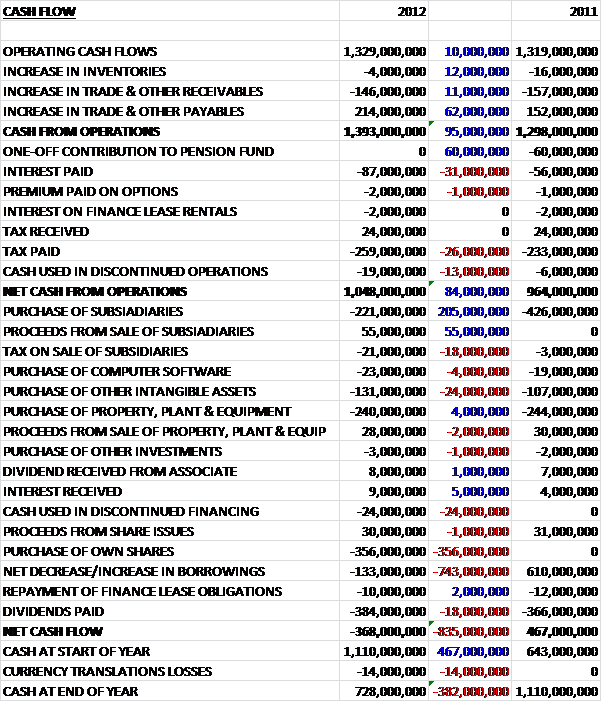

So, there seems to be a bit of a negative cash flow going on here – the group lost £368M during 2012, a whole £835M worse than last year. So what happened? We see that cash from operations was pretty good, after movements in working capital there was a cash inflow of £1.4B. After tax, and an increased amount of interest, there was still £1B of cash coming into the company. Some of that tax charge includes a £31M cash outflow to settle historic tax issues. The group made a one-off £55M from the sale of subsidiaries, but spent £221M on new acquisitions (considerably less than last year). Over £200M was spent on new property and equipment, and another £150M on intangible assets. The big difference over last year was the borrowings, £133M was paid back on loans, compared to new borrowings of £610M. The group also spent £356M on a share buy-back scheme and £384M was paid out in dividends.

So, were it not for the repayment of the loans (a lot more are still outstanding in the form of bonds) and the share buyback, the cash flow here would actually be positive. It isn’t massively positive but it is certainly not as bad as it first appears. I am not sure of the wisdom of buying their own shares – there is not really the free cash flow to do it, and if there was I would prefer some sort of cash return to shareholders but not much I can do about that! Due to the restructuring of the European business, there was a £20M cash charge and another £80M to be spent this year to cut costs and improve efficiencies.

There was a £54M outflow on pensions relating to payments agreed with the trustees to reduce deficits on the scheme. These regular payments are expected to continue going forward. The pension fund deficit now stands at £361M and £75M will be paid in first half of 2013.

Compass divides its regions into three segments: North America, Europe & Japan and Fast Growing and Emerging. The fortunes of the different regions have been contrasting. In North America, the largest by revenue (44%), business has been good and sales have grown organically by 8%. In Europe & Japan (37% of revenues), trading conditions have been difficult due to the well documented economic woes in the EU but Japan has mitigated this somewhat. Fast Growing (19% of revenues), like it says on the tin, grew sales by 12%. Therefore the group seems to have done well in North America and Emerging Markets but is being pegged back by the situation in Europe. There have been some announcements to improve efficiency in Europe for the long term.

Compass seems able to keep hold of their clients well and retention rates are over 94%, and those have seen some softening as companies in Southern Europe close. The like for like revenue growth seen is primarily due to price increases driven by food inflation that has been passed on to clients. Like for like volume remained flat with a positive trend in Emerging countries contrasting to a flat trend in North America and a decrease in Europe. Key emerging markets are Australia, Brazil and Turkey with China and India also being targeted. North America is still the most important region, however.

North America accounts for the largest amount of revenue. By sector, North America is made up of 31% Business & Industry; 27% Healthcare & Seniors; 24% Education; 13% Sports & Leisure and 5% Defence, Offshore & Remote. This year successes have included a 10 year contract to provide food and support services to the Texas A&M university system, which is the 6th largest educational institution in the US. Another notable contract win has been the Ascension Health contract.

In Business and Industry, contract wins at Adobe and IDC Research with contract retentions for Wal Mart and Proctor and Gamble have driven an increase in profit. The Healthcare sector delivered strong growth in profit with new contracts for Ascension, Cathedral Village Retirement community in Philadelphia to deliver a food service and the Victoria general and Royal Jubilee hospitals in Canada. Additionally, a contract to deliver support services to the University of Kentucky hospital was won. Revenues were up in the Education sector with new contracts for the Texas A&M university, University of Illinois, and retention of the Simon Fraser University contract in Canada. Given the size of the new contracts, some capital expenditure is planned to upgrade existing facilities. In Sports and Leisure, new contracts included the Barclays Centre and the BBCA Compass stadium. The group also has contracts supplying businesses in Alaska, Canada and the Gulf of Mexico.

Europe and Japan account for the second highest amount of revenue and it is fair to say things have been difficult here. By sector, the revenue percentages are Business & Industry 56%; Healthcare & Seniors 15%; Education 12%; Sports & Leisure 11% and Defence, Offshore & Remote 6%. Organic revenue in the region declined by 0.7% due to the worsening conditions in Southern Europe.

