Cranswick manufactures and supplies food products to UK grocery retailers, the food service sector and other food producers. The core market is the UK where they provide a range of fresh pork, gourmet sausages, premium cooked meats, cooked poultry, charcuterie, bacon, pastry products and sandwiches. About 75% of revenues come from the retail customers primarily through retailer own label products. They sell into the top four UK grocers along with the premium grocery and discounter channels. Export sales generate about 5% of revenues, primarily to Europe, Oceania, West Africa and the US.

The group’s biological assets consist of pigs (breeding sows, boars and pigs) and it has now released its final results for the year ended 2015.

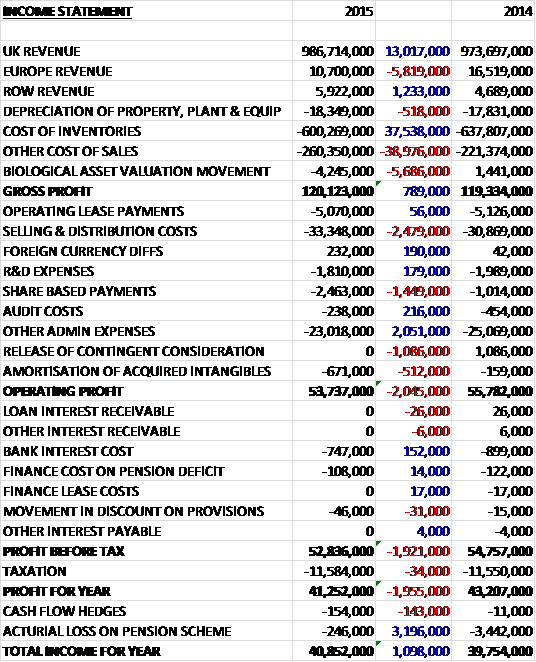

Revenues increased year on year as a £5.8M decline in European revenue was more than offset by a £13M growth in UK revenue and a £1.2M increase in ROW sales. Cost of inventories fell by £37.5M but this was offset by a similar increase in other cost of sales but there was a £5.7M detrimental movement in the value of biological assets so the gross profit was £789K above that of last year. Selling and distribution costs increased by £2.5M and share based payments were £1.4M higher but other admin expenses fell by £2.1M before the lack of a £1.1M contingent consideration release last year was not repeated and a £512K increase in the amortisation of acquired intangibles meant that operating profit fell by £2M. Finance costs were slightly lower, mainly due to a reduction in interest payments and tax was broadly flat to that the profit for the year was £41.3M, a decline of £2M year on year.

