Ricardo has now released its final results for the year ended 2015.

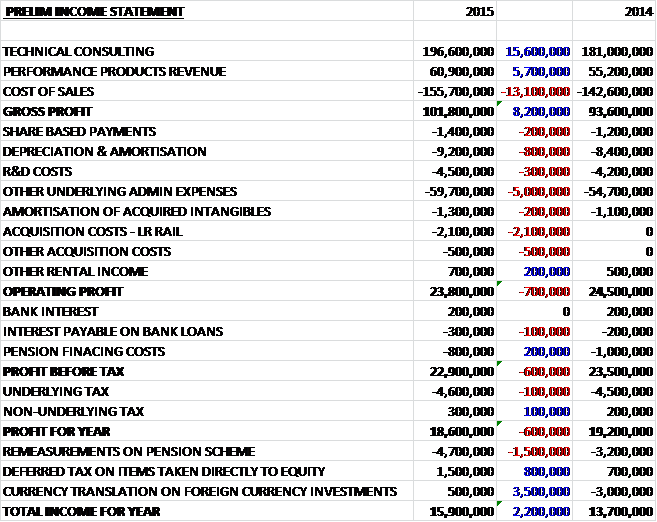

Revenues increased when compared to last year as Technical Consulting was up £15.6M and Performance Products grew by £5.7M. Cost of sales also increased to give a gross profit £8.2M ahead of last year. We then see an £800K increase in depreciation and amortisation along with a £5.3M growth in other underlying admin expenses. There were a number of one-off expenses, including £2.1M relating to the acquisition of LR Rail and £500K relating to other acquisition costs which meant that operating profit was some £700K lower than last year at £2.8M. A slightly lower finance cost due to lower pension financing costs then meant that the profit for the year came in at £18.6M, a decline of £600K year on year.

When compared to the end point of last year, total assets increased by £67.4M driven by a £47.1M growth in cash, a £12M increase in receivables, a £2.8M increase in deferred tax assets and a £2.2M growth in other intangible assets. Liabilities also increased during the year due to a £45.4M growth in bank loans, a £7.5M increase in payables, a £2.6M increase in current tax liabilities and a £2.6M growth in deferred tax liabilities. The main change we can see here is a £45.4M new bank loan that was used to increase the cash so that the group could make a payment for the acquisition of LR Rail. The end result of all this is a net tangible asset level of £71.1M, an increase of £5.3M year on year.

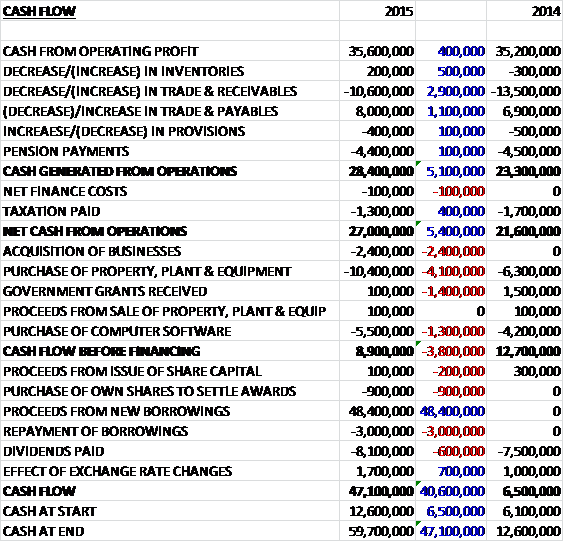

Before movements in working capital, cash profits increased by £400K to £35.6M which became a net operating cash flow of £27M, an increase of £5.4M year on year as receivables increased by less than last year and payables fell by less. The group then spent £10.4M in fixed assets relating to planned cash expenditure at the Shoreham Technical centre on both the expansion of the vehicle assembly facility as part of the supply agreement with McLaren, and the Vehicle Emissions Research Centre (£5.3M net of government grant); and £5.5M on computer software to give a free cash flow of £11.3M. Some £2.4M was spent on acquisitions, £900K on shares for pay awards and £8.1M in dividends. The group then took out a net £45.4M of new borrowings to give a cash flow of £47.1M and a cash level of £59.7M, ready to spend on the LR Rail acquisition.

