Tower Resources has now released its interim results for the year ending 2015.

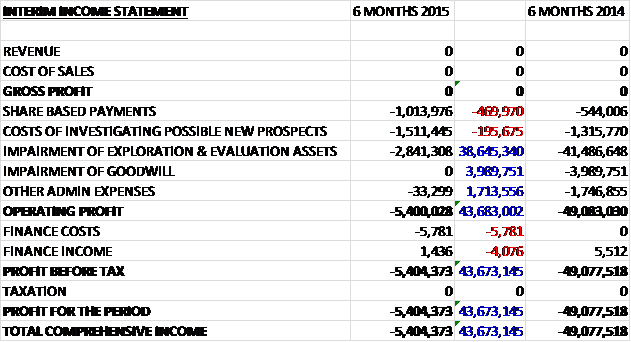

Obviously there is no revenue so no gross profit but there was over $1M of share based payments, an increase of $470K when compared to the first half of last year. The cost of investigating new prospects also increased, up $196K with $800K spent on the Thali license in Cameroon, but these increases were more than offset by a $1.7M decline in other admin expenses. We also see a $2.8M impairment of exploration assets relating to activities in Kenya and Namibia, compared to more than $41M last time and no impairment of goodwill. Finance costs were negligible and there was no tax so the loss for the half year came in at $5.4M, a decline of $43.7M year on year.

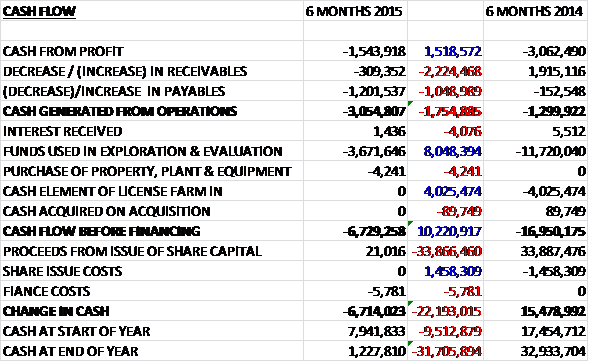

When compared to the end point of last year, total assets fell by $5.6M driven by a $6.7M decline in cash levels, partially offset by an $830K increase in the value of exploration and evaluation assets and a $309K growth in receivables. Liabilities also fell during the period due to a $1.5M decline in trade & other payables. The end result is a net tangible asset level of just $1.2M, a decline of $5M during the period.

Before movements in working capital cash losses halved to $1.5M but a fall in payables meant that the cash outflow from operations was $3.1M, an increase of $1.8M year on year. There was no farm in costs during the period so the only expense was the $3.7M used in exploration and evaluation which included $2.2M spent in Kenya and $600K spent in Namibia, both subsequently impaired, so that before financing, the cash outflow was $6.7M. There were no material items of financing so this was also the cash outflow for the period and the cash level at the end of the half year stood at just $1.2M.

The strategy of the group has changed somewhat. The entry into the Cameroon shallow waters marks a shift in the risk profit from frontier to proven producing basins. They have refocused the portfolio and resources to areas on the Atlantic Margin where they are confident they can add value in this difficult market. They have therefore withdrawn from areas where it is felt there is no medium term likelihood of commercially worthwhile success. They intent to take advantage of the current difficulties in the sector to assemble further acreage and they are moving increasingly towards being an early stage operator.

In Cameroon, negotiations for a 100% interest in the shallow water Thali block PSC continued throughout the period and the PSC was signed with the government in September 2015. The block is located in the Rio Del Rey basin, a proven producing sub-basin of the Niger Delta, offshore Cameroon. The PSC covers depths ranging from 8 to 48 metres and the basin has, to date, produced over one billion barrels of oil and has estimated remaining recoverable reserves of 1.2 billion boe, primarily within water depths of less than 2,000 metres. The Thali block itself includes existing oil and gas discoveries totalling 7M barrels and contains a number of already identified exploration opportunities across four distinct play systems.

On signing the PSC, a three year initial exploration period commenced with a work programme designed to unlock both appraisal and exploration potential. The initial priority is the acquisition of 3D seismic in the first half of 2016. This will be used to update the existing 24 year old data to allow better resolution of shallow plays as well as imaging of deeper sections. The group expect to be drilling by 2017/2018. The market downturn in the services sector presents the opportunity for the company to leverage lower seismic and drilling costs and a partner will be sought to share the financial commitment and provide additional technical input.

The terms of the contract include three exploration phases, including the minimum work commitment of the initial exploration period which covers three years and consists of geological and geophysical studies, 100km2 of 3D seismic acquisition and a commitment well with a minimum financial commitment of $13M. The first renewal period, covering the subsequent two years consists of one exploration or appraisal well with a minimum financial commitment of $15M. The second renewal period of two years also consists of one exploration or appraisal well with a minimum financial commitment of $15M. The company has the option of relinquishing the license on completion of each period.

The current oil discovery on the block is viewed as being sub-commercial but once better seismic imaging has been achieved the company sees potential to add incremental oil reserves to achieve commerciality. There is also significant potential to develop prospects at deeper levels, in both structural and stratigraphic traps once better imaging has been achieved. The existence of infrastructure in adjacent blocks means that the development of a 20M barrel oil field has the potential to be economically viable at current oil prices.