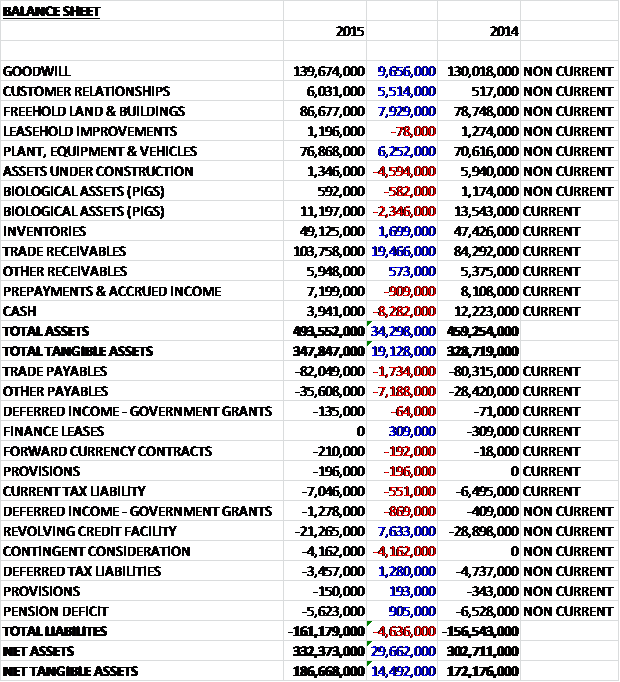

When compared to the end point of last year, total assets increased by £34.3M driven by a £19.5M growth in trade receivables, a £9.7M increase in goodwill, a £7.9M increase in the value of freeholds, a £6.3M growth in plant and equipment, a £5.5M increase in the value of customer relationships and a £1.7M increase in inventories was partially offset by an £8.3M fall in cash, a £4.6M decline in assets under construction and a £2.9M fall in biological assets. Total liabilities also increased as a £7.2M increase in other payables, a £4.2M growth in the contingent consideration, and a £1.7M increase in trade receivables was partially offset by a £7.6M fall in the revolving credit facility and a £1.3M decrease in deferred tax liabilities. The end result is a net tangible asset level of £186.7M, an increase of £14.5M year on year.

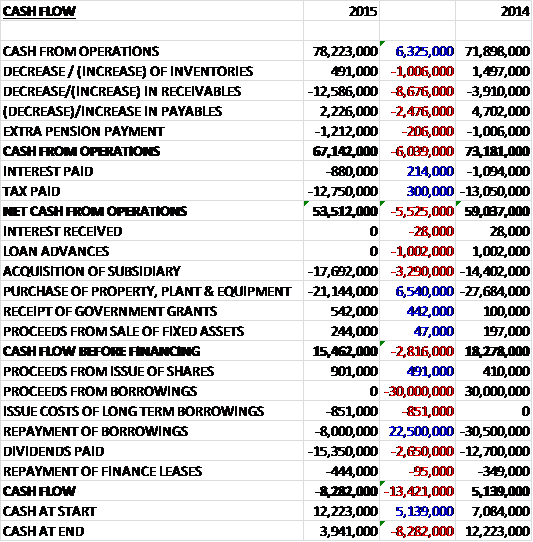

Before movements in working capital, cash profits increased by £6.3M to £78.2M. There was a large cash outflow from working capital, mainly as a result of a big increase in receivables which meant that after slightly lower payments of interest and tax, the net cash from operations was £53.5M, a decline of £5.5M year on year. The group spent £21.1M of this on capex and £17.7M on the acquisition of a subsidiary so that, even after the acquisition, there was a £15.5M cash inflow before financing. The group spent all of this on dividends but also spent £8M on loan repayments so that the cash outflow for the year was £8.3M to give a cash level of just £3.9M at the year end.

Volumes were 3% ahead of last year with growth strongest in the second half but this was offset by the impact of lower input prices being passed on to customers. Continental, bacon and sausages were the product areas that saw particularly good increases. Underlying sales for the year were comparable to the previous year as these increases were offset by lower fresh pork sales and the decision to use all of their own pigs internally as pig prices decreased year on year.

Following a substantial investment in the group’s pig breeding and rearing activities during the previous year, the business this year has focused on improving the quality of the herd and the performance of the breeding, rearing and finishing units. There is now capacity to provide more than 20% if the group’s overall British pig requirements and there will be ongoing investment to improve productivity and efficiencies.

Exports to non-European markets were 23% ahead of the prior year, as the business continues to make progress in developing their export trade. They are now exporting to a number of countries in the Far East and have recently sent shipments to Australia and West Africa. They now have a dedicated business development manager based in Shanghai and are working with the China British Business Council to expand their knowledge of the Chinese market. Exports to Europe were lower than last year as product was sold into the UK market where prices were more attractive.

Fresh pork sales were 10% lower than last year. This was partly due to the loss of business with one customer at the start of the year, which has now been recovered in full. The fall in sales was also attributable to a 9% fall in the average pig price with this reduction being reflected in lower selling prices. Fresh pork sales were supported by a strong BBQ season in the first half of the year along with a buoyant Christmas trading period. During the year work on the new rapid chill system at the Norfolk abattoir was completed. This investment has made the plant more energy efficient as well as improving yields and throughput speeds.

