Internet Q has now released its interim results for the year ending 2015.

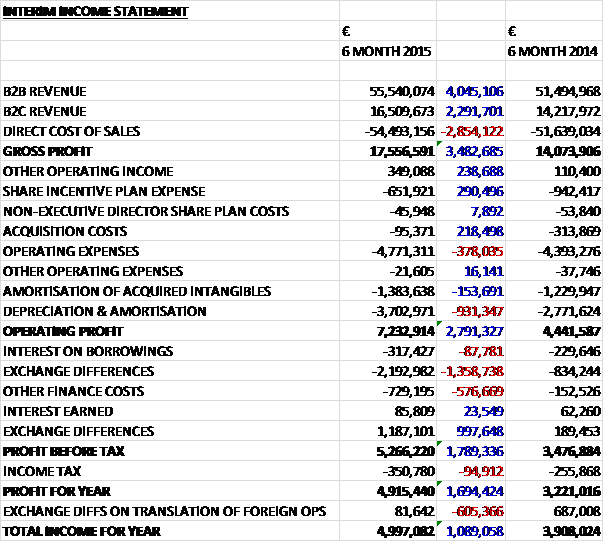

Revenue increased when compared to the first half of last year with a €4M growth in B2B revenues and a €2.3M increase in B2C revenue. Cost of sales also increased somewhat to give a gross profit €3.5M ahead of last time. Other operating income increased somewhat, and the expense related to the incentive plan fell, along with acquisition costs. Other operating expenses did increase, however, and depreciation and amortisation was €931K higher to give an operating profit some €2.8M more than last time. We then see a net €361K exchange rate loss and a €577K growth in other finance costs to give a profit for the period of €4.9M, an increase of €1.7M year on year.

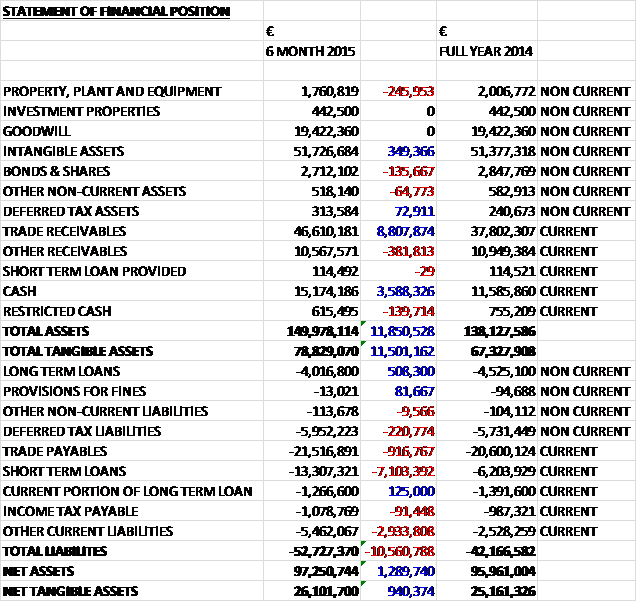

When compared to the end point of last year, total assets increased by €11.9M driven by an €8.8M growth in trade receivables and a €3.6M increase in cash levels. Total liabilities also increased during the period due to a €6.6M increase in loans, a €2.9M growth in “other” current liabilities and a €917K growth in trade payables. The end result is a net tangible asset level of €26.1M, an increase of €940K over the past six months.

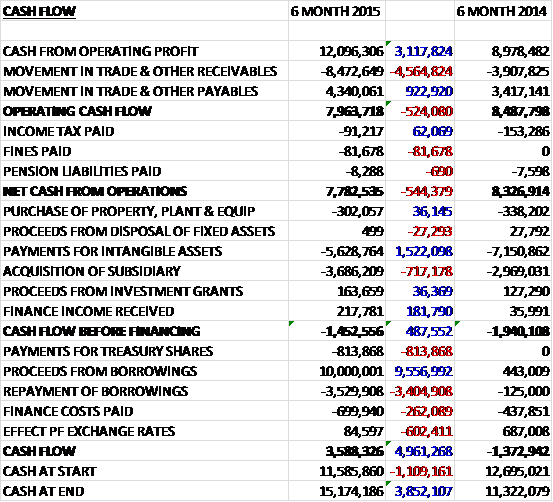

Before movements in working capital, cash profits increased by €3.1M to €12.1M but due to a large increase in receivables, the net cash from operations came in at €7.8M, a decline of €544K when compared to the first half of last year. The group then spent €5.6M on software development and €3.7M on deferred consideration so that once again, there was a cash outflow before financing at €1.5M (the capex is expected to be slightly higher in the second half of the year). The group then took out a net €6.5M of new borrowings to give a cash flow for the period of €3.6M and a cash level of €3.6M at the end of the half.

