Kalibrate has now released its final results for the year ended 2015.

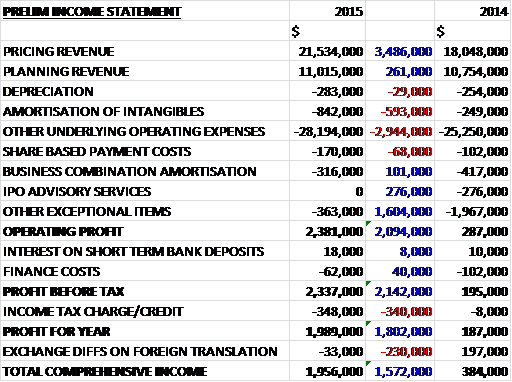

Revenue increased when compared to last year as pricing revenue was up $3.5M and planning revenue grew by $261K. There was a greater amount of amortisation and other underlying operating expenses were up $2.9M but this year benefited from the lack of $276K worth of IPO advisory services and other exceptional items totalling $2M that occurred last year so, although there as $363K relating to costs from the company’s floatation, including severance pay of $181K to Brad Ormsby. The operating profit was therefore, some $2.1M higher. Finance costs fell by $40K but the tax was much higher so that the profit for the year came in at just under $2M, an increase of $1.8M year on year.

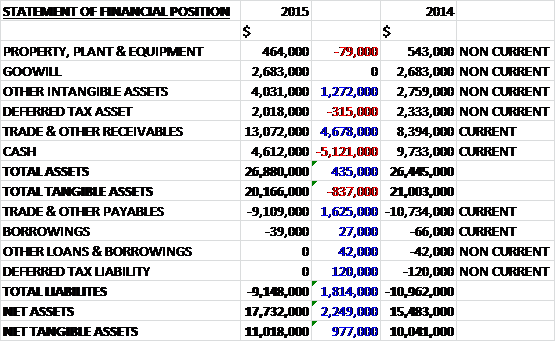

When compared to the endpoint of last year, total assets increased by $435K driven by a $4.7M growth in receivables and a $1.3M increase in other intangible assets, partially offset by a $5.1M decline in cash levels and a $315K fall in the deferred tax assets. Liabilities fell during the year mainly due to a $1.6M decrease in payables which meant that the net tangible assets were $11M, an increase of $977K year on year.

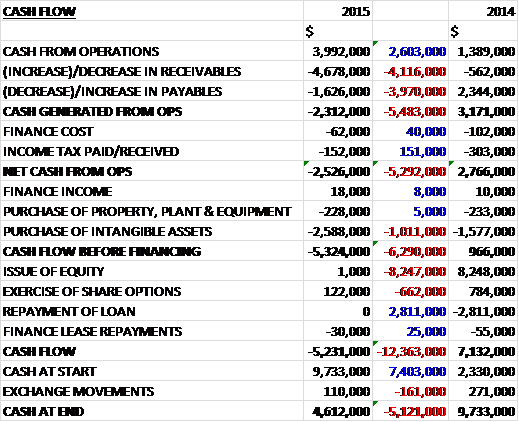

Before movements in working capital, cash profits increased by $2.6M to just under $4M. Large increases in receivables, apparently as a result of some significant deals closed at the end of the year, and declines in payables meant that there was a net operating cash outflow of $2.5M for the year, a detrimental movement of $5.3M year on year. The group then spent $2.6M developing intangible assets and $228K on property plant and equipment which meant that the cash outflow before financing items stood at $5.3M. The group gained a small amount from the exercise of share options, partially offset by some finance lease repayments so that the cash outflow for the year stood at $5.2M to give a cash level of $4.6M at the year-end which is clearly not a sustainable state of affairs.

The underlying operating profit in the pricing division was $1.7M, an increase of $109K year on year. The group achieved revenue growth in all geographies. The Americas increased 18% due to a positive mix of SaaS and perpetual license wins; Europe increased 24% due to the full implementation of its large managed services contract with a major oil company and several SaaS and perpetual license deals. ROW improved mostly from SaaS pricing wins in SE Asia and Australia. This growth has been achieved whilst they had the overall trend of a growing number of their clients electing to enter into SaaS model contracts instead of large upfront perpetual license contracts.

The underlying operating profit in the planning business was $1.5M, an increase of $72K when compared to the first half of last year with revenue increasing modestly to $11M. This increase in revenue in North America, Europe and Africa was offset by declining revenues in Japan. The Japanese planning market is very mature and the group experienced a very strong year in 2013 with a considerable amount of market activity. Since then, the market has retrenched into established site plans. The country’s pricing market, however, is as yet undeveloped and the group is adding resources to the market in order to introduce their pricing product. The group has seen significant increased planning projects in its core markets and has secured new clients for planning services in Bosnia, Bulgaria, Chile, the Czech Rep, Ireland, Kenya, Mexico, Romania, Morocco and Serbia.

The group has experienced demand for both planning and pricing products in deregulated markets including Latin America, Africa, India and SE Asia. Mexico deregulated during the year and Kalibrate completed a consulting project for a retail chain and, at the end of the year, signed a planning contract with one of the fastest growing fuel retailers in the country. A significant pricing deal in Brazil opens further opportunity in South America. They also won several SaaS pricing contracts in the Philippines and Australia, while in India they have been working with a national oil company on planning and pricing models as they prepare for competition to increase in their newly deregulated market.

Geographically, in North America pricing revenue was up 18% due to perpetual and Saas license wins with several strategic tier one accounts. Similarly, planning revenue increased by 13% mostly as a result of successfully cross-selling planning products to existing pricing customers during the period and from generating new revenue from additional data reselling. The revenue for Europe increased by 32% due in part to the implementation of the significant managed hosting relationship with a major oil group, several strategic pricing deals and some significant planning deals. The pricing revenue increased by 24% from the large managed services client and from multiple oil company pricing deals. The planning revenue increased this year does not fully reflect a large planning deal that started towards the end of the year with most of its revenue being earned in future years.