Pastry sales increased by 72% year on year. The rapid growth of the business initially added complexity and cost resulting in the return from the investment being below initial expectations but the performance from the Malton facility improved markedly during the second half. During the year several new products were listed with the lead customer and further products will shortly be launched for the Spring/Summer season. Good progress was made in broadening the customer base for these products through food service, forecourt and food to go channels, including some existing customers of the group’s sandwich business.

Cooked meat sales grew by 2% supported by new product launches and a strong promotional calendar as well as increased business with a key retail customer after securing a long term supply agreement last year. The project to extend the Milton Keynes facility was completed during the year on time and to budget. This investment increased capacity at the site and will deliver efficiency gains as well as improving product quality. During Q4 this year, all production at the Kingston Foods site in Milton Keynes was transferred to the facility in Hull. The consolidation of production at one site will allow the business to better serve its customers and to deliver cost savings. The board has agreed further investment at the Kingston facility which will see it used as a satellite gammon production site.

Sales of continental products increased by 8% reflecting the UK consumer’s growing taste for speciality continental products including charcuterie, cheeses, pasta and olives. Growth was supported by new product launches and new retail contracts in the second half of last year together with a focus on sourcing artisan products from across Europe. During Q4, a range of fresh olives was launched with a new premium grocery customer. The business increased sales of its British charcuterie range and is investing £600K in a new salami production facility at its site in Manchester to provide additional capacity in the fast growing category.

Bacon sales were 4% ahead of last year as continued growth of the hand cured, air dried bacon was supported by substantial increases in sales of premium gammon which is a product area that the group has a strong market position and where barriers to entry are high. During the year the business moved to sole supply status for premium bacon and gammon with one of their leading retail customers. Sales over the key Christmas trading period were particularly strong, with volumes well ahead of the same period last year.

Sausage sales increased by 6% with growth in premium sausage and beef burgers partly countered by lower sales of frozen and mid-tier ranges. The market for the premium product offerings is growing much faster than at the lower end. Sandwich sales grew by 15% driven partly by new contract wins at the start of the period and by additional sales to existing customers. The new contracts brought additional complexity to the business through an increased product range which adversely impacted operational efficiencies but a clear improvement was seen in the second half of the year. This improvement was achieved by a focus on labour efficiencies and yields and by streamlining the customer base and product range.

The retail market is reporting deflation for the first time against a backdrop of continuous growth, driven partly by falling commodity prices across the food chain, but also a trading environment which remains extremely competitive with price wars and the major multiples losing market share to discount retailers. Although there is top line deflation, in core categories such as bacon and sausage, premium tiers are growing strongly.

The food on the move category has grown significantly over the last four years. The group have made good progress in this area and have developed a strong portfolio of sandwiches and gourmet pastry ranges to service these channels. They have also accessed new channels including retailer cafes and front of store chillers. The group are working with a number of specific customers in the pub and restaurant sectors to improve quality, including projects such as better breakfast and the emerging trends around pulled pork and other premium products.

The retail sector remains challenging with deflation evident across the industry but the food to go category continues to perform strongly in both retail and travel sectors. The group have historically concentrated on the travel sector but new business wins in channels such as in store restaurants and hot food counters provide new revenue streams. The group are actively targeting new convenience sales which requires a different approach to product development and a new way of servicing the supply chain. They have won new contracts within the convenience sector over the past year and the business is aligning their core product offers to ensure they are tailored to the growing trend of online shopping.

In October 2014 the group acquired Benson Park for a total consideration of £23.8M consisting of £20M in cash and £3.8M in contingent consideration. The business produces premium cooked poultry which adds a new protein sector to the group and broadens the product range and customer base. The acquisition generated goodwill of £9.3M and in the five months it has been a part of the group it has contributed profits of £1.1M which seems pretty good to me. The contingent consideration is payable based on the performance of the business over a two and a half year period up to a maximum of £4M. The business has traded in line with expectations since acquisition and the major capital expenditure programme envisaged at the time of the acquisition has started with commissioning expected towards the end of 2015 which will increase capacity, improve efficiencies and allow them to offer a broader range of products.

