AG Barr has now released its interim results for the year ending 2016.

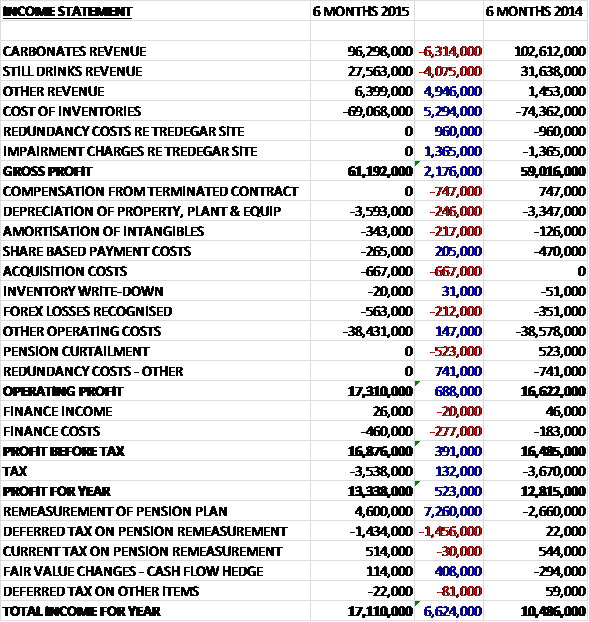

Overall revenues declined when compared to last year as a £5M growth in “other” revenue was more than offset by a £6.3M fall in carbonates revenue and a £4.1M decline in still drinks revenue. Cost of sales also fell and there were no non-underlying costs such as the £1.4M impairment charge at Tredegar and the £960K redundancy costs at the same site so that the gross profit was £2.2M higher. We also see the lack of a £747K compensation for the loss of the Orangina contract and a £667K acquisition cost that occurred this year that caused the operating profit to increase by £688K. Finance costs increased but tax fell somewhat to give a profit for the year of £13.3M, an increase of £523K year on year.

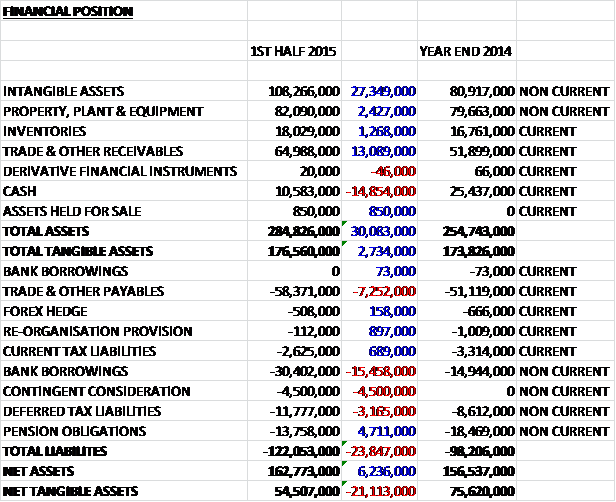

When compared to the end point of last year total assets increased by £30.1M driven by a £27.3M growth in intangible assets relating to the Funkin acquisition and the investment in the BRP project, a £13.1M increase in receivables, a £2.4M increase in property, plant and equipment, and a £1.3M growth in inventories partially offset by a £14.9M decline in cash. Total liabilities also increased during the period as a £15.5M growth in bank borrowings, a £7.3M increase in payables, a £4.5M increase in the contingent consideration and a £3.2M growth in deferred tax liabilities were partially offset by a £4.7M decline in the pension obligations. The end result is a net tangible asset level of £54.5M, a decline of £21.1M over the past six months.