The revenue in the rest of the world was down 13% due to a 26% decline in the Japanese market due to a reduction in sites to survey, an effect of overall market retrenchment, partially offset by an improvement in African market studies and wins in SE Asia and Latin America. With the continuing deregulation trend in various countries throughout the world, the group continue to see growing demand for both their pricing and planning lines in the ROW regions.

The group have had success this year in generating revenue from their existing clients, which has been achieved through cross-selling their pricing and planning products as well as expanded services and data reselling. At the time of the IPO, 18 of their clients purchased both planning and pricing products and at the year-end this stood at 31 with further room to grow. They have been able to expand some key relationships within mature markets of North America and Europe to grow their market share further. The complexities of managing fuel and convenience retail performance are increasing. A larger number of legacy and in-house systems are therefore being used by some clients that are no longer able to cope with the volume of data and sophisticated analytics required to keep pace with market dynamics. The group should be able to capitalise on these opportunities and help clients manage this complexity.

Deregulating markets present significant opportunities for the group’s strategy consulting services and pricing and planning solutions. They continue the groundwork and processes with a priority on India, where deregulation was announced in October 2014. They have expanded their relationship with a major client in India since deregulation and are pursuing new opportunities in the region. Management continue to see expansion opportunities in Africa, SE Asia, India and Latin America and in each of these growth markets, the drivers for progress remain the deregulation of fuel pricing in various countries, increased competitiveness in the fuel retail industry and add-on business from existing clients.

Kalibrate Cloud 1.0, the SaaS solution was launched in September 2014 and will be followed with the launch of significant upgraded capabilities in Kalbrate Cloud 2.0 as of October 2015. This upcoming update represents a significant step forward in expanded pricing capabilities, enabling pricing management from the fuel forecourt to in-store. This means that Kalibrate is the only company to offer this end-to-end capability.

The growth of the group’s managed services offering has evolved more quickly than expected. They invested significantly during the year and with their partner, Rackspace, they serve 28 managed services clients, including the largest contract in the group’s history which generates about $2M per annum. At the point of the IPO the group had a hundred existing pricing clients who they felt they could convert to managed service contracts. At the start of the year the number that had been converted stood at 14 and by the year-end this had doubled to 28. The focus remains on continuing to convert existing clients as well as adding new clients to the managed service offering in order to grow further the recurring revenue base and the Kalibrate Cloud single platform should be the driver for clients to move to managed services.

Due to market trends and client demand, the transition from software installations to SaaS contracts accelerated during the year. At the same time the group converted a number of existing perpetual license clients to SaaS based agreements. The SaaS solution enables the group to reach new market segments optimised for mobile delivery such as India, and more efficiently deliver solutions in a way that fits with clients’ operational imperatives. Next year will continue to see the group make this transition, allowing them to create a business that can deliver higher recurring revenues, even stronger client relationships and enhanced margins for the long term. In the short term, however, this does mean that cash collection is reduced. Indeed, three large clients switched to the SaaS model which would have generated about $2M in additional cash had they closed as perpetual license deals.

The group is becoming somewhat susceptible to the loss of one client, with one global customer contributing 12% of the group’s revenue. This was an increase from the 9% last year. The order book improved by 15% to $41.4M and was strengthened by annualised recurring revenue of $21M compared to $19.6M in the prior year. The group enjoyed a remarkable 100% global client retention rate for the past year which is good going in my view.

During the year Gregg Budoi replaced Brad Ormsby as CFO. He brings over twenty years of experience in the petroleum retail, convenience store and finance sectors, and intriguingly has extensive merger and acquisition experience.

The board remains committed to the strategy of securing new and converting existing clients to the SaaS model to provide further revenue visibility, improving gross margins and ensuring longer-term client relationships. Based on this continued momentum, the board expects to see continued progress in the year ahead and remains confident that the group is on track to achieve its current targets for 2016.

At the current share price the shares trade on a PE ratio of 26.6 which seems rather expensive to me, I don’t have a very up to date broker forecast but the forward PE is about 24.3 which still looks rather expensive to me. At the end of the year, the group was in a net cash position of $4.6M compared to a net cash position of $9.7M at the end of last year.

After the period-end the group announced a new reseller partnership with Clear Demand Inc. They have full global exclusivity to provide fuel retailers with Clear Demand’s in-store merchandise and promotions pricing capabilities, white-labelled under the Kalibrate Brand. By adding this service, Kalibrate will be the only business decision platform that enables the control of the entire fuel and convenience retail industry, from forecourt to in-store. This differentiation expands the group’s market size globally and strengthens its position as the industry leader. They have already entered into initial pilot programs with four clients.

Overall then, this was an interesting year for the group as they cemented their status as a listed company. Profits increased year on year, aided by less exception costs but the underlying profit still improved. Net assets also increased and although the underlying cash profits did improve, the real problem is the operating cash flow. A large increase in receivables, apparently due to some large contract wins at the year-end and the continued increase in SaaS contracts meant that operating cashflow actually deteriorated this year to a net outflow.

Operationally, the pricing business is gaining tractions and while the planning business also improved, the decline in Japan due to strong comparatives last year meant this increase was modest. Going forward, there remains considerable opportunities in recently deregulated markets and India must have huge potential. The reseller partnership with Clear Demand also looks interesting and should increase the group’s offering considerably. Despite this, I do feel that a forward PE of 24.3 is a bit much to ask for a company that is losing cash at the operating level so I will remain on the side lines here for now.