The group has an available bank overdraft facility of £20M, none of which was utilised at the year-end. They also have a revolving credit facility of £100M of which only £22M was utilised at the year-end.

Many of the executive directors have been with the group for a long time and are certainly very competent but they also seem very well paid, perhaps excessively so. This year the CEO was paid £2.3M including bonus and LTIP and the Chairman, who used to be CEO was paid £1.8M which seems very excessive to me. None of them really has a great interest in the shares of the company either and over 27% of shareholders voted against the remuneration policy which indicates a great deal of shareholder unease over the remuneration too.

The group does have a pension scheme but it was closed to new members back in 2004. The liability is currently £5.6M on assets of £24.4 so this is a pretty poorly performing pension scheme but with obligations of just £30.2M the potential downside is not huge. They have contracted future capital expenditure of £2.9M at the end of the year and £4.2M in operating lease payments during 2016.

The group has three customers who account for more than 10% of revenue, being 25%, 23% and 11%. Clearly this is a bit of a weakness but as they supply each of the big four supermarkets, I assume they are the large clients. The group hedges a both a proportion of its near term purchases and sales denominated in Euros but a 100 basis point increase in Sterling against the currency would reduce pre-tax profits by £442K with a similar gain on the weakening of Sterling. Another specific risk to the group is the potential for a significant infection or disease outbreak that may result in the loss of supply of both pig or poultry meat or the inability to move animals freely, impacting on the supply of key raw materials to the group’s sites.

The board are apparently confident that the group is well positioned to continue its successful long term development, which doesn’t tell us anything really. The shares currently trade on a PE ratio of 19.9 reducing to 17 on next year’s forecast which does not look that cheap. After a 6.3% increase in the total dividend, the shares are currently yielding 2% increasing to 2.2% on next year’s consensus forecast. Net debt stood at £17.3M at the end of the year compared to £17M at the end of last year.

On the 1st October the group released a trading update for the first half of the year. Total revenues were 10% ahead of the same period last year and slightly ahead of board expectations driven by strong volume growth across most product categories and a strong contribution from Benson Park. Underlying sales were 7% higher with volumes up 10% as customers continue to see the benefits of lower input prices. The next phase of the development and the Norfolk primary processing facility will start in Q3. This £6M investment will increase capacity and operating efficiencies as well as underpinning the plant’s drive to gain USDA accreditation. The major capital investment programme at Benson Park remains on track and will be commissioned ahead of the 2015 Christmas trading period. Net borrowings were below the previous quarter end and comfortably lower than a year ago.

Overall then this seems to have been a fairly solid year for the group. Profits were down but this was due to the reduction in the valuation of the pigs and if it were not for this, underlying profits would have increased. Net assets were also up and although operating cash flow declined, again this was due to a large increase in receivables and cash profits were up with a lot of free cash generated. Operationally, volumes have increased while prices have fallen due to lower input prices and food deflation. Strong performances in continental, bacon, sausages and ROW exports were partially offset by a reduction in sales in fresh pork, a fall in exports to Europe, presumably as a result of the strong pound, and a fall in margins at pastries and sandwiches as new customers and products “increased complexity”.

The Benson Park acquisition looks a canny one and it is already contributing to profits but the reliance on the big four supermarkets as customers does leave the group rather exposed to this very competitive market at the moment. With a forward PE of 17 and dividend yield of 2.2% these shares are not cheap but that is to be expected for a quality, cash generative business. The update for H1 this year shows revenues increasing but no mention is made of profits so I guess they are faring less well. Tricky one this, I think they are probably priced about right.