The adjusted operating profit at the B2B business was €9.6M, an increase of €1.5M year on year. The managed transition away from the lower margin aggregation business is now well progressed and the group is benefiting from its focus on the high-growth high margin Minimob platform. Growth has been fuelled by an increase in Minimob’s direct advertising revenue and the continued expansion of the performance based advertising client base. During the period the group deployed Minimob with China-based global advertisers, including UC Browser and Baidu; direct advertisers, including BBM, NetDragon and HotelQuickly; and agency led brand advertisers, including WeChat, Gumtree and Samsung.

Minimob’s smartphone ad-serving revenues have also grown strongly, increasing from €7M to €35M year on year. Continued progress has also been achieved in developing mobile marketing partnerships with mobile network operators in several geographies with Latin America delivering a 46% increase in revenue from €12M to €17.5M. The release of self-service features on the Minimob platform along with ongoing platform upgrades should drive further growth, free from the challenges display advertising is facing.

The adjusted operating loss at the B2C business was €222K, a €900K improvement year on year. During the period Akazoo produced positive EBITDA and with its pay-only business model, is differentiated in the marketplace. Obviously the main event in this division was the deal with R&R Music, however.

After the period end R&R Music invested €17M and contributed their business to acquire nearly 32% of the Akazoo business. The enlarged entity provides significant new cash resources, IP, human capital, synergies and other related assets. Based on the subscription terms of the new investment, the implied valuation of the enlarged business was about €104M with InternetQ holding about 69% of the business. Akazoo is now cash self-sufficient and the integration of R&R Music is proceeding to plan with the restructuring of the enlarged business across Europe well progressed and expected to be completed in H2. The group expects an impact of up to €3M to the full year EBITDA as a result of the integration and investment to deliver the growth plans of the combined entity.

Going forward the board believe they are on track to achieve full year market expectations prior to the impact of the R&R Music acquisition with revenue expected to show a second half weighting. They see further growth opportunities in the mobile marketing and music streaming sectors. Minimob’s growth potential will be further enhanced by the introduction of new programmatic campaigns, self-service campaign planning and an increase in proprietary data which will drive optimisation going forward. For Akazoo, growth will be supported by the market shift away from freemium models towards pay-only music streaming services, opening up new markets for growth.

The group finished the period with a net debt position of €2.8M consisting of €15.7M cash and €18.5M of bank debt. As usual there is no dividend announced as no free cash is being generated.

Overall then, this was another period of growth for the group. Profits were up, as were net assets but the operating cash flow fell due to a large increase in receivables (underlying cash profits improved) and as usual there is no free cash as the operating cash flow is ploughed back into the business through the purchase of intangible assets. Profits at the Minimob business improved and the losses at Akazoo also got better. The really interesting development here though is the injection of some €17M in cash from a third party that means the business is now self-sufficient. The deal will consume some cash in integration costs but in the medium term it will be interesting to see if the business can generate any real cash without this burden.

That remains the crux really, I find it difficult to invest while the group is not really making any operating cash flow (if we count capitalised intangibles as operating costs, which really they should be). This deal is threatening to make the group investible and I will keep a keen eye on developments here.

Despite the recent up-turn the trend still seems to be negative – one to watch.

On the 17th November the group released an update covering the first nine months of the year. Revenue was up 20% to €105.6M with B2B revenue up 17% to €79.7M and B2C revenue up 30% to €23.3M. Adjusted EBITDA was up 30% to €17.5M and adjusted pre-tax profit increased by 4% to €7.9M.

In Mobile marketing (B2B), new direct advertising campaigns, with no intermediary costs, created new revenue streams, increased momentum and helped drive improved B2B margins. There was a continued improvement in the quality of Minimob’s client base with new campaigns run for global brands including Alibaba, Deutsche Welle, Samsung, Ebay, Deezer, Pandora, Poker Starts, Amazon and HBO. There is also ongoing product development with the creation of a data front end that allows greater insight into daily transactions, the launch of a self-serve advertisers platform, and full development of the programmatic offering that will differentiate the Minimob platform from competition and will apparently help attract new business.