In the Nordics, the group won a contract with Scania; in Netherlands a contract win was recorded for UWV, in France a contract was won with Cash Nanterre (a hospital) and in Spain a food contract was won with Sanitas Group, a private healthcare insurance group and the multiservice contract with Pfizer has been extended. In the Nordics and Germany volumes were flat and in France and UK conditions deteriorated somewhat while in Italy, Spain and Portugal volumes decreased by about 5%. Trading conditions in Japan improved as the country recovered after the Earthquake and Tsunami last year. The group incurred a charge of £295M to address the poor conditions in Southern Europe with £100M earmarked in improving efficiencies and £195M for “further actions”. Not sure what this is for but it will apparently result in a £20M improvement in the profit performance next year.

The Fast Growing and Emerging sectors are still the smallest by revenues but they are becoming more important. In 2012, the revenue split was Business & Industry 40%, Defence Offshore & Remote 44% (probably mostly Australia); Healthcare 8%; Education 5% and Sports & Leisure 3%.

An important country for Compass is Australia, one of the top 5 by revenue. The most important part of the Australian operation is the running of camps that provide transient accommodation for the workforces of oil, gas and ore miners. Food and living services are provided, along with maintenance of the facilities to house the workers. This year has seen double digit organic growth in the country so it is continuing to contribute well – hopefully a Chinese slowdown won’t affect them too much. Brazil is another country that saw double digit organic growth. A new contract has been won at the Mendes Junior Holcim project and the food service contract with ThyssenKrupp was maintained. Elsewhere in Latin America, Compass extended a contract with Sanofi Aventis and operated the Pan American games. In Argentina, a new food service contract with Peugeot and a multi service contract with Petrolera was achieved. In Colombia, a contract with AngloGold has been won.

Turkey is a good prospect, and Compass has been spending money on acquisitions here. New contracts in the country have been won with Universal Hospitals, Goodyear and British American Tobacco. South Africa has also been strengthened with an acquisition and in Australia new contracts have been won with Xstrata Copper, BHP Billiton and Goldfields. In China, new contracts were won with Caterpillar and an extension in the contract with MTR Corp. Finally, in India new contracts include those with Medanta (hospitals) and Damiler India.

Potentially, there are a number of issues that could affect Compass. The Business & Industry and Sports & Leisure segments (about 50% of the business) are susceptible to economic downturns, as has been seen in Europe. Another issue facing Compass is food inflation but this can generally be passed on to customers as it is often included in the contracts. The pension scheme is another potential source of problems and is causing quite a drain on finances but it is now closed to new entrants. Currency changes can also cause problems and the strengthening of Sterling has been a bit of an issue, particularly against the Euro and Brazilian Real and had the effect of decreasing reported revenue by just over 1%.

Going forward, it is expected that the profit from the 2012 acquisitions will be offset by the lost profit from the disposal of the US Corrections business. It is not clear to me why this business was sold, other than the stated desire to concentrate on core businesses. After the balance sheet, the group purchased Crown Camp Services, a food and support services company in the Oil and Gas industry; and Nova Services, a company that provides food and support services to the business and healthcare sectors in Canada. Compass will continue to look for new acquisitions.

So, we have seen that revenues are up, with healthcare in particular doing well but within this we see a difference within the regions, with emerging markets doing well, North America holding its own and Europe contracting. Costs have also increased, mainly due to increased wages and food inflation but this means that the profit for the year was a whole £123M lower at £611M. The balance sheet is dominated by the Goodwill which means there is a negative tangible asset base, which widened by £324M to a negative £1.6B, which I can’t help but feel a little concerned about.

There was a big outflow of cash, with the group losing £368M over the year, but when the £356M spent on the share buyback scheme is taken into account, this looks rather more healthy. It does, however, mean that net debt rests at almost £1B. There is another £400M earmarked for the share buyback in 2013, which I am not 100% happy about.

Looking forward, steps are being taken to address the issues in Southern Europe and as long as North America holds its own, prospects look pretty good. Food inflation is also worry but Compass seems to be pretty good at passing this on to customers. The dividend yield on the current share price is an unexciting but decent 2.7% (maybe some of that cash the company doesn’t have for the share buyback could be returned with dividends…). The current P/E ratio is quite a hefty 18.4, and based on analyst predictions, the forward P/E of 16.8 doesn’t earmark this share as a bargain either. Having said that, this is clearly a successful company in an enviable market position, so I intend to keep hold of the shares.

On 7th February, Compass released a statement covering the first quarter of the year. Overall things have progressed well and organic revenue growth was 6%. However, conditions in the three regions remained similar to that expressed above. Revenues were good in North America, strong in emerging economies but week in Europe and Japan. However, the measures that have been put in place to reduce costs are apparently going well. A few more acquisitions have taken place – all in the Americas and all seem to be quite sensible. Overall, fairly good – no surprises in this statement and the shares for me are still a hold.

On 26th March, Compass released a statement covering the first two quarters of the year. It seems things are much the same and trading remains strong in North America, with revenues up 8.5% on a comparable working day basis. In Europe, things continued to deteriorate and revenues on the same basis are expected to be 2.5% down, although the cost cutting exercise should mitigate this effect somewhat. Emerging markets continues to perform well, with the oil and gas industry in Australia singles out as being particularly good. Revenue growth is expected to be over 10% in the first half with a similar profit margin.

About £80M has been spent on further acquisitions, with acquisitions in Colombia, US and Canada. The share buy-back program continues to progress. Overall, this is a good update. Revenues in North America and emerging markets are progressing very well, and it is quite exciting to see some up and coming economies becoming more important for Compass. The European results continue to drag but the cost cutting methods seem to be bearing fruit. Still a strong hold for me.