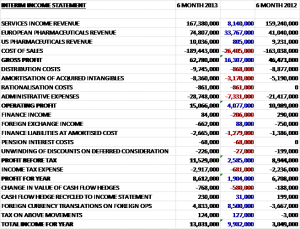

Dechra have now released their half year results for the year ending 2013. I will start with the income statement.

Starting with the revenue, we see that this is up across the board and in particular, revenues in Europe have increased considerably due to the acquisition of Eurovet. Cost of sales are also up, but to a lesser degree so gross profit is £16.3M higher at £62.8M. Admin expenses are also up considerably and there is a big amortisation charge relating to the acquired business. This doesn’t really concern me much as it is a non-cash charge. The operating profit is £15.1M, over £4M up on the same period of last year. This increase is eroded somewhat by some financial costs, the largest of which are financial liabilities at amortised cost – not totally sure what that relates to. There was also a higher tax bill which left the profit for the half year just under £2M higher at £8.6M.

There were some very good currency translations on foreign operations, which left the total income for the half year nearly £10M higher at £13M. Even discounting these exchange differences, I think this is a decent performance.

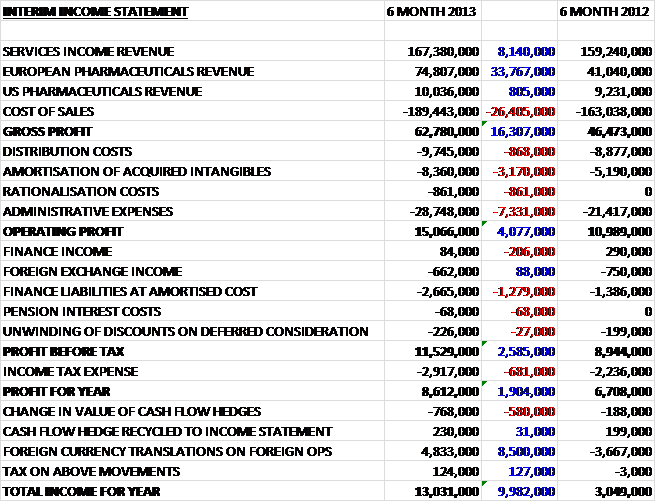

The assets:

From the position at the end of last year we can see that assets have reduced by £16.7M. This is predominantly down to a £15.8M reduction in cash, and partly due to a £3M reduction in intangibles, presumably relating to the goodwill impairment. Small increases in receivables and inventories do little to mitigate this.

Liabilities are also down, however, as a £12.1M reduction in payables and an £8.2M reduction in deferred consideration (presumably as some has now been paid – this will be shown in the cash flow statement below). Overall then, this means that net tangible assets have improved by nearly £10M to leave them at -£62.4M.

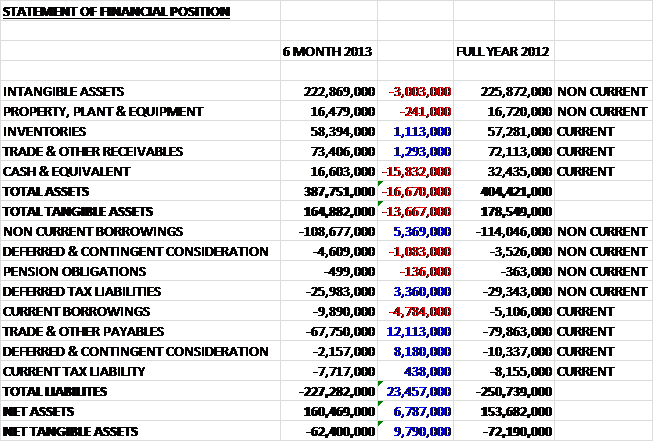

The cash flow statement:

From operations the group achieved a cash flow of £25.9M. Once the movement in working capital had been taken into account, however, this figure was only £11.6M as the group seem to be carrying a lot less in payables than they were, apparently some of this was due to supplier shut downs over Christmas. Interest of £2.7M and tax of £5.1M then wiped out most of the rest of the cash to leave only £3.8M before the capital expenditure of £3.2M is taken account of. The proceeds from new share capital counteracted the repayment of loans but the large headline negative cashflow seen here was caused by a £10.1M payment relating to acquisitions. This was mostly paid due to exceeding $20M income in 12 months from the acquisition of Dermapet as we were made aware of by the statement earlier in the year. There is the potential for $6M more in deferred and contingent consideration being paid. There was also a £7.4M payment for dividends.

I am not sure how useful it is to compare the cash flow for just half a year but clearly the £16M of cash lost is not sustainable. It seems to have been caused by the Dechra paying some of its pending payables and that £10M charge for acquisitions. If payables remained flat and this charge was not incurred then there would be a positive cash flow here. So, not great but hopefully this is a one-off.

By operating profit, the European Pharmaceuticals segment is the most important, but all segments grew profits on last year. The main story operationally is the integration of the Eurovet purchase and savings have already been made by selling products through the new German subsidiary created in the takeover.

Not counting the Eurovet contribution, European sales were relatively flat (but 8% higher at constant currencies). The lack of growth has been put down to less sales due to the old distribution network running down stocks before being transferred to the new subsidiaries. This effect should be reversed in the second half of the year. Own brand pharmaceuticals have been doing well and grew by over 10%. There is a danger going forward that antibiotic usage may be more heavily controlled in Europe due to resistant strains of bacteria becoming more common. Pet diets also did well and were up by more than 6%.

