Harvey Nash is a provider of specialist recruitment and outsourcing solutions. It has offices in the UK, Europe, the US, Hong Kong, Japan, Australia and Vietnam and it is listed on the LSE. Their services include executive search and leadership services where they work with organisations to recruit board members and senior executives on a permanent and interim basis, along with consultancy such as assessment and leadership services. A second service is professional recruitment where the technology recruitment business helps organisations recruit experts on a permanent and contract basis, and they also provide bespoke assistance to clients in order for them to manage their workforce risk, payroll services and hiring processes. The final service is offshore and solutions where they provide managed IT services and projects, software development, and BPO services in Vietnam along with mission critical elements of telecoms R&D.

Managed solutions have become the gateway to new client relationships, whether it’s the management of existing client business operations or providing recruitment outsourcing and payroll services. Increasingly more routine elements of the recruitment or solutions process are undertaken offshore, reducing cost and increasing efficiency. Revenue anticipated, but not invoiced at the balance sheet date is accrued on the balance sheet as accrued income (perhaps this is common practice but this seems a bit aggressive to me) whilst revenue invoiced but not earned at the balance sheet date is recorded as a liability as deferred income.

The group has now released its final results for the year ended 2015.

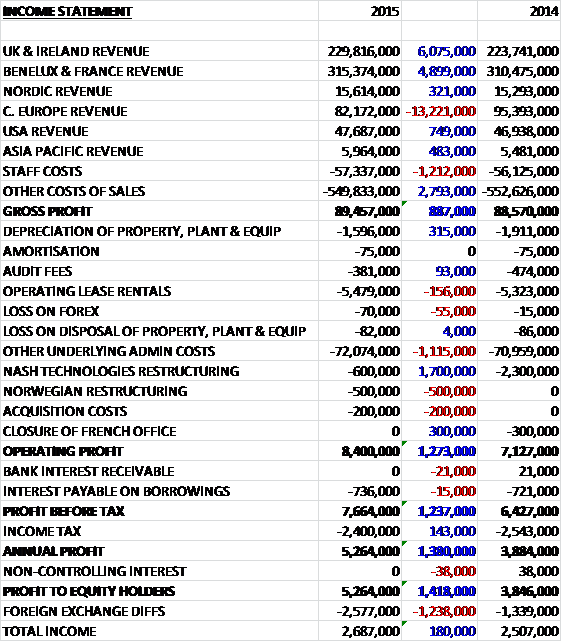

Overall revenues fell when compared to last year as increases in the majority of markets was more than offset by a £13.2M fall in Central European revenue. Staff costs increased slightly but other cost of sales declined to give a gross profit some £887K ahead. We then see a slightly lower depreciation but an increase in admin costs before various non-underling costs took their toll, with a £1.7M fall in Nash Technologies restructuring, partially offset by increases in other costs to give an operating profit £1.2M higher than in 2014. After slightly higher finance costs were offset by a lower tax charge, the profit for the year came in at £5.3M, an increase of £1.4M year on year.