The underlying operating profit at the Technical Consulting division was £20M, an increase of £2.2M year on year. Underlying operating margins have increased from 9.8% to 10.2% with the order intake increasing from £192M to £209M. During the year the UK and German Technical Consulting businesses have been integrated to form a European Technical Consulting division, along with a separate global motorcycle division which includes the newly acquired Vepro business. The European division secured a range of large multi-year programmes in the passenger car, commercial vehicle and power generation sectors in particular. Activity levels have been particularly high in the engine and vehicle groups and this division remains the main generator of profit.

In Ricardo Motorcycle the focus has been on the delivery of existing large multi-year powertrain programmes and the global roll-out of an expanded product and service offering to existing and new clients. As a result they have secured a new multi-year vehicle programme with an international client in the motorcycle and scooter section of the market.

In the US, the business has maintained its commercial performance in the passenger car and commercial vehicle sectors whilst positioning the business for growth in other areas. The business mix has seen increasing engine testing activity across both light and heavy duty applications and increased interest in rail and energy sectors. The defence activity continues to diversify and during the year the group launched Ricardo Defence Systems to enable them to access higher level security programmes from the US Defence Administration. The California business is growing and they will continue to see expansion in activities in that area.

Asia, including China and Japan, remains a key region and the Shanghai based business has secured and started to deliver a number of large locally won contracts. This has included a mixture of hybrid vehicle, engine, transmission and attribute development activities. In Japan they have seen good levels of performance in the passenger car and commercial vehicle sectors. The Energy and Environment business has had a good year and has seen growth in both international and private sector clients. The five historic practice areas of Energy and Climate Change, Air Quality, Resource Efficiency and Waste Management, Sustainable Transport and Rick Management have performed within expectations alongside PPA which was acquired during the year and integrated as a sixth practice area. The strategic consulting activities continue to operate well across all geographies and performance has been good in all operating regions.

The passenger car sector remains the most significant market for the group. Projects continue to be driven by emissions legislation, CO2 reduction and global competition. During the year demand remained high, with large multi-year contract orders from automakers and suppliers in the UK, EU and Asia. New orders were secured across the vehicle systems and core powertrain areas of the business, focused on both new products and upgrades to existing products.

One of the key drivers of the strong demand is the requirement to deliver lower carbon dioxide solutions at lower cost whilst still maintaining high levels of functional performance. This is driving increased interest in the vehicle lightweighting, advanced combustion and intelligent vehicle and driveline technologies. Autonomous vehicle technology in particular is attracting significant interest in North America. Interest in hybrid and electric vehicle architectures, battery pack and battery management system design and vehicle attribute development also feature strongly. The Vehicle Emissions Research Centre was commissioned at the Shoreham Technical centre during the year and the group continues to invest in advanced combustion and other key technologies in areas related to improvements in overall vehicle efficiency, such as intelligent driveline, lightweight materials and electrification.

The group’s activities in the government and environmental sector have been driven largely by the long-standing relationships that the business has with government bodies in the UK, the EU and elsewhere. Activity in the government sector continues to focus around issues such as urban air quality, flood prediction and prevention, sustainable transport solutions to overcome congestion, emissions compliance, waste and resource efficiency and future energy mix.

Despite UK government pressure on budgets, the business has secured a number of major contract wins with departments such as Defra and BIS. In the US they continued to build relationships with the Department of Energy, the Environmental Protection Agency, the National Highway Traffic Safety Administration and the California Air Resources Board. In the EU they are working with the EU Commission and international donor organisations on a range of new products and initiatives. Future growth is focused on the private sector and international expansion outside of the UK. The acquisition of PPA in November has enabled the business to strengthen its activities in the energy sector, especially in Africa and Asia.

During the past year the group launched Ricardo Motorcycle as a global business unit and added UK based consultancy Vepro during the year. They have continued a partnership relationship with Exnovo, a motorcycle vehicle engineering business in Italy. Growth in the sector is being driven by the need for a reduction in carbon dioxide emissions, the increasing focus on urban mobility solutions and a growing interest in e-bikes together with the increased demand for high quality motorcycles in developing markets. During the year the business remained focused on the delivery of existing large multi-year powertrain programmes for clients in Japan, China and Germany. The business mix covers a number of major subsystems including engines and driveline and transmission systems. They have also secured a new multi-year vehicle programme from an international client in the motorcycle and scooter sector of the market. The high performance vehicles and motorsport team is pursuing a range of new opportunities.

