Harvey Nash has now released its interim results for the year ending 2016.

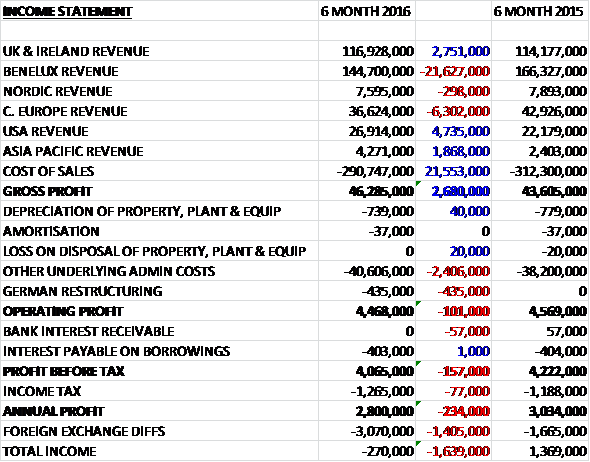

Revenues declined considerably when compared to last year as a £4.7M increase in USA revenue, a £2.8M growth in UK and Ireland revenue and a £1.9M increase in Asia Pacific revenue was more than offset by a £21.6M fall in Benelux revenue and a £6.3M decline in Central Europe revenue with Nordic revenue down by £298K. Cost of sales also fell considerably, however to give a gross profit £2.7M above that of the first half last year. Admin costs increased, though and the German restructuring costs of £435K pushed the operating profits down by £101K. After a small increase in tax and the elimination of bank interest receivable, the profit for the year came in at £2.8M, a decrease of £234K year on year.

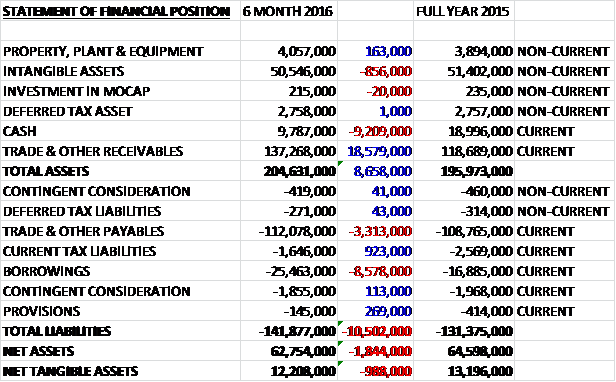

When compared to the end point of last year, total assets increased by £8.7M driven by an £18.6M growth in receivables partially offset by a £9.2M decline in cash and an £856K decrease in intangible assets. Liabilities also increased as an £8.6M increase in borrowings and a £3.3M growth in payables was partially offset by a £923K fall in current tax liabilities. The end result is a net tangible asset level of £12.2M, a decline of £988K over the past six months.

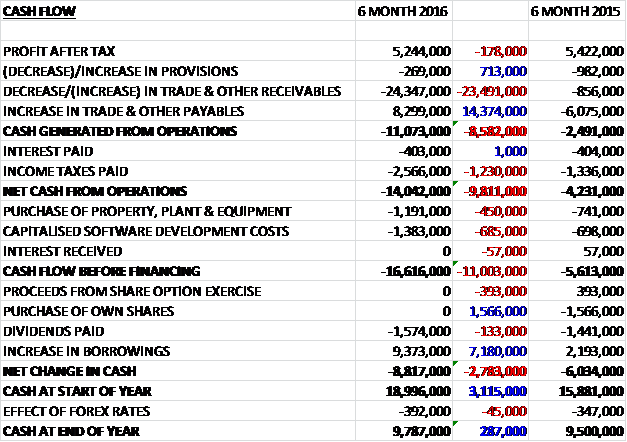

Before movements in working capital, cash profits fall by £178K to £5.2M. A huge increase in receivables, however, along with a smaller increase in tax relating to the payment of prior year taxes in Belgium and Germany, meant that there was a £14M cash outflow from operations, an increase of £9.8M year on year. The group also spent £1.2M on fixed tangible assets relating to the modernisation and updating of the technology platforms and database, technology and office infrastructure spent, and £1.4M on development costs relating to software development for a vehicular small cell solution in Germany, so that before financing there was a cash outflow of £16.6M. After an increase in borrowings, the cash outflow for the period was £8.8M to give a cash level of £9.8M at the period-end.

The growth in contracting in the US, the UK and Benelux has absorbed more cash than normal at the seasonal peak which was exacerbated by a five week billing month ending on the half-year date which meant that receivables increased despite lower turnover and shorter debtor days. In addition, payables decreased due to the unfavourable timing of certain contractor payrolls and as a result, net borrowings increased considerably. The cash performance is expected to improve in the second half of the year as working capital swings substantially reverse and catch-up tax payments and capex flows normalise.

The operating profit in the UK and Irish business was £2.1M, an increase of £181K year on year. Strong results were reported from Scotland and the new UK regional locations of Newcastle and Bristol made their first positive contributions. In London, significant growth was generated from Finance and Banking, which was mitigated by weaker results from oil and gas. Contract demand for technology specialists was robust as the acute skills shortage continued.

While results from the senior interim business were improved on the prior year, the UK election impacted demand for permanent activities in Q1 in local government, education and the NHS. The healthcare market is returning to normal, however, with net fees for the half year up 8.6% and increased demand for international mandates. In Ireland, gross profit increased by 9.3%, led by demand for finance professionals and technology specialists for Dublin-based US multinationals and an improved performance from the recently opened office in Cork.