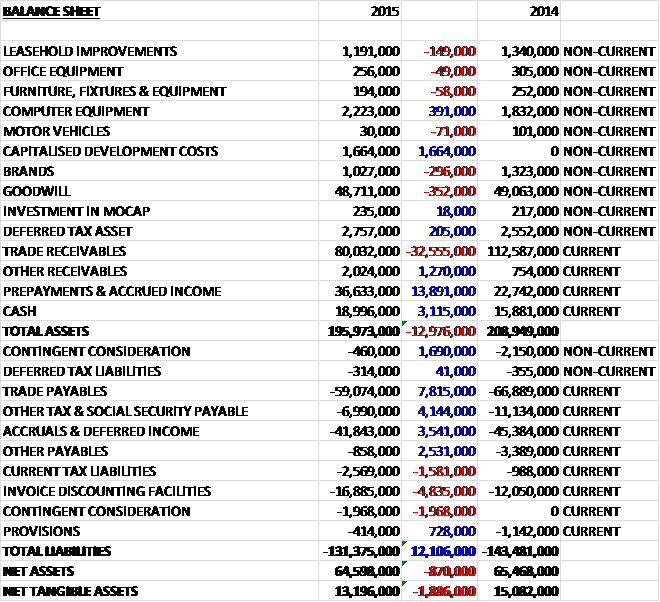

When compared to the end point of last year, total assets fell by £13M driven by a £32.6M decline in trade receivables as a result of efficient working capital management and the timing of invoicing, partially offset by a £13.9M increase in prepayments and accrued income as a result of an increase in accrued income in the Netherlands due to the timing of invoicing, a £3.1M growth in cash, a £1.7M increase in capitalised development costs and a £1.3M growth in other receivables. Total liabilities also fell during the year as a £4.8M increase in the invoice discounting facilities and a £1.6M growth in current tax liabilities was more than offset by a £7.8M fall in trade payables, a £4.1M decline in other tax and social security payables, a £3.5M decrease in accruals and deferred income and a £2.5M fall in other payables. The end result is a net tangible asset level of £13.2M, a decline of £1.9M year on year.

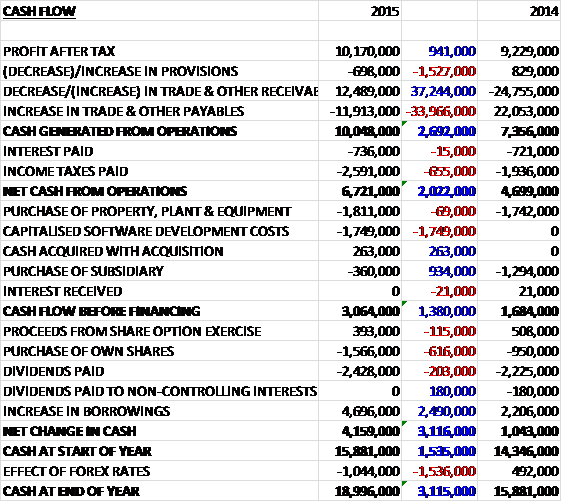

Before movements in working capital, cash profits increased by £941K to £10.2M. There was a broadly neutral working capital position compared to a small outflow last time and after higher taxes were paid, net cash from operations came in at £6.7M, an increase of £2M year on year. The group spent £1.8M on tangible fixed assets and the same amount on software development so that the free cash flow was £3.1M. The group spent all this on buying its own shares and dividends, and after a £4.7M increase in borrowings, the cash flow was £4.2M to give a cash level of £19M at the year end.

The operating profit at the UK and Ireland division was £3.7M, a growth of £524K year on year as the business capitalised on market share gains and continued with investment to expand capacity during the recession. Demand for contingent technology professionals continued to be the strongest area of the market with London and the finance and banking sectors in particular being buoyant. The broader demand for executive and higher salary did not demonstrate similar growth but education, health, consumer and board recruitment has been active. Interim management reported a steady performance with an increasing pipeline of opportunities as the economy continued to improve.

Growth came from the recently established locations in the UK – Newcastle, Bristol and Warrington, with the larger hubs such as Birmingham and Manchester broadly flat against record results in the prior year. In Scotland, the referendum reduced demand for permanent hires but the number of contractors out at the year-end was up 87% comparted to the previous year. In Ireland, continued strong demand from mainly US and European multinationals for IT contractors drove overall growth up 22% in gross profit. The recently established office on Cork also delivered good growth, albeit from a low base. Gross profit from offshore IT services was one again the fastest growing service, up 17% following a strong year of new business sales, underpinning the UK profitability and cementing key recruitment client relationships.

The operating profit in Benelux and France was £4.3M, an increase of £291K when compared to last year. Currency headwinds were the key feature of the Eurozone results. In the Benelux regions, clients continued to favour temporary recruitment over permanent and the business acquired in 2012, Talent IT in Antwerp, delivered a strong result in its final earn-out year with gross profit up 25% which resulted in the trigger of a £2M contingent consideration payment in 2016. The Netherlands reported a small decline of 2% in gross profit terms, mainly related to lower permanent recruitment.

The operating profit at the Nordics business was £351K, a growth of £37K year on year but gross profit declined as a result of a weak performance in Norway. The business in Sweden performed well with gross profit up 16% despite challenging trading conditions with the interim management business reported the strongest growth, up 43%. Finland and Denmark, although both small, both reported strong increases in gross profit. Norway’s economy has been impacted by weakening domestic demand in the first half of the year and a significant decline in the price of oil in the second half such that gross profit was down 37%. The downsizing of the operation and property was not sufficient to return the Norwegian business to breakeven by the end of the year with a smaller loss expected for 2016.

