Air Partner has now released its interim results for the year ending 2016.

The group no longer seems to split the revenue by sector which is rather annoying but revenue for the period increased by £3.3M and after an increase in cost of sales, gross profit grew by £1.4M. Underlying admin costs increased by nearly £300K and we also see some £270K in acquisition costs and £72K of acquired intangible amortisation to give an operating profit £785K ahead. Finance costs were negligible but after a big swing to a tax cost as opposed to the rebate from last time relating to a R&D claim and changing the tax basis for Jetcards in the US, gave a profit for the year of £1.5M, an increase of £58K year on year.

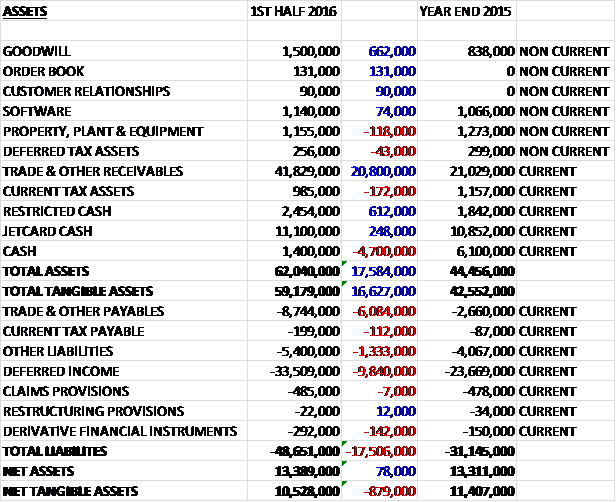

When compared to the end point of last year, total assets increased by £17.6M driven by a £20.8M growth in receivables partially offset by a £4.7M decline in cash levels. Total liabilities also increased during the period due to a £9.8M increase in deferred income, likely related to the increase in money put on the Air Partner Jetcard; a £6.1M increase in payables and a £1.3M growth in other liabilities. The end result is a net tangible asset level of £10.5M, a decline of £879K over the past six months.

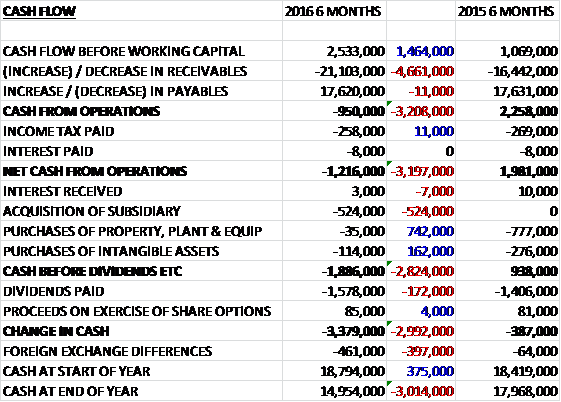

Before movements in working capital, cash profits increased by £1.5M to £2.5M. A large increase in receivables – apparently due to increased receivables from the larger credit clients – meant that after a slightly smaller tax payment the net cash outflow from operations came in at -£1.2M. The group then spent £35K on tangible assets, £114K on intangibles and £524K on an acquisition so that the cash outflow before financing was £1.9M. They also spent £1.6M on dividends so that the outflow for the period was £3.4M to give a cash level of £15M at the end of the half (only £1.4M of this relates to non-jetcard cash). This is actually a rather disappointing performance in my view.

The underlying operating profit in the Commercial Jet Broking division was £1.7M, an increase of £600K when compared to the first half of 2015. The growth was largely driven by improved trading in the UK against fairly easy comparatives in the first half of last year, and in Europe which benefited from a larger tour operating programme compared to summer last year. Within the UK commercial jet business, they increased focus on a clearer sales strategy and improved service levels. Surprisingly there was a strong contribution from the oil and gas sector and other strength came from demand from football teams and continued government work.

Trading in Commercial Jets in Europe was decent, benefiting from a large tour operating programme as well as a strong performance from the German automotive sector (which might now be under threat due to VW’s woes). Austria delivered a stable performance but results in Italy were down year on year mostly due to government related work in 2014 which was not repeated this year. Despite some new customer gains, the performance in the US was behind expectations due to a lower number of one-off charters ad well as less activity that expected from a key customer.