The operating profit in the Benelux division was £1.8M, a decline of £456K when compared to the first half of last year. Challenging market conditions in the Netherlands and reduced margins for managed services across the Benelux held back profits. Additional investment for growth in Belgium also reduced the short term contribution in Antwerp and Brussels. Demand for permanent placements increased during the period, however. The process of closing the French executive search office was finally completed during May.

The operating profit in Central Europe was £187K, an increase of £186K when compared to the first half of 2015 with increases in Switzerland, Poland and Germany. Gross profit in Germany was 29.4% higher due to the increasing demand for flexible technology and engineering labour and a significant rise in permanent recruitment, with placements more than doubling on the prior period as business confidence improved. In the German outsourcing business, revenue was down 6.4% with a loss of £200K. As a result, further restructuring is being undertaken in the legacy telecoms outsourcing services business in the second half of the year to reduce costs in line with sales.

In the innovations business, software development totalling £1.1M was capitalised in relation to the ongoing development of a vehicular small cell solution for the German automotive industry. Key milestones in support of the policy of capitalisation were achieved and the process of reviewing all options for the future of the German outsourcing business is progressing.

The operating profit in the Nordic business was £107K, a growth of £50K year on year with the figure affected by the devaluation of both the Swedish and Norwegian currencies. The business in Sweden continued to grow, further consolidating its market leading position in senior and professional recruitment and leadership services, with a 15.2% growth in gross profit. Good permanent recruitment activity facilitated a 22.2% increase in fee earners, particularly in the smaller locations such as Finland and Norway. Following the restructuring in Norway last year, the loss in the period was significantly reduced.

The operating profit in the US was £756K, a growth of £286K when compared to the first half of last year, aided by favourable market conditions and strong demand for technology professionals. Permanent placement revenues increased by nearly 20% on the prior year while gross profit contracting and outsourcing grew by 51.3% and 36.4% respectively.

The operating loss in Asia Pacific was £58K, an improvement of £87K year on year on revenues that increased by 77.7% to £4.3M. This was driven by senior executive recruitment in Hong Kong and Japan, an encouraging start to the new Singapore office and continued strong trading in Vietnam where the recruitment business reported an increase in permanent revenues of 15.9%. In Australia a focus on productivity and costs partly mitigated the 16.8% decline in gross profit against the prior period. This was due in part to the weakening Australian dollar but mainly challenging operating conditions in Q1.

After the period-end the group paid the deferred consideration of £2M in respect of the Belgian acquisition of Talent IT. Since the period-end the group has performed in line with management expectations but since the end of the first half, global macro-economic uncertainty has increased, notably with respect to China, and currency issues continue. Overall the board remain positive about the outlook for the rest of the year, however.

The net debt position at the end of the half was £15.7M compared to a net cash position of £2.1M at the end of last year. After a 10% increase in the interim dividend, the shares are currently yielding 3.8%, increasing to 4% on next year’s consensus forecast.

Overall then this has been a mixed period for the group. Profits were down but this was only due to the German restructuring and underlying profits increased slightly. Net assets fell, however, and both cash profits and operating cash flow decreased during the period, with the latter driven by a huge increase in receivables which is being put down to growth in some regions along with a five week billing week – I’m not convinced by that but if these cash flows reverse in the second half, the cash flow for the year should be pretty good.

The UK performed well due to Scotland and some new offices with other good performances from Ireland, Germany, Sweden and the US with Australia and Norway continuing to struggle along with the Netherlands which does not seem to be performing well. With a forward PE of 10.4 and a dividend yield of 4% the shares still look cheap but now there is a net debt position driven by the working capital outflow and growth seems to be stubbornly slow, I am not sure what do about this one.

The share price does seem to have come off slightly in recent months but the recovery is arguably still in place.

On the 7th December the group released a trading update for the first nine months of the year. Overall they traded in line with board expectations with adjusted pre-tax profit increasing by 7% year on year, driven by strong trading in the US and Germany, solid results in the UK and progress in Asia. Net borrowings were at a similar level to the balance at the end of the first half.

The group has also announced the sale of its German telecoms outsourcing business, Nash Technologies, which was completed in early December. The revenues of the business had declined due to the merger involving its largest client, Alcatel-Lucent, and the business was loss making. The group have agreed its sale to the CEO of Nash Technologies by way of a management buyout. The disposal will have no effect on the core recruitment business in Germany, which is trading strongly and contributed €1.3M to group profits in the first nine months of the year.

The aggregate consideration from the disposal payable at completion is just under £20K with the buyer assuming working capital liabilities capped at £1.7M. In addition, the buyer will pay additional cash consideration to the group by way of an earn-out based on the performance of Nash Technologies subject to a maximum amount of £6.5M. It has also been agreed that should the buyer dispose of the business before the end of 2022, they will pay the group the first £1.7M of any net proceeds arising from any such disposal and 50% of any proceeds in excess of this amount, capped at £6.5M.

Excluding the effect of the earn-out, the charge on disposal will include a non-cash loss of £6.2M representing the difference between the net book carrying value of the business and the net cash initial proceeds; and the future cash commitments, capped at £4.1.

I suppose it is good news that they have managed to offload a loss-making part of the business (last year it lost £300K) but the fact that they have not been able to recover any of the book value is very disappointing.

On the 26th February the group released a pre-close trading update. The adjusted pre-tax profit is expected to be in line with market forecasts and gross profit grew across all geographies and service lines on a constant currency basis. The gross profit for permanent recruitment was up 10%, the gross profit for contracting recruitment was up 8% and the gross profit for offshore services increased by 10%. The net cash position at the year-end was £200K, ahead of expectations due to tight control of working capital. There was strong growth in the US with constant currency gross profit up 16% and also Asia Pacific with a 38% growth off a lower base.