The group has seen strong growth in the commercial vehicle sector, especially from the Asian markets. They have secured a number of large engine and transmission projects across the medium and heavy duty sectors. Activity levels are being driven by legislation and new product development for global applications. Strong engagement in this sector has driven increasing engine test activity, especially in North America. They have also seen growing interest in the aftertreatment and fuel cell capabilities at their technical facility in California. Facilities include a catalyst hydrothermal ageing test lab, a synthetic gas reactor test lab for rapid evaluation and modelling of aftertreatment components and systems, and fuel cell testing capabilities for solid oxide and proton exchange membrane fuel cells. They have also focused on developing their product offering in the areas of fuel economy improvement, system optimisation and hybridisation which are areas seen as significant growth markets.

Activity in the off-highway sector continued to remain at a relatively low level following the recent implementation of stage IV emissions standards in Europe. The focus in the coming years will be assisting clients with EU, US and Chinese legislation for 2020. The product offering in this sector is focused on new powertrain and engine development, complete machine optimisation, cost-effective after treatment solutions and hybridisation options, all of which are attracting increasing levels of interest. They also continue to invest in energy recovery technology.

The group’s defence related activity has seen an important number of new customer wins. They have seen increasing activity in mainland European, Middle Eastern and Asian markets as a result of focused business growth activities outside the UK markets. In the UK they have seen increasing demand for their Total Systems Optimisation approach, a programme which is focused on optimising vehicle architecture selection to minimise lifecycle costs and maximise fuel economy. In the US they have launched Ricardo Defence Systems as a platform for expansion by enabling the business to access higher level security programmes from the US Defence Administration. The focus remains on the land domain and they are actively engaged in a range of future opportunities in international markets.

The Rail business has continued to grow with a focus on Technical Consulting activities in the rolling stock area in both the EU and North America. They are also at an advanced stage with the DDFlyTrain research and development project conducted with Artemis Intelligent Power and Bombardier Transportation. This project has used the company’s high speed flywheel-based brake energy recovery system concept to deliver a projected fuel saving of around 10% on Diesel Multiple Unit rolling stock. The business has developed a broad geographic spread with a variety of programmes taking in Tier 1 equipment manufacturers, rail operators, rail equipment manufacturers and governments with a focus on increasing fuel efficiency and reliability. In the US, the group is developing a Maglev rail system for a low-cost urban connection between Orlando airport and the nearby convention centre.

The clean energy and power generation sector has seen the majority of its activity in the large engine area for power generation. The group is engaged in a number of large projects covering genset development, gas engine conversions, heavy fuel oil engines and Combined Heat and Power solutions. They have seen less activity this year in the renewable energy sector, although they continue to deliver offshore and onshore wind energy projects. Good levels of activity have also been seen in fracking applications for the oil and gas market and there has been significant growth in the management consulting activities across the energy sector. The marine sector is driven by increasing demands for high speed diesel generator sets and main propulsion systems, and also for the conversion of engines for gas or dual fuel operation. The majority of their activities in this sector have been based around failure analysis, investigations, specialist design and development activities.

The underlying operating profit at the Performance Products business was £7.7M, a decline of £200K when compared to last year and order intake declined from £67M last year to £43M. About half of the revenues earned in this sector come from just one customer. in the defence sector, activities have focused on the supply of ongoing post-design services for the UK MOD which included the supply of infra-red lighting and axle upgrade kits.

Demand for engines from McLaren for its supercars continued and the group now supply power units for the new 650S and the P1 hybrid models. The McLaren engine assembly facility is currently being expanded to enable the business to satisfy McLaren’s product expansion plans. Production of the Porsche Cup and advanced dual clutch transmissions to Bugatti continued in line with the long-term supply agreements. In motorsport, the group has remained busy during the year with manufacturing orders from F1 customers, and products such as the transmissions for the Japanese Super Formula, Indy Lights and World Series by Renault. Work has also been ongoing to design and manufacture a GT3 racing transmission for two new premium clients.