The Cabot operations are now included in the Commercial Jet sector. The group’s existing aircraft remarketing operations are predominantly in the short-term wet lease market but the acquisition adds significant aircraft sales and dry lease expertise, channels where the group has previously experienced demand from its existing customer base. Since the acquisition, Cabot has been appointed as the exclusive marketing agent by China Airlines for two Boeing 747-400s as well as by Kenya Airways for four Boeing 777-200ERs.

The underlying operating profit in the Private Jet Broking division was £939K an increase of £349K year on year. The increase was largely driven by a strong performance in the UK, somewhat offset by a weaker than expected performance in the US. For Jetcard, the targeted sales focus has seen deposits rise to £13.6M from £11.9M at the same point of last year. Utilisations have improved by 22% which helped the card deliver its strongest performance since its launch in 2004. The number of cardholders now stands at 220, up by 45 cards on last year. The highest increase in JetCard numbers was seen in the US with 23 new cards whilst the UK saw an increase of 15 and Europe added 7. The ad-hoc performance has been mixed. While the performance in the UK has been strong, the US and European businesses have experienced a decline in profit when compared to last year.

The underlying operating profit in the Freight division was £394K compared to a break even position in the first half of last year. The group have continued their work with government aid agencies to assist in a number of geopolitical crises and in addition, good growth has been seen in the UK, German and US businesses, albeit from a small base. The “Red Track” technology has continued to the success of the aircraft on ground business and it is encouraging to see the focus and investments made in the business deliver an improved performance.

The fall in the non-jetcard cash level is a little concerning. This is apparently due to working capital movements as a result of increased charter demand from some of the largest credit customers as well as acquisition investments and associated costs.

The group have identified certain components of their customer’s journey that were inconsistent and a programme was put in place to enable them to understand these issues and fix them. The £485K provision relating to claims was held in relation to the settlement of claims which have been received from third parties following the closure of Air Partner Private Jets with all remaining claims expected to be settled by March 2016.

In May the group acquired Cabot Aviation Services, a global aircraft remarketing broker. The total consideration was £814K with £514K settled in cash and the rest settled by an equity consideration. The acquisition came with £264K of intangible assets and generated goodwill of £701K. In the two and a half months since acquisition the business generated operating losses of £53K on revenues of £43K.

After the end of the period, the group acquired Baines Simmons, an aviation safety consultant, for a net consideration of up to £6M. The acquisition was funded from a combination of the group’s cash resources and a £3.6M debt facility.

The board remains confident that its expectations for the remainder of the year will be achieved although I have no idea what those expectations actually are. The success behind the improved trading, notably UK Commercial Jets and the tour operations in Europe, should continue into the latter half of the year. The board also believe that the momentum with JetCard and the UK’s ad-hoc division in Private Jets can be maintained. Challenges remain in the US, however, along with the sluggishness of private jets in Europe and they are looking at improvements in these areas.

After a 10% increase in the interim dividend the shares currently yield a decent 5.2% but I could find no forecasts or the full year dividend.

Overall then this was a decent period of progress for the group. Profit improved year on year, but net tangible assets fell. Although operating cash flow declined, this was due to a large increase in receivables and underlying cash profits improved. Nonetheless the increase in receivables is unwelcome and the group is not generating any operational cash flow at the moment, let alone free cash. The performance in all three divisions improved with commercial jets up due to a good UK performance against poor comparatives last year and a good tour operating programme in Europe. The performance in the US was poor, however, due to less activity from a key customer.

In private jets, the good performance was again driven by the UK with US adhoc orders down. The non-jetcard cash seems to be on the slide, which is a worry and the cash position is not looking that great any more. Still, the Baines Simmons acquisition looks to add a different string to Air Partner’s bow and the 5.2% dividend yield is certainly welcome. I will continue to hold here.

On the 28th January the group released a pre-close trading update. Trading momentum in the second half of the year remained good with a stronger than expected end to the period. As such, the board expect underlying pre-tax profit to be at least £4.2M compared to £2.6M in the prior year. This sounds good to me and I have bought back in here.