Dechra have made the decision to close the manufacturing facility in Denmark and the licenced pharmaceuticals will now be produced in Skipton in the UK. The Skipton site is already doing well as contract manufacturing increased nearly 16% and a strong order book was reported. Service revenues increased by 5% but pressure remains on margins due to the continuing necessity to discount products. The laboratories increased revenues by 8%.

In the US, progress has been OK, with revenues up 9% at constant currency, although they have experienced supply problems with their in-licensed dermatological range. The veterinary licensed ophthalmic products are being transferred to a new supplier and will be relaunched this year.

There have been a number of successful registrations over the half year, including Methoxasol which is an antimicrobial for swine and poultry in the EU; Soludox has now been authorised for use with Turkeys; Comfortan can now be used for cats; Libromide has been extended into France, Austria, Portugal and Switzerland; and Felimazole has been approved for use in Australia.

During the half year, the group has completed a licencing and supply agreement for a branded veterinary generic pharmaceutical product in the US which will be their first entry into this market. Dechra have already paid $1.5M for this and a potential $5M could be paid in the future. They have also agreed a licencing agreement for SCY-641, which is used for the treatment of Canine Keratoconjunctivitis. Again, a fee has been paid (not disclosed) and more could follow.

Net debt increased by £15.3M to £102M. Net assets £160.5M comprising mostly of goodwill. Bank facilities are currently at £130M which at this rate doesn’t give a huge amount of head room.

So, overall this is a fairly decent update. Revenues are up across the board, but mainly due to the extra sales bought in by the Eurovet acquisition. The profit for the half year was £2M higher at £8.6M. Net assets are up due to the reduction in trade and payables, and the payment of the contingent consideration but net tangible assets are still a negative reflecting the large amount of intangibles on the books. The lack of debt headroom is a worry and the net debt of over £100M is also a bit of a concern given the lack of tangible assets and I hope that they haven’t overextended themselves with these recent large purchases.

Going forward, trading continues to be robust but the regulatory pressure on vets to reduce use of antibiotics is being monitored and in January the performance of the Services segment was poor due to bad weather affecting footfall in vet surgeries. Operationally, this half was all about the continuing Eurovet integration and things seem to be going fairly well in this regard, though the warning about the low vet footfall in January may be a slight worry. It is pleasing to see Dechra entering new markets with the branded generic pharmaceuticals in the US.

Cash flow this half year was strongly negative but this was entirely due to the movements in working capital and the payment of the contingent consideration relating to the Dermapet takeover – there is not much left to pay with regards to that now and these issues can be considered one-off cash costs. The dividend here is nothing to write home about and is currently yielding 1.8%. So, there are some concerns here (particularly about the large debt and the worry over the use of antibiotics) but overall I see these shares as continuing to be worth holding.

On 8th May, Dechra released an interim statement covering Q3 2013. Overall revenue for the quarter was up nearly 15% on the same period of last year and was 18% up during the first three quarters. The best performing sector was European Pharmaceuticals that due to the Eurovet acquisition was up nearly 70% in the quarter and a similar amount for the nine months. On a like for like basis, companion animal products were up 11%, farm animal products up 1% and pet diets grew by 2% for the first nine months of the year.

US Pharmaceuticals did not fare so well, in Q3, revenues crashed by over 14% over last year but were roughly level in the nine month period. This has been blamed on problems with a third party manufacturer, which is very disappointing. Revenue in the services sector also declined, down by 2.5% but for the nine month period, revenue was up nearly 3%. This is apparently due to significantly reduced footfall through vet practices, which in turn is blamed on the weather!

Overall this is a disappointing update, all sectors seem to have slowed in the third quarter and the supplier issues in the US is of particular concern. The fact that reduced service revenues are blamed on the weather also seems a bit week to me. The performance in April is apparently much better, however, so I still rate these as a hold (just about).

On 10th July, Dechra released a trading update covering the whole year. Overall, group revenues were up 19% but performance was hampered by supply issues in the US and adverse weather in Europe. European revenues increased by 65%, but most of this increase was due to the contribution from Eurovet. On a like for like basis, revenues were up 5% despite being hampered by a prolonged winter period. Both Pharmaceuticals and Diets improved. In the US, revenues increased by a modest 3% due to third party supply issues that still do not seem to be resolved. Services revenue grew by 6% year n year and the segment secured some important new contracts, including agreements with internet pharmacies. The net debt position was improved in the second half of the year. Not a bad update by any means but the fact that the supply issues in the US are not yet resolved are cause for some concern.

On the same day, Dechra announced their intention to sell the National Vet Services, Dechra Lab Services and Dechra Speciality Labs to Patterson Inc of America for a cash total of £87.5M. The reasons given by the board are that it enables Dechra to focus on its key own branded vet products business which is higher margin than the service business and that there are no material synergies between the Pharmaceuticals segment and the Services segment. The cash receipt will go towards clearing some of the debt, which I definitely approve of.

The Services group basically includes the labs and the distribution service to vet practices and it generates a lot of revenue for the group, but only about £11M of profit during the year. The services segment has £59M of net assets, so when combing this with the £11M of profit each year, I do think that £87.5M is a little cheap. It will obviously reduce profits and increase costs (as Dechra will still have to distribute its products) in the short term and it means that Patterson will have a foothold in the UK market. What their long term intentions are, I’m not sure but it worries me slightly.

Overall then, I do think that Dechra are running on too much debt and this is probably the best way of gaining the cash to pay that down. I have some concerns that the disposal is taking place at too low a price and it will hit profits in the short term.