Rail activity continues to perform to plan through the continuing manufacture and supply of monorail transmissions for applications in Malaysia and Brazil. They continue to seek out similar future opportunities with exploit the market presence developed through the technical consulting activities and the newly created Ricardo Rail business.

During the year the group completed five major R&D programmes and was awarded five new ones. They have actively engaged with the new European R&D framework programme “Horizon 2020” through the European Green Vehicle initiative. The five new programmes awarded are Horizon 2020 projects.

The DDFlyTrain programme delivered a proof of concept flywheel demonstrator for the rail industry using the Ricardo Torqstor flywheel and test rig. The collaborative partners were Bombardier and Artemis and the research project was co-funded by Innovate UK and the Rail Safety and Standards Board. Bombardier’s Turbostar Diesel Motor Unit was used to project fuel saving, based on high speed flywheel brake recovery technology retrofitted to DMU rolling stock. Simulation and rig testing were used to demonstrate the practical feasibility, operational fuel and energy savings, and the economic investment case for high-speed flywheel energy storage technology on DMU trains. The project received the Rail Exec award in the safety and sustainability category and the TorqStor technology received the 2014 SAE Tech Award as one of the top five technologies on display at the SAE World Congress.

The group has now delivered and commissioned the MultiLife wind turbine bearing system on a 600kw turbine. The Barnesmore wind farm operated by Scottish Power in Donegal, Ireland is known to experience aggressive wind conditions and was used for the location of the project. The system reduces the need to remove and repair the wind turbine gearbox, which increases the time that the turbine is generating revenue. This is achieved by rotating the face of standard bearings over time which ensures that the fatigue damage or wear never reaches a critical localised condition during the turbine’s life. The system has the potential to extend bearing life in excess of 500% based on rig tests. The project was partly funded by the DECC and Ricardo is collaborating with Scottish Power and the Universities of Sheffield and Strathclyde.

A new engine research programme called Magma looks at optimised approaches for gasoline engines, including adoption of the Miller cycle. In the transmission area, the ULTRAN project is yielding impressive results with innovative lightweight transmission designs that reduce the weight of a rear-wheel drive unit by 25%. In the hybrid area, a project to investigate Switched Reluctance Machines for future e-Machine applications is yielding industry-leading FEA tools for e-Machine design. The project delivered a prototype high-speed synchronous reluctance machine. ECOCHAMPS, a new Horizon 2020 project, is targeting the next generation light and heavy duty hybrid electric vehicles.

The US DoD continues to emphasise rapid acquisition of proven innovations that can save soldiers’ lives. The group is investing in a collaborative programme with a Tier 1 supplier to provide a world-class stability system for a tactical vehicle. The solution mitigates the problem of rollover for on and off road vehicle situations and provides improved vehicle performance and reliability whilst offering significant operational cost savings. Development and testing are complete and the product is well-aligned to DoD acquisition objectives.

At the University of Brighton, the Sir Harry Ricardo Combustion Research Centre is expanding to provide a dedicated joint research facility where university staff will work alongside Ricardo engineers. The objective is to undertake fundamental research to assist with the design of the next generation of internal combustion engines while developing the group’s staff to learn new skills and capabilities.

In October the group acquired Vepro and in November they acquired Power Planning Associates for a combined consideration of £3.6M. Vepro brings motorcycle chassis, powertrain integration and prototype build expertise to the motorcycle business. It also brings complementary customer relationships with key accounts in India and the US. PPA provides an extension to the group’s energy sector capability, ranging from conventional small scale and distributed power systems, to renewable power and smart grid technologies. It also specialises in techno-economic and management consultancy services for the energy sector. The consideration was £3M in initial cash which was all paid before the end of the year, along with £600K in contingent consideration. The acquisitions generated a total of £2.3M in goodwill. Since acquisition, the two businesses generated an underlying operating profit of £200K.