In the Digital Entertainment sector (B2C) there has been the successful integration of Akazoo and R&R Music with the launch of operations across the UK, Greece and Ukraine underway, the app has doubled its subscriptions growth rate in Poland, benefiting from a significant increase in brand awareness. Following the launch of the service in Indonesia in Q1, subscriptions in the region grew at a 50% month on month rate, and there was the successful launch and distribution of Akazoo radio in Poland, Indonesia and South Africa.

The group has recently launched the self-service advertiser platform, as a separate feature of Minimob, and noted a positive adoption of the proposition by clients and partners. They are seeing accelerated revenue growth in the second half of the year with Minimob’s strengthened position fuelling growth of the B2B segment and improved margins. The board expect that the shift towards adtech campaigns will have a positive effect on their top line and cash conversion going forward.

All this sounds very good of course, but what I am really interested in is the cash flow. Until the group starts making some real cash, I will continue to wait on the side lines.

On the 3rd December the group released a statement covering the recent price decline following a blog post. They state that given the factual inaccuracies in the post, they have taken the decision to strongly refute the assertions made and the conclusions drawn. They say that there has been no material change in the operational and financial performance or outlook for the business since the Q3 trading update. I believe the blog post was made by Tom Winnifrith of Share Prophets. There may well be some factual inaccuracies in the blog but he usually does his homework and has been very good at spotting dodgy companies in the past so I would certainly not be buying these shares following this collapse in the share price.

On the 7th December the group released a rebuttal of the blog post last week. They made a few comments, most of which seems to be waffle but some of the more important points in my view were: The B2B concentration ratio referred to by the author refers to 2014 and largely relates to the group’s legacy mobile marketing campaigns business in which the billing/collections were often made using a small number of multi-country aggregators in line with common industry practice (in response to the point about the group having a high client concentration); management strongly denies suggestions that the group is involved in any manipulation of Akazoo’s ratings on social media and the fact that they often agree to use its respective local partner’s brand instead of the Akazoo brand in promoting the B2C service may explain why the Akazoo-related “liking” activity of international pop stars may appear low.

In response to the suggestion that the Akazoo Polska has a terrible brand in the country, the company seems to agree and mentions that in Poland the service now mainly operates using Orange’s own brand (powered by Akazoo). The blog suggests that the group has a relationship with three companies called Twinsbox, Adviator and Bette Tech. Apparently these companies are not related parties and the appearance of the group’s office addresses on the websites of these companies appears to be the case of content scraping and now the company has been made aware of this, they have threatened those parties with legal action and at least one has removed their address from their website.

It appears the group has had dealings with them, however. About five years ago, Twinsbox acted as a trial local agent for the group but as it was unsuccessful this arrangement ended shortly afterwards. They also confirm that they occasionally interacted with Adviator with them acting as a low value systems technical integration contractor on behalf of Russian mobile networks or mobile aggregators active in the Russian market.

Obviously this response is much better than the last one, but this doesn’t quite ring true with me. I have no real opinion either way, however, but it is a fascinating turn of events here and I will watch on with interest.

On the 2nd February the group announced that it has been approached by Toscfund, Penta Capital and the current CEO, acting jointly, about a possible offer for all of the outstanding shares in the company which are not already owned by them. They have until the 1st of March to make an offer. Well, this is an interesting development and obviously had the effect of boosting the shares. I suppose the end game is getting close here and we will find out in a month’s time what is really going on here.

On the 9th February the group released a trading update covering 2015. Revenues increased by 145 to €150M. The Mobile Marketing business contributed about 72% of these revenues and the Digital Entertainment business contributed 28%. Cash levels at the year-end were about €19M compared to €12M at the end of the prior year. Apparently the group has a solid pipeline and is exhibiting positive momentum across both businesses. This is all well and good but their performance is a sideshow really with the most important thing at the moment the potential buy out of the company.

On the 1st March it was announced that the consortium and directors have reached an agreement for the cash offer of the company. Under the terms, each shareholder will receive £1.80 per share which represents a premium of 120% over the closing price before the first announcement and values the company at about £72.2M. It looks as though they have about 54% of the total shareholding already accepting the terms so I suspect this will go through. Interestingly there is a comment that the allegations in Tom Winnifrith’s blog post, or their impact on the share price are not reasons for making the offer and that discussions were already taking place prior to the allegations.

So, it looks like this saga may have come to an end with a pretty decent outcome for shareholders (although perhaps not those that have been holding for the long-term). It seems we will never know whether the company is a scam or not but it has been an interesting saga. Unless anything changes, this will be my last post on this company.