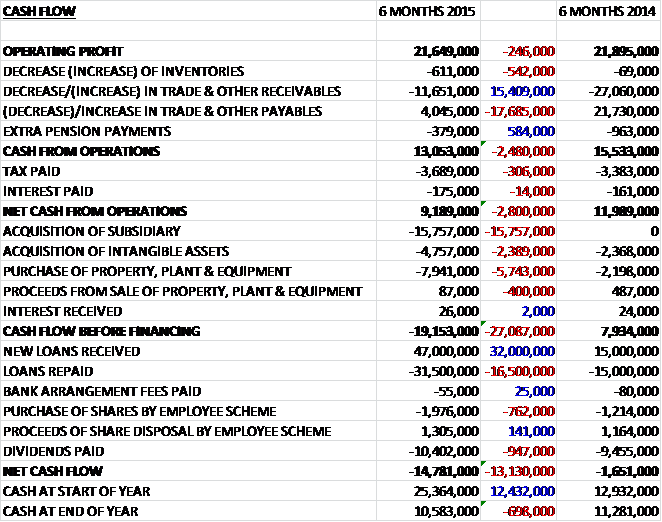

Before movements in working capital, cash profits fell by £246K to £21.6M. The large increase in receivables was much lower than last year (apparently as a result of activity around the Commonwealth Games) but the increase in payables was also lower so that after a slightly higher tax payment the net cash from operations came in at £13.1M, a decline of £2.8M year on year. This did not cover the £7.9M spent on property, plant and equipment relating to normal capex and the acquisition of additional land at the Milton Keynes site, along with the £4.8M purchase of intangible assets and when the £15.8M spent on the acquisition is added, the cash outflow before financing was £19.2M. The group then took out a net £15.5M of new loans which were used to pay the £10.4M of dividends so that the cash outflow for the six month period was £14.8M to give a cash level of £10.6M at the period-end.

There have been a few changes to the numbers reported last time. There was a miss-statement between the gross profit for carbonates and the other segments. An element totalling £2.3M of gross profit in relation to carbonates was reported in the “others” segment which seems a bit sloppy to me. Also, following the implementation of the new ERP system it was concluded that some distribution costs previously recorded in operating expenses would be more appropriately recorded within cost of sales. This has resulted in a reduction in the gross profit of £3.4M for the year and £1.8M in the half-year. There was no change to reported operating profit.

The soft drinks market in the period has been impacted by continued price deflation and very poor weather. As expected the revenue performance has also been affected by the stretching prior year comparatives driven by good weather and the promotional activity around the Commonwealth Games. The total soft drinks market experienced a 0.6% decline in revenue during the period with a modest growth of 1.4% in volume driven by strong performance in water and the positive performance of the energy drinks category.

In the period, gross margin improved, benefiting from a combination of improved procurement conditions and supply chain savings. Operating margins were adversely impacted by the combination of lower volumes and investment in the business, however. The group previously announced a £5M investment at the Cumbernauld factory with the installation of new high speed glass filling capability. The investment will lead to the discontinuation of the returnable glass bottle system at the end of the year but moving to non-returnable, recyclable glass will support the long term development of this popular product format and should facilitate a number of brand development projects next year.

In the period the group also announced phase 3 of the ongoing investment at the Milton Keynes site. Their plans include the building of increased warehouse capacity to improve operational efficiency, flexibility and costs as well as the purchase of four acres of development land adjacent to the site. The total expected cost of the development phase, including the additional land for future expansion, is £11M.

The underlying gross profit in the carbonates division was £50.1M, a decline of £524K year on year; the underlying gross profit in the still drinks and water segment was £8.2M, a fall of £1.9M when compared to the first half of last year; the underlying gross profit in the “other” segment was £2.8M, an increase of £2.3M year on year. This includes the sale of the acquired Funkin cocktail products, rental income for vending machines and the sale of ice cream.

The past six months have been busy for the group. The period began with the closure of the Tredegar factory and the subsequent clearance and sale of the site that completed in September. During the early part of the year they also commissioned carton packaging capability at the Milton Keynes site, increasing capacity and improving flexibility in that product format. In addition, they have completed the planning and go-live of the Business Process Redesign project which means they are now operating their business on a much more effective, modern and robust system capable of supporting sustained future growth.