On the 1st July, annoyingly just one day after the year-end, the group completed the acquisition of Lloyd’s Register Rail. LR Rail is a rail consultancy and assurance business and is a partner for a wide range of international clients. It provides services ranging from rolling stock design, signalling and train control, intelligent rail systems, operational efficiency improvements, training and independent assurance services. The initial cash consideration is £40.6M and the provisional assessment of goodwill is £28M. It has major clients such as Network Rail, Dutch Railways, MTR, Crossrail, Etihad Rail and Qatar Rail. In August the group acquired Cascade Consulting for a total consideration of £3.2M. The business provides additional capability and reach in the areas of water resource and water quality management, ecosystem services and environmental impact assessment. This acquisition generated £2.6M in goodwill.

At the year-end the group held total banking facilities of £89.4M which included committed facilities of £75M and an overdraft of £14.4M. Committed facilities of £45.4M were drawn down which attracts interest of between 1.6% and 2.35% above LIBOR and are repayable in 2020. The pension scheme is a source of potential problems, the £1.2M increase in the deficit this year was primarily due to a reduction in the discount rate assumption. The additional cash contributions of £4.3M per annum were agreed with the trustees following the last full actuarial valuation in April 2014 – this is not an insignificant sum.

At the year-end the closing order book stood at £140M which is a decline of £2M when compared to the same point of last year. Market conditions remain positive in the UK and Asia, with a good pipeline of defence vehicle activity in the US and recent secured wins in the motorcycle sector in Germany.

At the current share price the shares trade on a PE ratio of 22.5 falling to a more reasonable looking 18.9 on next year’s consensus forecast. After a 9% in the full year dividend, the shares yield 1.8%, increasing to 1.9% on next year’s forecast. The group is currently in a net cash position of £14.3M, an increase of £1.7M year on year with some £40.6M spent on the LR acquisition the day after the year-end which acquired some £12.6M of net assets so after this acquisition I guess the net debt must be about £26.3M.

Overall then this was a solid year for the group. Profits did fall but this was due to acquisition related costs and discounting these, underlying profit was up. Net assets increased year on year and operating cash flow also improved to give a decent amount of free cash. Capital expenditure may well be lower next year as the Vehicle Emissions Research Centre was completed but there will be acquisition related pay outs of course. Operationally, technical consulting seems to be performing well but profits at the performance products division fell as a large project came to an end, presumably for the MOD. Whether the new projects, including the work for McLaren can offset this remains to be seen.

The group has embarked on a bit of an acquisition spree with four over the past year or so. The LR Rail is by far the largest one, and hopefully they will concentrate on assimilating this business rather than go mad on acquisitions. The forward PE of 18.9 is not cheap but probably about right for a company of this quality and the dividend yield of 1.9%, although nice to have, is not really much to get excited about. Ricardo remains my second largest holding so I will not be adding any more at this point but I am happy to hold for the time being.

It seems as though the shares are consolidating…

On the 4th November the group announced the appointment of Ms Malin Persson as non-executive director. She was employed by Volvo between 1995 to 2012 where she was VP Corporate Strategy and Business Development, President and CEO of the research and innovation company Volvo Technology and head of environmental affairs at Volvo Logistics. She is also owner of Accuracy AB, a consultancy and engineering company. This seems like a very strong appointment to me.

On the 19th November the group released a trading update from July to date. They have seen a good start to the year with strong order intake in the last four months of £113M, some £43M higher than at the same point of last year. On a like for like basis, order intake is up £22M with the total order book at the end of October of £206M compared to £132M. Significant orders within technical consulting include a project for an electric bike and two passenger car transmission orders in the US, a multi-year rail project for the independent validation and verification of a transit railway in Asia, and further passenger car orders in Europe. In performance products, there was an increased level of orders for McLaren.

The rail business has performed in line with expectations since the acquisition of LR Rail and the integration is progressing well. The final stage of the acquisition of the rail business is the completion of the joint venture in China which is expected to be finalised in the next few months for an agreed consideration of £1.9M. In performance products preparations are on track for the increase in volumes expected in the second half of the year in respect of the engine supply contract for McLaren and overall trading is in line with board expectations and they remain confident of continued progress during the year.

This all reads quite well and I am fairly happy to keep hold of my shares here, which represents my second largest holding.