In Namibia the group received formal notification from Repsol, the operator of PEL0010 of their decision not to proceed into a second year of the final renewal period on the license which would have included a commitment to drill a well. After the first renewal period expired in August, the joint venture’s interest in PEL0010 has therefore been relinquished. Tower has itself submitted a proposal to the Namibian Ministry of Mines and Energy for a new license covering the former PEL0010 acreage. The company is also negotiating other new operated acreage positions offshore Namibia.

In Zambia, analysis of the samples taken from the fieldwork programme continued throughout the period. Results indicate that elements for a working petroleum system are present with the potential for both oil and gas generation. No modern seismic or drill data exists in this basin. In August, the company completed its second programme of fieldwork and obtained more encouragement that the area has significant exploration potential with the presence of potential source rock, reservoir and seal now being proven.

Given the existing surrounding infrastructure and constrained domestic energy market, the group believes that there is significant gas to power opportunity in the area with the blocks well positioned relative to markets and distribution infrastructure. The three year secondary period has been split into three one year periods with respective commitments to further field work, airborne gravity and magnetic data acquisition, and a 2D seismic programme. The company is actively looking for a partner to accelerate the programme so that prospects can be drilled in 2017.

In South Africa, in September, approval was received to enter the two year first renewal period on the offshore Algoa-Gamtoos license (50% owned). Evaluation continues by the operator New Age of the previously acquired 3D and 2D seismic with several prospective plays being worked up. Whilst commitments are limited to additional geophysical work, further seismic acquisition is planned, but this will not be possible before 2017 due to environmental restrictions. A funding partner will be sought in due course. Approval to convert the Orange Basin TCP into an exploration right is being awaited.

In Kenya, in February, the group announced that the Block 2B Badada1 well had been drilled but was plugged and abandoned as a dry hole. In May the Kenyan Ministry of Energy granted an extension of six months to the first additional exploration period to enable the joint venture partners to assess the results of the well. Following the group’s assessment a decision was made to exit the licence from the end of August, however, with all license commitments of the first additional exploration period having been met. As a result of renewed political uncertainty in Madagascar and a lack of progress with negotiations for Block 2102, the company has withdrawn its interest for the time being. With the group’s focus now being on the western parts of Africa, the East African Regional office in Uganda has been closed and the head office has moved to a more cost effective premises in London.

In July the company announced a placing and subscription to institutional and some other investors of nearly 3BN shares at a price of 0.19p per share to raise $8M. Of note, M&G investments (part of the Prudential group) invested $3.6M in the placing and they currently hold 18% of the company’s share capital. In addition, Standard life now has a 5% interest and employees and consultants subscribed to $1.4M of the placing funds so there are some heavy hitters invested here. The chairman believes the group is well positioned, he is comfortable with the current funding position and is optimistic about the future.

At the period end the group has cash balances of $1.2M and took in a further $8M in July from an equity funding. The board believe this will be enough to meet its committed capital expenditure programme for at least the next year.

In September, Dr. Philip Frank joined as non-executive director along with Nigel Quinton as exploration director. Dr. Frank has over thirty years of experience in the industry. He joined FTSE250 company Emerald Energy in 2003 as exploration manager until the group was acquired by Sinochem for £532M in 2009. Until March 2015 he was exploration director at Sterling Energy with responsibility for all new venture and exploration activities in Africa and Kurdistan. Nigel Quinton is a geoscientist with over thirty years exploration experience. He is a co-founder of Sterling Energy and became Operations and Technical director after it listed on AIM. He has worked at Tower since 2012 as head of exploration and has overseen the drilling operations and led the negotiation of the entry into the Thali PSC in Cameroon.

Overall then, much like other similar companies, this has been a difficult six months for the group. The loss did improve year on year, but net assets fell and the operating loss increased, although this was due to adverse working capital movements. There was a $6.7M cash burn and after the recent placing, cash is probably at about $9M so there is likely to be enough cash to last the next year but after that more funding is going to need to be sought. The change is strategy from more risky frontier exploration is an interesting one and the Thali block in Cameroon does look rather promising to me. Namibia seems to be on the back burner at the moment, although there are some applications going through. The next drilling is likely to be in either Zambia or Cameroon but will not take place until 2017.

This company is starting to look interesting with the Thali block and there are some heavy hitters investing in the placing. There are a huge number of shares in issue though and I would not rule out yet more dilution further down the line so I am holding tight for the moment. I lost a lot of money on the Namibia debacle so I am a little hesitant to back them again.

On the 16 February the group released a South Africa update. The group with its 50% partner New African Global Energy, have agreed not to proceed with an application to convert the TCP in the SW Orange Basin into an exploration right. Accordingly, New African will reimburse the group the sum of $500K which was paid as part of an original farm-in agreement in 2013, which has now been terminated. The exit from this high-cost deep water frontier basin is consistent with a move towards a more balanced portfolio of proven and emerging basins and will allow Tower to concentrate its efforts in South Africa on the Algoa-Gamtoos ER which offers more near-term potential.

At Algoa-Gamtoos, the 2016 work programme and budget has been approved between the joint venture partners (New Age and Tower). The programme will include further geophysical work and the interpretation of previously acquired 3D seismic data with a view to seeking a partner for the next stage of operational activity.

I suppose every little helps, and this receipt of funds now means that the South African programme for 2016 is self-funding, which is nice.