The operating profit in Central Europe was £799K, a decline of £444K when compared to 2014. Results across the region were mixed. In Switzerland and Germany, recruitment gross profit declined by 4% and 6% respectively but in Germany a weak first half was offset by a much stronger second half mainly due to increasing demand for engineering and employed IT consultants. Executive recruitment in Poland was lower than the previous year but technology recruitment was strong with a 94% increase in gross profit.

The operating profit in the US was £865K, an increase of £13K year on year. The business invested in headcount as confidence in the recovery grew stronger. Permanent recruitment was robust as the pipeline of orders for permanent hires continued to improve with net fees up 11% on the last year, with the Seattle office generating the highest proportion. Executive search was up 15% boosted by demand for senior executives to drive technology based digital business strategies in larger companies.

A natural swing in demand occurred during the year from contract to permanent as clients switched their resourcing strategies to filling long term permanent positions. This impacted contribution and led to a small decline in core contracting gross profit over the year. The decline was offset by strong growth in the new Enterprise Technical Delivery Service, which grew by 31%. This service provides contract resources to large enterprises mainly through a vendor management programme using the group’s unique offshore sourcing strategy. The acute skills shortage combined with investment in digital resulted in many clients, mainly in the media sector, resourcing projects with offshore skills based in Vietnam, resulting in an increase of 26% in gross profit from this service.

The operating loss in the Asia Pacific division was £304K, a detrimental movement of £388K when compared to last year due to investment in headcount and new offices. Progress was slower than initially expected and Australia remained challenging. Hong Kong and Vietnam continued to grow their pipeline and headcount, however. The Tokyo team experienced a mixed six months with the integration process a distraction as they settle into the group. The board are confident that the business will be back on track in the year ahead, however.

The demand for permanent recruitment grows as the market expands while temporary, contract and offshore services enable clients to balance risk and achieve cost reductions so are probably more in-demand during difficult periods.

There were some non-recurring items this year. £600K related to the strategic review of Nash Technologies and the relocation of lab assets. £500K related to the restructuring of Norwegian operations and £200K was incurred in the UK in respect of the acquisition cost of Beaumont KK. In total, these came to £1.3M compared to £2.6M last year.

In August 2014 the group acquired Beaumont KK, a recruitment business in Tokyo for an initial consideration of £400K with contingent consideration payments up to a maximum of £500K depending on the performance of the business over the next couple of years to 2017. The acquired business contributed an operating loss of £24K to the group in the five months or so since it was purchased and the transaction generated goodwill of £702K.

If sterling had strengthened by 10% against the US dollar last year, the operating profit would have been £11K lower so no real susceptibility there. If it had strengthened by 10% against the Euro, however, operating profit would have been £619K lower which is a considerable risk for the group. Other potential risks include the disruption to the recruitment sector through the growing use of social media to source candidates and a potential global economic downturn. The group increased its invoice discounting facility to £50M and currently has some £35.1M undrawn, including a £2M overdraft facility.

The softening of permanent recruitment demand experienced in Q4 in mainland Europe appears to have stabilised and the macro outlook is currently supportive in the USA, UK, Ireland, Vietnam and parts of mainland Europe such as Germany and Sweden. The board are expecting similar trends in trading conditions across the major markets and despite the impact of the strong Sterling, they are encouraged by the start of the current year and believe the outturn for the whole year will be in line with expectations.

At the current share price the shares trade on a PE ratio of 13.3 which reduces to 10.4 on next year’s consensus forecast which seems decent value. At the year-end the group had a net cash position of £2.1M compared to £3.8M at the end point of last year. After a 1% increase in the final dividend, the shares are currently yielding 3.7%, increasing to 4% on next year’s forecast.

Overall then, progress seems to have been rather slow over the past year. Profit was up, although if the restructuring and acquisition costs are excluded, the underlying profit was flat. Net assets declined year on year but operating cash flow improved somewhat to give an increased free cash flow, although the group still needed to take out further loans. Operationally, the UK, Ireland, Belgium and Sweden seem to be performing well but Germany, Norway and Australia are not doing so well, albeit Germany does seem to be improving as the year progresses. The weakness of the Euro continues to be a real concern but with a forward PE of 10.4 and dividend yield of 4% along with a net cash position, the shares certainly seem to be factoring this risk in and look a little cheap to me.