The go-live of the BPR proved more challenging than anticipated. They experienced a period of difficult internal operating conditions after they went live with the system which impacted the revenue performance and customer service. They have now stabilised their systems and the focus is to realise the business benefits of the new operating platform.

In February the group acquired Funkin ltd, a company which offers a broad range of premium cocktail solutions including fruit purees, cocktail mixers and syrups. The total consideration paid was £22M comprising £17.5M in initial cash and £4.5M of contingent consideration. It came with £7.2M of intangible assets and generated goodwill of £15.7M. Since acquisition the business contributed an operating profit of £700K with a growing international presence in the US and Europe in addition to the leading position in the UK.

During the year the group appointed David Richie, CEO of Bovis Homes on to the board as a non-executive director.

At the period end, the net debt stood at £20M compared to just £3.7M at the same point of last year. The group still has some £14.5M undrawn on the revolving credit facility and £5M of unused overdraft. They have committed to the acquisition of £6.4M of property, plant and equipment.

Market conditions across the first half of the year have been difficult and are forecast to remain so. The business has responded to the market conditions but the poor weather since July has meant that they are not yet at the targeted “run rate”. Assuming a satisfactory trading performance over the important Christmas period, the board now expects the company to deliver a full year result broadly similar to last year, which doesn’t sound that positive.

After an 8% increase in the interim dividend, the shares are now yielding 2.4% increasing to 2.5% on next year’s consensus forecast.

Overall then, this has been an unusually difficult six months for the group. Profits did increase, but this was only because of the closure costs of the Tredegar site last year and underlying profit fell. Net tangible assets declined too, as the acquired Funkin business was mostly made up of intangible assets and operating cash flow fell, with no free cash flow at the end of the period. Both profits in carbonates and still drinks fell with poor weather, price inflation and difficult comparatives with last year all taking their toll. The group is also investing a lot into its plant at the moment with some £16M in additional capex outlined in two different projects so there is some risk associated with this, as the teething problems with the BRP system has shown, and net debt has grown.

Market conditions remain difficult with supermarkets continuing to struggle against price deflation and there is no growth expected this year. All this does mean that the share price has come down a bit, however, and with a forward yield of 2.5% and forward PE ratio of 17.2 the shares no longer look quite as expensive as they did. With the current uncertainties, though, I do not think that now is the right time to invest in this company.

The chart doesn’t look too inspiring…

On the 3rd December the group released a trading statement covering the last 18 weeks. Revenue from the ongoing business increased by 3.9% with year to date revenue from ongoing business falling by 0.2% (actual year to date revenue is down 2.2%). As expected, the revenue performance in Q3 gained momentum as the group put the challenges of the first half of the year behind them. Despite the competitive environment they have maintained market share.

The warehouse expansion project at the Milton Keynes site is nearing completion and good progress is being made on the production capability projects at both Milton Keynes and Cumbernauld, which will provide increased flexibility. The board anticipate that the marketplace will remain highly competitive but assuming a satisfactory Christmas trading period, the company remains on track to meet their expectations for the year.

On the 29th January the group released a pre-close update for Q4 trading. In the quarter they expect to deliver revenue growth of over 2.5%. The soft drinks market in the UK continued to be challenging and highly competitive but business performance continued to improve across the second half of the year and revenue for the year as a whole is expected to be around £257M which is a 1.5% decline on a like for like basis. Across the year the group have tightly controlled their cost base to ensure margins remain steady.

The operational investments in efficiency have continued to make good progress and all of the current projects are expected to be delivered on time and in budget. The implementation issues encountered in the first half associated with the business process re-design go-live have been resolved and free cash flow generations remains strong. Overall they are on course to meet their expectations for the year.

This is a much better update then, trading seems to be improving towards the end of the year which bodes quite well for 2016. Is this enough for me to buy in? I’m not sure, the market remains very competitive and I may be better off sitting this one out. I’ll keep it on watch.